Disclaimer: This article is general information for Ontario readers and Canadian small-business owners. It is not legal, accounting, or tax advice. The right structure depends on your corporation, family situation, province, contracts, and future plans.

At a Glance

A Holding Company can be useful in Canada, but it does not create automatic tax savings. Its main value is often tax deferral inside a corporate group, not permanent tax elimination. In many cases, the real planning advantages come from intercorporate dividend flows, asset separation, and future sale planning. The risks usually come from passive investment income, associated-corporation rules, and poor timing before a share sale. CRA’s guidance on the small business deduction, corporation tax rates, and associated corporations makes that clear.

Quick Answer

A holding company does not create automatic tax savings in Canada. Its main tax value is often deferral, meaning profits may sometimes move within a corporate group and remain invested before you personally withdraw them. The legal starting point for that planning is section 112 of the Income Tax Act, which generally allows a corporation to deduct a taxable dividend it receives from a taxable Canadian corporation when computing taxable income. But that does not mean the money becomes tax-free in your hands. Once funds come out personally, personal tax usually enters the picture. On top of that, Part IV tax, passive investment income rules, associated-corporation rules, and qualified small business corporation share tests can all change the result. A holding company can be smart planning, but it can also become an expensive misunderstanding.

Why the “holding company saves tax” pitch is only partly true

A lot of business owners hear the same simplified message: “Set up a holding company and save tax.” That sounds clean, but it leaves out the most important part of the analysis.

In Canada, a holding company can be useful because after-tax business profits may sometimes be paid from an operating company to another corporation without triggering immediate personal tax. That can create a timing advantage if the money stays in the corporate structure for investing, creditor separation, or future planning. But timing is not the same as permanent tax elimination. If you need the money personally now, the benefit often shrinks quickly. CRA’s corporation tax rates page shows why: the federal small-business rate and the general corporate rate are lower than many personal rates, so there can be value in leaving money inside the corporate system. But once cash comes out to you, the personal tax side of the equation starts to matter.

That is the real truth behind most holding company tax savings discussions. A holding company may improve when tax is paid. It does not guarantee less total tax in every case. That is especially true when owners withdraw most corporate profits every year for personal living costs.

What is a holding company?

A holding company is usually a corporation that owns shares, investments, or surplus assets rather than running the active business itself. In a common structure, the operating company earns active business income, signs contracts, employs staff, and carries the day-to-day commercial risk. The holding company owns shares of the operating company, receives dividends, or holds investment assets and retained earnings.

That distinction matters because a holding company is not a special tax program. It is just a corporation used for a different purpose inside a group. The tax result depends on what the holding company owns, how cash moves between companies, and what happens later when money is paid to the shareholder. CRA’s pages on corporation income tax returns and when to file reinforce the practical point: a holding company is still a corporation, which means another T2 return, another compliance cycle, and usually another layer of bookkeeping and administration.

[Internal link: incorporated business tax checklist]

[Internal link: year-end corporate tax planning guide]

[Internal link: small business bookkeeping checklist]

Does a holding company actually save tax?

Sometimes, yes, but usually through timing rather than magic.

The most common planning reason for a holding company is that section 112 of the Income Tax Act generally allows an intercorporate dividend deduction where one corporation receives a taxable dividend from another taxable Canadian corporation. That can let after-tax profits move from Opco to holding company without immediate personal tax. But it is still too simplistic to say those dividends are always “tax free.” Part IV tax under section 186 can apply to certain assessable dividends, especially depending on whether the payer is connected to the recipient and how dividend refund rules work. Section 129 then becomes relevant because it governs refund mechanics such as refundable dividend tax on hand.

So the practical tax question is not “Can I move money to a holding company?” The real question is: Do I need that money personally now, or can it stay invested inside the group? If it stays inside the group, the deferral can be meaningful. If it comes out to you personally right away, the value of the structure may be much smaller than the original pitch suggested.

Who should even think about a holding company?

A holding company usually becomes worth discussing only when there is already an incorporated business producing profits that may stay in the corporate structure. It is generally not the first planning move for someone who is still operating as a sole proprietor or someone who draws out nearly all business profits personally every year.

The structure tends to become more relevant when the operating company has excess retained earnings, wants to separate investable cash from operating risk, or is moving into longer-term estate or sale planning. It becomes less compelling when the business is still early-stage, cash-hungry, or fully distributing profits for the owner’s living costs. That follows from the way corporate rates, filing obligations, and group-planning rules work under CRA’s corporate tax framework.

How passive income inside a holding company can reduce the benefit

This is where the structure can become less attractive than expected.

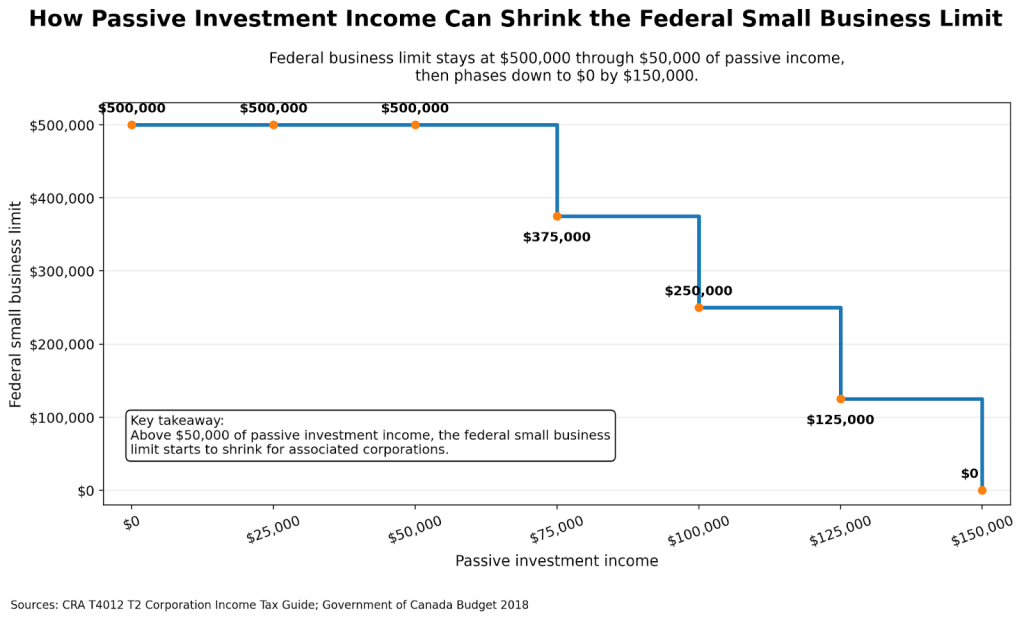

CRA’s small business deduction rules say a CCPC’s federal business limit is reduced when the corporation and associated corporations earn combined adjusted aggregate investment income between $50,000 and $150,000. Once the passive-income grind starts, more active business income can move out of the lower federal small-business rate and into the higher general federal corporate rate.

That matters because a holding company is often associated with the operating company. If the holding company earns enough passive investment income, the group may lose some of its federal small-business-rate room even if the active business is still doing everything “right.” CRA’s pages on associated corporations and the SBD and the passive-income grind both point to the same conclusion: you need to look at the corporate group, not just one legal entity.

Ontario adds an important nuance. CRA says the Ontario small business deduction is not subject to the federal passive-income business-limit reduction. So the federal grind still hurts, but the Ontario small-business-limit calculation does not follow that same passive-income reduction rule. That does not make passive income harmless. It just makes the tax result more nuanced than many business owners expect.

Can a holding company hurt a future share sale?

Yes.

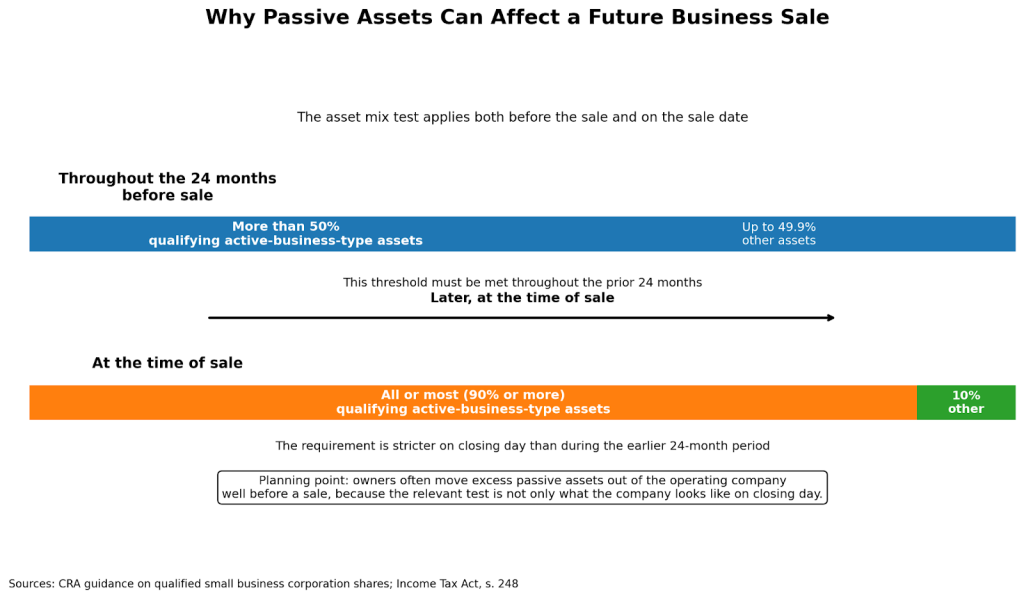

A holding company can support sale planning, but it can also create problems if passive assets stay in the wrong place or if planning starts too late. CRA’s guidance on qualified small business corporation shares says that, generally, a small business corporation must meet an “all or substantially all” active-asset test at the time of sale, and CRA commonly interprets “all or substantially all” as about 90% or more. Related QSBC conditions also look back over a prior period, which is why owners talk about purification and early planning.

This is where a holding company can be helpful. If excess passive assets are moved out of the operating company early enough and properly, the operating company may be better positioned for a future share sale. But if passive assets are left in the wrong corporation too long, or if the cleanup starts only when a sale is already approaching, the desired share-sale tax result may not be available when you need it.

Holding company vs operating company

A holding company and an operating company do different jobs:

| Feature | Operating Company | Holding Company |

| Main purpose | Runs the active business | Holds shares, investments, or surplus assets |

| Revenue source | Sales and operating income | Dividends, interest, rents, gains, investments |

| Tax focus | Small business deduction, payroll, HST, operations | Intercorporate dividends, passive income, sale planning |

| Risk profile | Customer, employee, lease, and contract risk | Usually lower operating risk if structured properly |

| Best use case | Day-to-day business | Deferral, asset separation, long-term planning |

The table is simplified, but it captures the key point: a Holding Company is most useful when it has a clear purpose beyond “someone told me it saves tax.”

What Ontario owners should know in 2026

Ontario owners should separate what is current law from what is proposed.

CRA’s current Ontario small business deduction page still reflects a lower Ontario corporate rate of 3.2% for eligible small business income, while Ontario’s 2026 Budget annex and economy chapter state that the government is proposing to cut the small business corporate income tax rate from 3.2% to 2.2% effective July 1, 2026. That is a proposal, not something to assume has already become law in every planning model.

Federally, CRA’s corporation tax rates page still shows a 9% small-business rate and a 15% general federal rate. That means the advantage of keeping qualifying active business income inside a corporation remains part of the planning conversation, especially where passive income could reduce access to the federal small-business rate.

What is the smart way to set this up?

The smart approach is to start with goals, not paperwork.

First, confirm whether you already have an operating corporation or are still carrying on business personally. Then map the current flow of salaries, dividends, and retained earnings. Estimate how much cash must come out personally each year. Measure passive investment income already earned, or likely to be earned, across associated corporations. Review whether a future share sale matters to you. And compare the tax benefit against the real cost of separate bookkeeping, separate legal maintenance, and another T2 filing cycle. CRA’s corporation income tax return and when to file pages make clear that a second corporation means a second annual compliance obligation.

Only after that should you decide whether to add a holding company, use an existing company, or leave the structure alone.

Common mistakes

Most holding company mistakes come from treating the structure like a universal tax hack.

Common examples include:

- assuming a holding company means tax-free personal cash

- ignoring Part IV tax and connected-corporation rules on intercorporate dividends

- forgetting the passive-income grind

- leaving passive assets in the wrong place before a future sale

- using a holding company even though profits are mostly withdrawn personally every year

- ignoring the extra filing and compliance work

Those are not abstract risks. They flow directly from the rules in section 112, section 186, CRA’s passive-income guidance, and CRA’s filing rules for corporations.

FAQ

Does a holding company always reduce tax in Canada?

No. A holding company may improve tax timing by keeping money inside the corporate system, but it does not guarantee lower total tax for every owner.

Can I move money from Opco to holding company without paying personal tax right away?

Often, an intercorporate dividend can move within the corporate structure without immediate personal tax because section 112 generally allows a deduction for certain taxable dividends received from taxable Canadian corporations. But Part IV tax still needs review.

Will passive income in holding company affect Opco?

It can. CRA says the federal business limit is reduced when the corporation and associated corporations earn combined passive investment income above the threshold range.

Does Ontario follow the federal passive-income business-limit reduction?

Not for Ontario’s small business deduction calculation. CRA says Ontario’s small business limit is not subject to that federal passive-income reduction.

Does a holding company create more paperwork?

Yes. Most resident corporations must file a T2 every year even if no tax is payable, and most must now file electronically.

Final Takeaway

A Holding Company can be useful in Canada, but the real benefit is narrower than the marketing pitch. The strongest cases are usually about deferral, asset separation, and sale planning, not instant tax miracles. If your business earns surplus profits that can stay inside the corporate group, a holding company may help. If you need most of the money personally every year, or if passive assets and sale planning are ignored, the structure may add cost faster than it adds value. The right time to review a holding company is before money moves, not after.

If you want a version tailored for your website style, I can also turn this into a cleaner final draft with chart callouts and stronger CTA language.

Sources & References

- Income Tax Act, section 112 – Intercorporate dividend deduction

https://laws-lois.justice.gc.ca/eng/acts/I-3.3/section-112.html - Income Tax Act, section 186 – Part IV tax on assessable dividends

https://laws-lois.justice.gc.ca/eng/acts/I-3.3/section-186.html - Income Tax Act, section 129 – Refundable tax mechanics for private corporations

https://laws-lois.justice.gc.ca/eng/acts/I-3.3/section-129.html - CRA, Corporation tax rates

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/corporations/corporation-tax-rates.html - CRA, Small business deduction rules and passive investment income

https://www.canada.ca/en/revenue-agency/programs/about-canada-revenue-agency-cra/federal-government-budgets/budget-2018-equality-growth-strong-middle-class/passive-investment-income/small-business-deduction-rules.html - CRA, How certain relationships affect the small business deduction and SR&ED investment tax credits

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/corporations/business-tax-credits/how-relationships-affect-small-business-deduction-sred-investment-tax-credits.html - CRA, Corporation income tax return

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/corporations/corporation-income-tax-return.html - CRA, When to file your corporation income tax return

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/corporations/corporation-income-tax-return/when-file-your-corporation-income-tax-return.html - CRA, Ontario small business deduction

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/corporations/provincial-territorial-corporation-tax/ontario-provincial-corporation-tax/ontario-small-business-deduction.html - Ontario Government, 2026 Ontario Budget – Annex

https://budget.ontario.ca/2026/annex.html - Ontario Government, 2026 Ontario Budget – Chapter 1B Economy

https://budget.ontario.ca/2026/chapter-1b-economy.html - CRA, Definitions for capital gains – eligible small business corporation

https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/about-your-tax-return/tax-return/completing-a-tax-return/personal-income/line-12700-capital-gains/definitions-capital-gains.html - CRA, Selling a business

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/business-registration/maintain-business/selling-business.html