Disclaimer: This article is general information for Ontario readers and Canadian incorporated contractors. It is not legal, accounting, or tax advice. Personal services business results depend on the actual facts of the working relationship, not just what the contract says.

Quick Answer

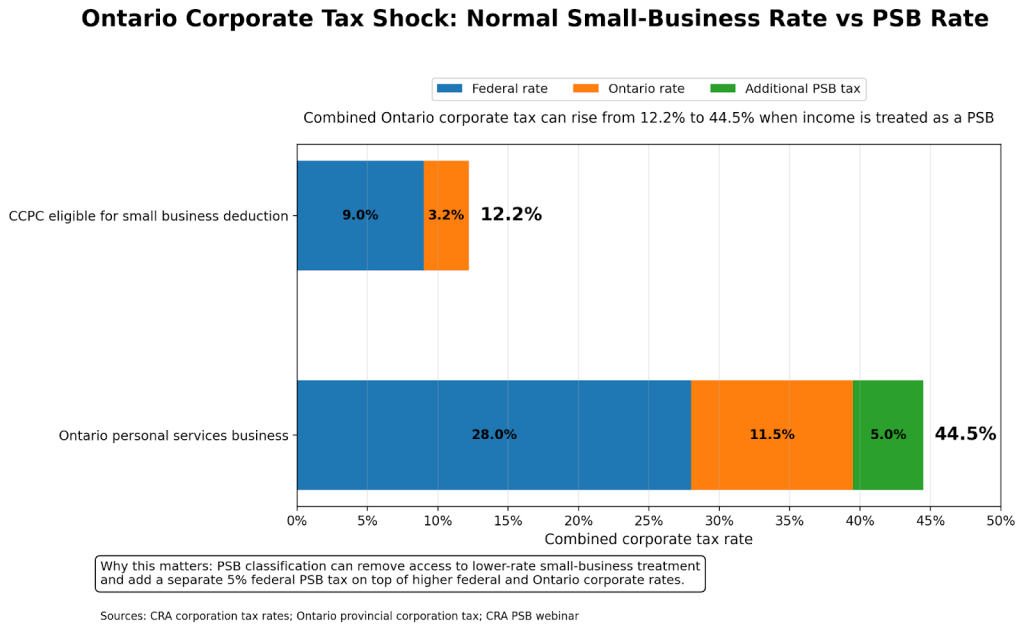

In Canadian tax law, the important term is usually personal services business, not “personal service provider.” CRA’s newer guidance on what a PSB is explains that a corporation can be treated as a PSB when the individual doing the work would reasonably be considered an employee of the client if the corporation did not exist, unless one of the statutory exceptions applies. If that happens, the corporation can lose access to the small business deduction, lose the general tax reduction, face an additional 5% federal PSB tax, and be limited to a much narrower list of deductible expenses. CRA’s own PSB webinar says that in Ontario, this can push the corporate tax rate on PSB income to 44.5%.

Why this issue matters more than many contractors expect

A lot of incorporated contractors assume the biggest challenge is winning the contract and getting paid. The bigger risk often shows up later, when CRA asks a different question: are you really carrying on an independent business, or are you effectively working like an employee through a corporation? CRA’s page on employment status makes clear that labels and intentions do not decide the answer on their own. What matters is the actual relationship: who controls the work, who bears risk, who supplies tools, and whether the worker is running a business on their own account.

That is why a corporation that looks perfectly normal from the outside can still be treated as a PSB. If CRA reaches that conclusion, the tax outcome changes sharply. The company may lose valuable deductions, lose lower-rate corporate treatment, and face a much larger tax bill than expected. In practice, the mistake is often not incorporation itself. It is assuming incorporation automatically fixes an employee-style relationship.

What “personal service provider” means in CRA terms

In everyday business language, people often say personal service provider, but CRA and the Income Tax Act use the term personal services business. The legal definition appears in section 125 of the Income Tax Act, which says a PSB generally exists where an individual performing services on behalf of the corporation, or a related person, is a specified shareholder and that incorporated employee would reasonably be regarded as an officer or employee of the client if the corporation did not exist. The main exceptions are where the corporation employs more than five full-time employees throughout the year in the business, or where the service income comes from an associated corporation.

That definition matters because a PSB is not just “an incorporated contractor.” It is a specific tax category. The issue is not whether you invoice through a corporation. The issue is whether the actual working arrangement still looks like employment after you strip away the corporate shell. CRA’s own PSB page uses almost exactly that framing.

When CRA may treat a corporation as a PSB

The practical analysis is closely related to CRA’s employee-versus-self-employed test. CRA’s current page on employment status explains that employees are generally under the direction and control of the payer, are integrated into the payer’s business, and do not usually have a real chance to make a profit or suffer a loss. By contrast, a self-employed worker is carrying on their own business and is free to choose how to perform the contract.

In PSB situations, the same kinds of facts matter: control over the work, ability to hire or substitute others, who supplies tools and workspace, exclusivity, profit and loss risk, and how integrated the worker is into the client’s operations. CRA’s PSB webinar gives a very familiar example: one shareholder, one worker, one client, client-owned tools, and work that looks like the client’s own employee role. That is exactly the pattern that raises PSB risk. A contract calling you an “independent contractor” helps only if the real-world facts support that label. CRA’s employment-status guidance is clear that the facts outrank the wording.

Why the tax hit can be so severe

The tax cost is high because a PSB loses access to major corporate tax preferences and gets hit with an extra federal tax on top. CRA’s page on what a PSB is states that PSB income is not eligible for the general tax reduction or the small business deduction, and CRA’s T2 guide, Chapter 7 says a corporation must add an amount equal to 5% of its taxable income from a personal services business under section 123.5.

CRA’s PSB webinar walks through the Ontario result in plain terms. It says the federal corporate tax rate starts at 38%, is reduced to 28% after the federal abatement, and that PSBs do not get the general rate reduction or the small business deduction. It then adds Ontario’s 11.5% corporate rate and the extra 5% PSB tax, producing a total corporate tax rate of 44.5% on PSB income in Ontario. That is why this issue is not just a technical classification problem. It can materially change the economics of working through a corporation.

Which expenses usually survive

Very few.

The key rule is in paragraph 18(1)(p) of the Income Tax Act, which says that where a corporation is earning income from a personal services business, deductions are largely denied except for a short list. That list includes salary, wages, or other remuneration paid to the incorporated employee, benefits or allowances provided to that incorporated employee, certain selling or contract-negotiation expenses, and legal expenses incurred to collect amounts owing for services rendered. CRA’s PSB webinar and T2 materials mirror that restricted list.

This is one of the most expensive surprises for incorporated contractors. A corporation that looks ordinary from a bookkeeping perspective may stop looking ordinary for tax purposes once CRA classifies it as a PSB. Office expenses, travel, meals, home office costs, software, and similar items may not survive the way owners expected. CRA’s PSB materials emphasize that the damage is usually double: a higher tax rate and fewer deductions at the same time.

Filing and payroll obligations still apply

PSB status does not remove your filing obligations. CRA’s page on corporation income tax returns says resident corporations generally must file a T2 every tax year, even if there is no tax payable. CRA’s when to file your T2 return page says the return is generally due within six months after the end of the corporation’s tax year. And CRA’s T2 guide before-you-start section says the old $1 million threshold for mandatory electronic filing has been eliminated for tax years starting after 2023, which means most corporations now have to file electronically.

If the corporation pays salary or wages, payroll rules still apply. CRA’s page on PSB obligations says a PSB must open a payroll account and file information returns if it makes payments to employees or self-employed workers, including where the employee is also the specified shareholder. CRA’s webinar also says that if salary is paid, the corporation must withhold income tax, CPP, and sometimes EI, remit them on time, and issue T4 slips.

Incorporated contractor vs likely PSB

No single factor decides the answer, but some patterns are clearly safer than others.

| Feature | More like a true independent business | More like a likely PSB |

| Client base | Several clients or active client development | One dominant client |

| Control | Worker decides how work is done | Client controls methods, schedule, and daily work |

| Tools and equipment | Worker invests in tools/workspace | Client supplies key tools/equipment |

| Subcontracting | Worker can hire help or substitutes | Worker must perform services personally |

| Profit and loss | Real upside and downside | Little meaningful financial risk |

| Integration | Separate brand and business presence | Worker functions like part of client’s workforce |

| Tax result | Possible normal corporate treatment | Higher PSB risk |

This table is simplified, but it lines up with CRA’s employment-status guidance and its PSB materials. The final answer always depends on the full factual picture.

What to do now if you think the risk is real

Start with the facts, not fear.

Review your biggest client relationship and ask whether, without the corporation, you would reasonably look like that client’s employee. Then check whether the corporation had more than five full-time employees throughout the year in the business, or whether the service income came from an associated corporation. If not, the usual statutory exceptions may not help. From there, revisit the expenses already claimed and confirm whether they would still survive if CRA treated the corporation as a PSB.

If older returns may be wrong, CRA’s page on reassessments and adjustments to your T2 return and the page on requesting a reassessment explain the correction process. The CRA webinar also points taxpayers to reassessment and voluntary-disclosure options where appropriate.

Common mistakes to avoid

The most common PSB mistake is assuming incorporation alone solves employee-status risk. It does not. The second is relying too heavily on a written contractor agreement without checking whether the real facts line up. The third is claiming ordinary corporate deductions without reviewing the restricted PSB rules. The fourth is ignoring payroll and T4 obligations once the corporation starts paying salary. And the fifth is assuming old T2 filings are safe from review just because they are already filed. CRA’s pages on PSBs, employment status, T2 filing, and reassessment all point in the opposite direction.

FAQ

Is “personal service provider” the legal tax term in Canada?

Not usually. CRA and the Income Tax Act use the term personal services business.

Can I still be a PSB if I have a written contractor agreement?

Yes. CRA says the actual facts of the working relationship matter more than the label in the contract.

Does one client automatically mean I am a PSB?

No. But one-client structures often create more risk, especially when the corporation does not look like a real independent business.

What deductions can a PSB usually claim?

Generally, only a narrow group of expenses survives, including remuneration to the incorporated employee, related benefits or allowances, certain selling or contract-negotiation expenses, and legal expenses to collect amounts owing.

How expensive can PSB treatment be in Ontario?

CRA’s webinar says Ontario PSB income can face a combined corporate tax rate of 44.5%.

Final Takeaway

The key point is simple: the real risk is not the phrase personal service provider. The real risk is whether CRA can treat your corporation as a personal services business. When that happens, the damage usually comes from three directions at once: a harsher tax rate, fewer deductions, and cleanup work on returns and payroll reporting. The safest approach is to test the facts early, not after a CRA reassessment letter arrives. If you mainly serve one client, work under that client’s control, use that client’s tools, and do not operate like a genuine independent business, the PSB risk deserves serious review.

If you want, I can also turn this into a more SEO-focused version with stronger keyword placement for personal service provider and cleaner chart callout text.

Sources & References

- CRA, Fact sheet – Personal Services Business

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/corporations/corporation-income-tax-return/personal-services-business-pilot/fact-sheet-personal-business.html - CRA, Personal Services Business webinar

https://www.canada.ca/en/revenue-agency/news/cra-multimedia-library/businesses-video-gallery/personal-services-business.html - CRA, What is a PSB

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/corporations/corporation-income-tax-return/tax-implications-personal-services-business/what-psb.html - CRA, Understand your obligations as a corporation carrying on a PSB or the payer of a PSB

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/corporations/corporation-income-tax-return/tax-implications-personal-services-business/obligations-psb.html - CRA, Employment status: Employee or self-employed

https://www.canada.ca/en/revenue-agency/services/tax/canada-pension-plan-cpp-employment-insurance-ei-rulings/employee-self-employed.html - CRA, T2 Corporation Income Tax Guide – Chapter 7: Page 8 of the T2 return

https://www.canada.ca/en/revenue-agency/services/forms-publications/publications/t4012/t2-corporation-income-tax-guide-chapter-7-page-8-t2-return.html - CRA, T2 Corporation Income Tax Guide – Before you start

https://www.canada.ca/en/revenue-agency/services/forms-publications/publications/t4012/t2-corporation-income-tax-guide-before-you-start.html - CRA, Corporation income tax return

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/corporations/corporation-income-tax-return.html - CRA, When to file your corporation income tax return

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/corporations/corporation-income-tax-return/when-file-your-corporation-income-tax-return.html - CRA, Reassessments and adjustments to your T2 return

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/corporations/after-you-file-your-corporation-income-tax-return/reassessments-adjustments-your-t2-return.html - CRA, Requesting a reassessment of your T2 return

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/corporations/after-you-file-your-corporation-income-tax-return/reassessments-adjustments-your-t2-return/requesting-a-reassessment-your-t2-return.html - CRA, Corporation tax rates

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/corporations/corporation-tax-rates.html - Department of Justice, Income Tax Act, section 125

https://laws-lois.justice.gc.ca/eng/acts/i-3.3/section-125.html - Department of Justice, Income Tax Act, section 123.5

https://laws-lois.justice.gc.ca/eng/acts/I-3.3/section-123.5.html - Department of Justice, Income Tax Act, section 18(1)(p)

https://laws-lois.justice.gc.ca/eng/acts/I-3.3/section-18.html - Ontario Government, Corporate Income Tax

https://www.ontario.ca/document/corporations-tax/corporate-income-tax