Quick Answer

For annual reporting periods beginning on or after January 1, 2026, the IASB’s IFRS changes are concentrated in three areas:

- Amendments to IFRS 9 and IFRS 7 on classification, measurement, and related disclosures for financial instruments.

- Contracts Referencing Nature-dependent Electricity (targeted amendments to IFRS 9 and IFRS 7), often relevant for renewable power purchase agreements.

- Annual Improvements to IFRS Accounting Standards, Volume 11, which includes smaller amendments affecting multiple standards.

In Canada, IFRS is required mainly for publicly accountable enterprises, while many private companies can use ASPE unless they choose IFRS. Even when a new standard is not effective until later (for example IFRS 18 in 2027), IAS 8 generally expects useful disclosure about the possible impact when the change is material.

Opening Hook

IFRS changes can feel technical, but the consequences are very practical.

A missed disclosure can delay audited financial statements. A delayed audit can delay financing renewals. A confusing note can raise questions from lenders or investors, especially if your business has covenants tied to ratios or defined subtotals.

The 2026 IFRS updates are not just fine print. They introduce new and updated expectations around financial instruments and related disclosures, plus annual improvements that can quietly change checklists and documentation. If you report under IFRS in Canada, the smart move is to treat 2026 as a structured implementation project, not a year-end surprise.

Quick Start: Pick Your Path

- Public company or publicly accountable enterprise

Focus on: What changed in 2026, Implementation roadmap, Common mistakes - Private company using IFRS for lenders or investors

Focus on: Financial instruments changes, IAS 8 disclosures, Covenants - Private company unsure whether IFRS is required

Start with: Do you need IFRS in Canada - Energy buyer or seller with renewable PPAs

Focus on: Nature-dependent electricity contracts amendments - Planning ahead for bigger 2027 changes

Focus on: Issued but not effective yet: what to prepare for

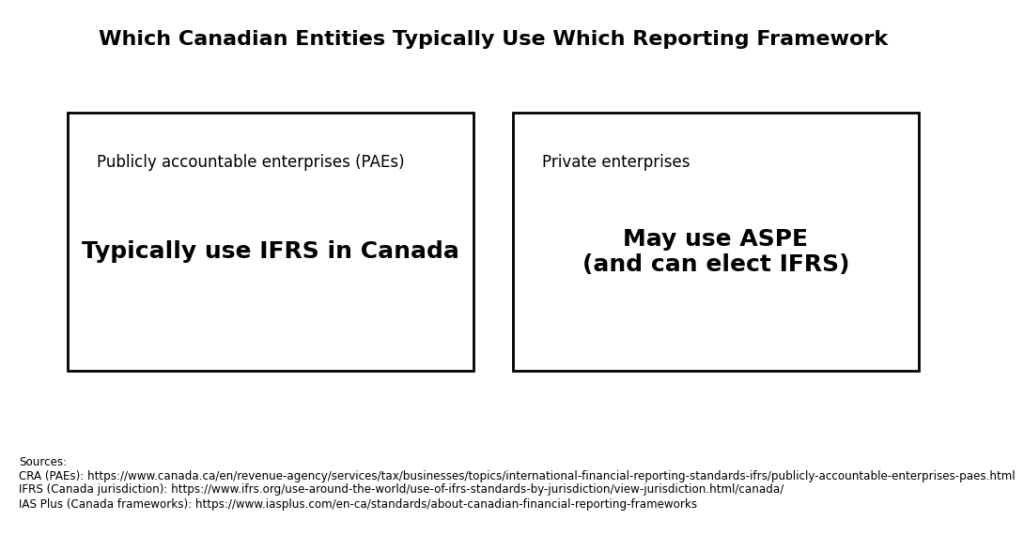

Do Canadian businesses have to use IFRS

In Canada, IFRS is required primarily for publicly accountable enterprises (PAEs). Many private enterprises can use ASPE instead, unless they elect IFRS for stakeholder needs (for example, group reporting, investors, or lenders).

What counts as a publicly accountable enterprise

CRA guidance generally describes a PAE as an entity that either:

- has issued, or is in the process of issuing, debt or equity instruments that trade in a public market, or

- holds assets in a fiduciary capacity for a broad group of outsiders as one of its primary businesses (for example many financial institutions).

Canada context: endorsement and Canadian GAAP

In Canada, the Accounting Standards Board endorses new and amended IFRS Accounting Standards for adoption as Canadian GAAP for publicly accountable enterprises.

IFRS vs ASPE: a practical comparison for many Ontario private companies

| Topic | IFRS (Part I) | ASPE (Part II) | Best fit often is |

| Complexity | Higher | Lower | ASPE for many private SMEs |

| Investor comparability | Strong globally | Mostly Canada-focused | IFRS if raising capital or reporting to global stakeholders |

| Disclosure depth | More extensive | Reduced | ASPE if users are mainly owners and lenders |

| Update cadence | More frequent | Generally less frequent | IFRS if you need alignment with group reporting |

Note: The right framework depends on who uses your statements and what they expect.

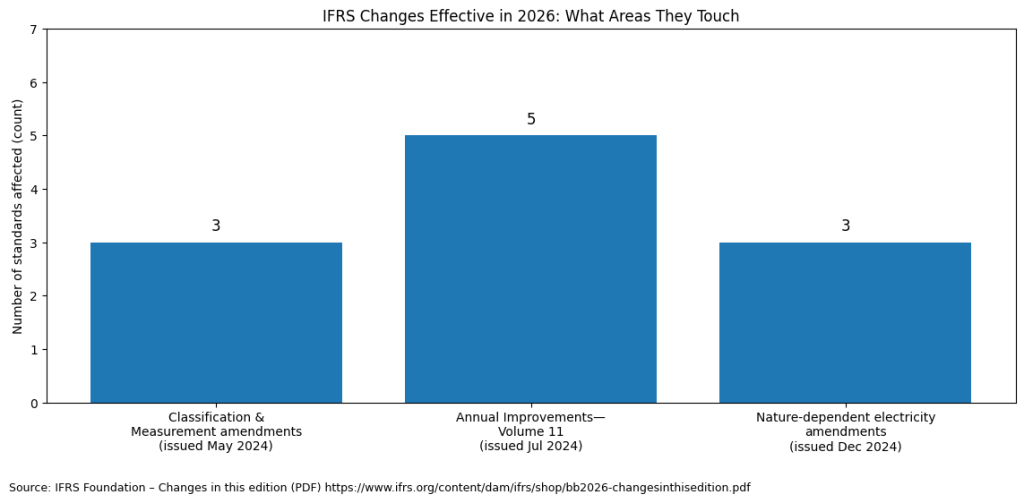

What IFRS standards changes are effective in 2026

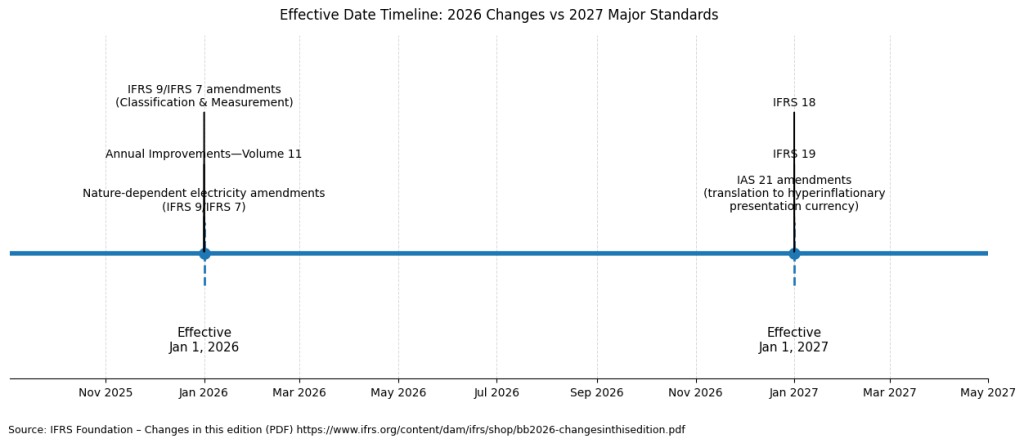

The IFRS changes effective from January 1, 2026 include:

- Amendments to IFRS 9 and IFRS 7 issued by the IASB in May 2024 that address classification and measurement practice issues and add disclosure requirements.

- Contracts Referencing Nature-dependent Electricity amendments to IFRS 9 and IFRS 7 issued in December 2024, effective in 2026.

- Annual Improvements to IFRS Accounting Standards, Volume 11, issued in July 2024 and effective in 2026.

What changed in IFRS 9 and IFRS 7 for 2026

The 2026 amendments to IFRS 9 and IFRS 7 were issued to make classification and measurement requirements more understandable and consistent, and to add new or updated disclosures. A key theme is better transparency for certain instruments, including those with contingent features and equity instruments designated at FVOCI.

Where these amendments show up for non-financial companies

Even if you are not a bank, IFRS 9 and IFRS 7 can matter if you have:

- loans receivable, promissory notes, or related-party financing arrangements

- investments in equity instruments (including FVOCI designations)

- complex contract terms that change cash flows

- liabilities settled through electronic payment systems

Practical impact checklist

For most Canadian businesses, the biggest risk is not the core accounting entry. It is the documentation and disclosure.

- Update your financial instruments inventory (what you have, how you classify it, what features matter).

- Update your IFRS 7 note templates and disclosure checklist.

- Document key judgments in a short memo that your auditor and lender can follow.

Nature-dependent electricity contracts: who should care

The IASB issued targeted amendments to IFRS 9 and IFRS 7 to help companies better report the financial effects of contracts where electricity production depends on nature, commonly structured as renewable power purchase agreements. These amendments are effective for annual periods beginning on or after January 1, 2026.

In plain English

This matters most if you have:

- renewable PPAs (wind, solar)

- contracts where quantities vary with weather conditions

- hedges tied to renewable electricity volumes or prices

If you operate large facilities or have long-term electricity procurement, you may encounter these terms even if you do not view yourself as an energy company.

Annual Improvements, Volume 11: small changes, real checklist impact

Annual Improvements are smaller amendments intended to clarify wording, fix inconsistencies, or simplify requirements. Volume 11 includes amendments affecting IFRS 1, IFRS 7, IFRS 9, IFRS 10, and IAS 7, effective for annual reporting periods beginning on or after January 1, 2026.

Practical impact

Annual Improvements commonly trigger:

- updates to disclosure checklists

- tweaks to accounting policy wording

- auditor questions if your templates are out of date

Treat them as a controlled checklist update, not a last-minute scramble.

Issued but not effective yet: what to prepare for in 2026

Even in 2026, you should plan for significant standards effective after 2026. For example, IFRS 18 is effective for annual reporting periods beginning on or after January 1, 2027. IAS 8 generally expects disclosure about standards issued but not yet effective when the impact could be material.

Why IFRS 18 matters

IFRS 18 introduces new requirements for presentation and disclosure in financial statements, including changes to how performance is communicated in the statement of profit or loss and how management-defined performance measures are disclosed.

IAS 8 disclosure reality

IAS 8 expects entities to disclose that they have not yet applied the new standard and to provide known or reasonably estimable information relevant to assessing the possible impact, or to state if the impact is not known or reasonably estimable.

How IFRS changes connect to audits, covenants, and tax

IFRS is financial reporting, not tax law. CRA taxable income is determined under the Income Tax Act and typically requires adjustments from accounting profit. However, IFRS changes can affect reported profit, equity, and subtotals that lenders and investors use, and can influence audit effort and timeline.

What tends to move in the real world:

- covenant calculations that reference IFRS measures

- lender questions when note disclosures change

- audit timelines when judgments are not documented

- internal reporting packages that rely on IFRS classifications

Step-by-step roadmap to handle IFRS 2026 changes

Start by identifying which 2026 amendments apply to your transactions, then determine whether the changes are disclosure-only or measurement-affecting. Update accounting policies and disclosure templates, run a dry-run note package, and document key judgments early. Finally, prepare IAS 8 issued-but-not-yet-effective disclosures for 2027 standards where relevant.

A practical implementation sequence

- Inventory what you have

- financial instruments: loans, investments, related-party balances

- group structure: subsidiaries and consolidation considerations

- cash flow statement presentation considerations

- any renewable electricity contracts

- Map amendments to real line items

- what could affect classification or measurement

- what is disclosure-only

- Update your toolset

- disclosure checklist and note templates

- accounting memos and documentation templates

- close procedures (who drafts, who reviews, what evidence is saved)

- Dry run early

- draft the updated notes mid-year or before audit planning

- Align with stakeholders

- auditor: interpretation-heavy items and documentation expectations

- lender: covenant definitions and any ratio reporting packs

Common mistakes businesses make with IFRS changes

Direct Answer: The most common issues are process problems: missing new disclosures, weak documentation of judgments, assuming amendments only affect financial institutions, and leaving IAS 8 future-standards disclosure vague. These issues can slow audits and create lender friction.

Common pitfalls:

- treating IFRS 9 and IFRS 7 changes as bank-only

- not updating year-end disclosure checklists for Annual Improvements

- missing nature-dependent electricity contract features in procurement agreements

- documenting judgments late, during audit fieldwork

- using boilerplate IAS 8 disclosures when the impact is likely material

Visual: Your 2026 IFRS change tracker

| Change area | Effective for annual periods beginning | Who should focus | What to update |

| IFRS 9 and IFRS 7 amendments (classification, measurement, disclosures) | Jan 1, 2026 | Any IFRS reporter with loans, investments, contingent features | Instrument inventory, accounting memos, disclosure templates |

| Nature-dependent electricity contracts (IFRS 9 and IFRS 7) | Jan 1, 2026 | Entities with renewable PPAs or variable-volume electricity contracts | Own-use assessment documentation, hedge docs, disclosures |

| Annual Improvements, Volume 11 | Jan 1, 2026 | All IFRS reporters | Disclosure checklist and template refresh |

| IFRS 18 (issued, not yet effective) | Jan 1, 2027 | Entities with external users and covenant reporting | Transition plan and IAS 8 disclosure prep |

FAQ

Which IFRS amendments are effective for annual periods beginning on or after January 1, 2026

The main changes effective for annual periods beginning on or after January 1, 2026 include amendments to IFRS 9 and IFRS 7 and the Annual Improvements to IFRS Accounting Standards, Volume 11. The IASB also issued amendments for contracts referencing nature-dependent electricity that are effective in 2026.

Do privately owned Ontario corporations need IFRS, or can they use ASPE

Many private enterprises in Canada can use ASPE. IFRS is required primarily for publicly accountable enterprises, though some private companies elect IFRS for lender, investor, or group reporting needs.

How do the 2026 IFRS changes affect year-end reporting, audits, and bank covenants

Most impacts show up in disclosures, documentation, and stakeholder questions. If ratios or disclosures change, lenders may request explanations. Audits can slow down if judgments are not documented early.

What IFRS changes are issued but not yet effective as of 2026

One major standard is IFRS 18, effective January 1, 2027. When impacts could be material, IAS 8 generally expects disclosure of issued-but-not-yet-effective standards and information relevant to assessing the possible impact.

What is a practical checklist to implement changes without overhauling everything

Focus on a controlled project: inventory relevant items, map amendments to those items, update templates, dry-run notes early, and document judgments for auditor and lender review.

Closing

The IFRS changes effective in 2026 are manageable when you treat them as a structured update: identify what applies, refresh checklists and templates, and document key judgments early.

If you want help mapping the 2026 amendments to your transactions, drafting clean disclosures, and preparing lender-ready reporting packages, speak with a qualified CPA and align with your auditor well before year end.

Sources and references

- IFRS.org: IASB news release on IFRS 9 and IFRS 7 amendments (May 2024): https://www.ifrs.org/news-and-events/news/2024/05/iasb-issues-amendments-cmfi-ifrs7-ifrs9/

- IFRS.org: IASB news release on nature-dependent electricity contracts amendments (Dec 2024): https://www.ifrs.org/news-and-events/news/2024/12/iasb-updates-accounting-standards-nature-dependent-electricity-contracts/

- IFRS.org: IASB Annual Improvements Volume 11 news (July 2024): https://www.ifrs.org/news-and-events/news/2024/07/iasb-issues-annual-improvements-ifrs-accounting-standards/

- IFRS.org: IFRS 18 effective date and overview: https://www.ifrs.org/issued-standards/list-of-standards/ifrs-18-presentation-and-disclosure-in-financial-statements/

- IFRS.org: IAS 8 standard text landing page: https://www.ifrs.org/content/dam/ifrs/publications/html-standards/english/2025/issued/ias8.html

- Canada.ca (CRA): Publicly accountable enterprises (PAEs) and IFRS requirement: https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/international-financial-reporting-standards-ifrs/publicly-accountable-enterprises-paes.html

- IFRS.org: Use of IFRS by jurisdiction, Canada: https://www.ifrs.org/use-around-the-world/use-of-ifrs-standards-by-jurisdiction/view-jurisdiction.html/canada/