Growth is exciting, until the back office starts to creak.

A second location, new staff, higher transaction volume, and more vendors can turn small errors into expensive messes: missed payroll remittances, duplicate payments, inventory that disappears, or GST/HST charged incorrectly. The painful part is that these issues often show up late, during a CRA review, at year end, or when a lender asks for clean financials.

Internal controls are simple, repeatable steps that help your Small Business prevent mistakes, detect problems early, and prove compliance. For Canadian small businesses, strong controls often reduce CRA stress by improving recordkeeping and ensuring GST/HST and payroll deductions are handled correctly. They also support growth by tightening purchasing, protecting cash flow, and producing cleaner financial statements for lenders and investors. You do not need a big-company internal audit team. Most SMEs get strong results from a short control checklist, clear approvals, and monthly reviews.

Internal controls are how you keep momentum without losing control. They are not about distrust or paperwork. They are about making sure the right things happen the same way every time, so your numbers are reliable, compliance risk drops, and you can scale with confidence.

COSO, one of the most widely used internal control frameworks, is explicit that controls create value beyond compliance and financial reporting, including helping organizations grow on a sustained basis with confidence and integrity.

Quick Start: Pick Your Path

Use this guide to jump to what fits your setup.

- Sole proprietor or partnership (you do most things yourself)

Focus on: cash controls, invoicing, and tax-ready records. - Incorporated business

Focus on: approvals, delegation, and a clean month end. - Employer (payroll)

Focus on: remittance deadlines, T4 accuracy, and payroll review steps. - GST/HST registrant

Focus on: tax coding, place-of-supply basics, and invoice support. - Scaling fast (new location, more staff, new software)

Focus on: standard processes and monthly monitoring. - Concerned about fraud or theft

Focus on: payment controls, access controls, and independent review.

What are internal controls for a Small Business

Internal controls are the policies and routine checks that help you reach objectives in operations, reporting, and compliance. In plain English, they are steps that prevent errors, catch problems early, and create proof for audits. Good controls help small businesses grow by making results more predictable and reducing surprise costs.

Controls, defined in simple terms

A control can be as simple as:

- only one person can set up a new vendor, and it requires approval

- invoices are numbered and matched to deposits

- payroll is reviewed before it is finalized

- bank accounts are reconciled monthly

COSO defines internal control as a process designed to provide reasonable assurance about achieving objectives related to operations, reporting, and compliance. The word reasonable matters. Controls reduce risk. They do not eliminate it.

Why Canadian small businesses should care

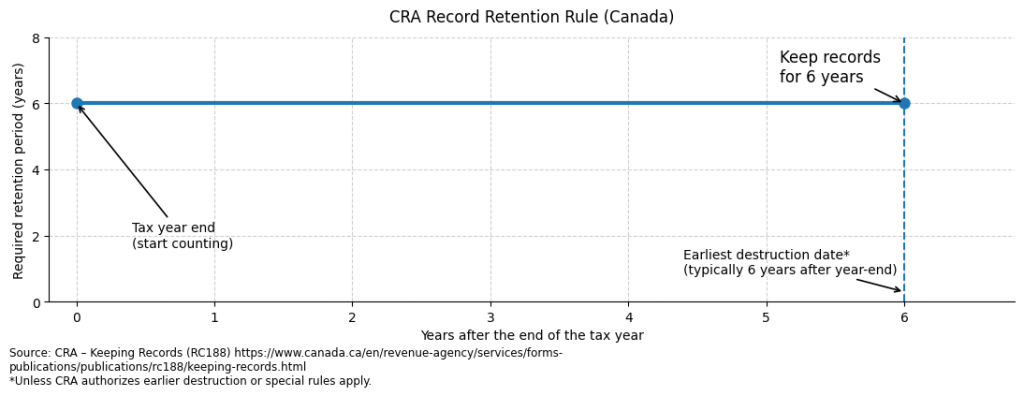

Even if you are not thinking about audit, CRA expects adequate records. CRA guidance states that, generally, you must keep required records and supporting documents for six years from the end of the last tax year they relate to, unless CRA allows earlier destruction.

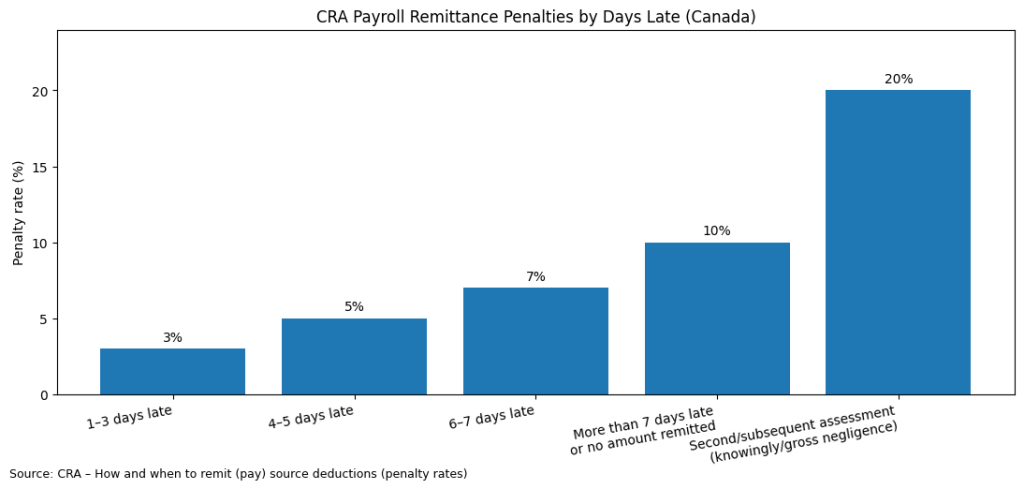

If you are an employer, remittance timing matters. CRA’s payroll guidance outlines late remittance penalties that escalate based on how late the payment is, including higher penalties in repeat or gross negligence situations.

Translation for operators: controls are not theoretical. They are how you avoid penalties, protect cash flow, and reduce year end cleanup.

How internal controls turn into growth

Direct Answer: Controls create growth by making your business easier to manage and finance. They reduce cash leaks (errors, duplicate payments, uncollected invoices), improve the quality of financial statements, and support faster decision-making. Strong controls also make compliance predictable, so you spend less time fixing problems and more time serving customers.

Growth levers controls improve

- Cash flow: tighter invoicing and collections, fewer surprise outflows

- Margins: better purchasing discipline and expense coding

- Speed: repeatable processes mean faster onboarding and fewer ad hoc decisions

- Financing: lenders prefer reliable books and documented processes, which reduces key person risk

- Resilience: fewer crises from missed remittances or missing receipts

Which controls matter most for Canadian Small Business compliance

Start with controls that protect the areas CRA and provincial programs care about most: recordkeeping, payroll deductions, and GST/HST. Make sure you can support every claim on your return with documentation, remit payroll deductions by the due date, and charge the correct GST/HST rate based on place-of-supply rules.

1) Recordkeeping controls

What CRA expects is simple: records that support what you filed, and retention for the required period.

Controls to implement:

- a consistent filing rule (one place, one naming convention)

- a monthly missing-receipt follow up

- standardized naming for invoices and vendor bills

- read-only storage or a locked period after month end close

Evidence to save: a monthly “close” folder that includes bank recs, sales summaries, and key tax reports.

2) Payroll controls (Canada, Ontario reality)

If you withhold payroll deductions (income tax, CPP, EI), timing matters. CRA lists late-remittance penalties that increase with lateness and can be higher for repeat or gross negligence situations.

Controls to implement:

- a payroll calendar with due dates and a backup approver

- a preview payroll register review before finalizing

- a separate approval step before pay runs

- remittance confirmations saved each pay period

Ontario note: many employers also manage Employer Health Tax and WSIB premiums. Assign a clear owner and include reconciliations in your monthly close.

3) GST/HST controls

Most GST/HST problems for SMEs come from:

- charging the wrong tax rate (place of supply)

- missing support for input tax credits

- inconsistent tax coding in bookkeeping

CRA’s place-of-supply guidance helps determine whether to charge GST or HST based on where a supply is made.

Controls to implement:

- standard tax codes in accounting software

- an exception list (zero-rated, exempt, out-of-province)

- a monthly reasonableness check (sales vs tax collected, compared to prior months)

Do small businesses need internal audit

Most small businesses do not need a formal internal audit department. Instead, you want periodic independent checks, such as owner review, an external bookkeeper, or a CPA-led controls check up. The goal is the same: test whether controls work, then fix weak points before they become costly.

A helpful mental model is the Institute of Internal Auditors’ Three Lines Model, which separates day-to-day management activities from independent assurance. Even if you are small, you can borrow the idea by adding an independent review step each month or quarter.

A practical framework that will not overwhelm your team

Use a simple framework: define your top risks, assign an owner, then add one preventive control and one detective control for each risk. Preventive controls stop problems. Detective controls catch them fast. Keep controls lightweight, documented, and tied to a monthly review so they do not fade away.

The Top 8 risks checklist most SMEs can use

Choose the risks that match your business:

- cash deposits not recorded or deposited late

- customers not billed, or billed incorrectly

- expenses coded incorrectly (tax and reporting errors)

- duplicate vendor payments

- payroll errors or late remittances

- GST/HST charged incorrectly

- inventory shrinkage or job-cost leakage

- unauthorized access to bank, cards, or software

Visual: Preventive vs detective vs corrective controls

| Control type | What it does | Small Business example | Works best when |

| Preventive | Stops errors before they happen | Approval required for new vendors; spending limits | You are hiring and delegating |

| Detective | Finds issues quickly | Monthly bank reconciliation; variance review | Transaction volume is rising |

| Corrective | Fixes and prevents repeat issues | Update a checklist after an error; retrain staff | You had a near miss or repeat issue |

Step by step roadmap to implement internal controls

Implement controls in four sprints: map your processes, choose a few high-impact controls, document them in plain language, then monitor monthly. Start with cash, payroll, and tax-related controls because mistakes there are expensive. Expand controls only after the basics are working consistently.

Sprint 1: Map your money flow

Write down, on one page:

- how money comes in (quotes to invoices to deposits)

- how money goes out (purchase to bill to payment)

- who can change bank details, vendor info, and payroll

Sprint 2: Pick minimum viable controls

Choose 1 to 2 controls for each flow.

Revenue

- invoice numbering and deposit matching

Purchasing

- approval thresholds and vendor onboarding approval

Payments

- payment batch approval and restricted bank access

Payroll

- pre-payroll review and remittance confirmation saved

Taxes

- monthly GST/HST check and a record retention policy

Sprint 3: Document and train

Keep documentation short:

- who does it

- when they do it

- what evidence is saved (report, PDF, screenshot)

Sprint 4: Monitor monthly (this is where growth happens)

If you only do one control meeting per month, review:

- bank reconciliation

- aged receivables

- payroll remittances submitted

- GST/HST reasonableness check

- unusual transactions and new vendors

Fraud and cash leaks: why controls protect revenue

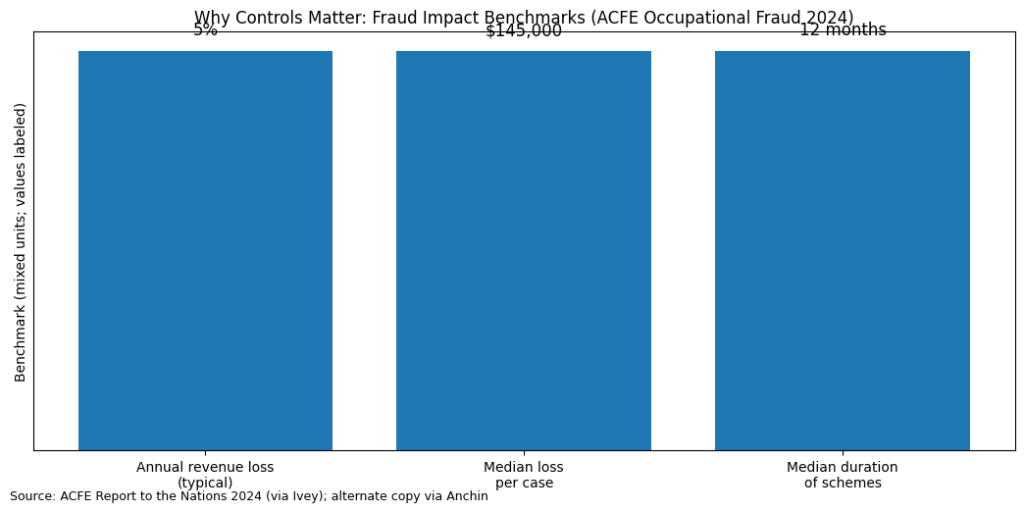

Direct Answer: Controls do not just prevent penalties. They protect revenue. The ACFE’s 2024 Report to the Nations notes a long-running benchmark that organizations lose about 5% of revenue to fraud, and reports a median loss of $145,000 with a median duration of 12 months.

For a Small Business, that kind of leak is not theoretical. It is often the difference between hiring, investing, and stalling.

Practical anti-fraud controls that fit SMEs:

- separate the person who approves spending from the person who pays

- lock down banking access and require multi-factor authentication

- require documentation for reimbursements

- review the vendor list quarterly

- scan for round-number payments, unusual timing, and new payees

Common mistakes that make internal controls fail

Direct Answer: Controls fail when they are undocumented, too complex, or not reviewed. The most common breakdowns are weak recordkeeping, late payroll remittances, inconsistent GST/HST coding, and overly broad access in banking and accounting tools. Fixing these does not require a big team. It requires clear ownership and monthly follow through.

Common failure points:

- no clear record retention policy, receipts scattered across inboxes

- bank reconciliation skipped “just this month,” then it becomes three months

- payroll remittances missed because no backup person owns the deadline

- GST/HST coded inconsistently, then returns become guesswork

- vendor setup has no approval, increasing risk of errors and fraud

- too many admin permissions in banking and accounting apps

- controls exist in someone’s head, not on paper

FAQ

What are internal controls in plain English

Internal controls are routine steps that keep your business on track, like approvals, reconciliations, and documented processes. They help prevent errors, detect issues early, and prove compliance. They are designed to provide reasonable assurance that your operational, reporting, and compliance goals are being met.

What are the best internal controls for a very small business with one owner

Focus on controls that do not require extra staff: monthly bank reconciliation, invoice-to-deposit matching, receipt capture, and a monthly tax check (GST/HST and payroll if applicable). CRA expects adequate records and retention, so a clean record system is a strong starting point.

How do internal controls reduce CRA payroll penalties

Controls reduce penalties by preventing late remittances and documentation gaps. CRA outlines escalating penalties based on how late a remittance is, including higher penalties in repeat or gross negligence situations. A payroll calendar, backup approver, and proof-of-payment filing are simple controls that protect you.

Do I need an internal audit if I am a small business

Usually no. Most SMEs benefit more from an owner-led monthly review or a CPA-led controls check up than from a full internal audit function. The goal is independent verification that your controls are working.

How do I avoid charging the wrong GST/HST rate when I sell across Canada

Use CRA’s place-of-supply guidance to determine where the supply is made and which rate applies. Then build that logic into invoicing using standard tax codes, an exception list, and monthly checks.

How long do I need to keep small business records in Canada

CRA’s general rule is six years from the end of the last tax year the records relate to, unless CRA permits earlier destruction. A simple control is to store records digitally with consistent naming and a finalized-period archive.

What is the fastest way to start if my books are already messy

Start with one clean monthly close: reconcile bank and credit cards, lock down access, standardize tax codes, and fix receipt capture. Then add a monthly review checklist and stick to it.

Closing: the key takeaway

Internal controls are not red tape. They are how a Small Business stays compliant, produces reliable numbers, and scales without constant fire drills.

If you want help building a right-sized controls checklist, especially around payroll, GST/HST, and year-end documentation, speak with a qualified accounting professional. Talk to Clearwealth Accounting Advisors about a controls check up for your Small Business.

Sources and references

Canada Revenue Agency (CRA) — Keeping Records (RC188). Confirms the general rule to keep records for six years (with exceptions and CRA authorization rules).

https://www.canada.ca/en/revenue-agency/services/forms-publications/publications/rc188/keeping-records.html

CRA — How and when to remit (pay) source deductions (due dates + penalties). Lists payroll remittance penalty tiers including 3%, 5%, 7%, 10%, and 20% in certain repeat/knowingly/gross negligence situations.

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/payroll/remitting-source-deductions/how-when-remit-due-dates.html

CRA — GST/HST: Charge and collect (place of supply). Supports the framework for determining whether to charge GST or HST based on place-of-supply rules.

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/gst-hst-businesses/charge-collect-place-supply.html

COSO — Internal Control. Supports positioning that internal controls provide value beyond compliance (helping achieve objectives with confidence/integrity; “reasonable assurance” framing).

https://www.coso.org/internal-control

Institute of Internal Auditors (IIA) — The IIA’s Three Lines Model (PDF). Supports the concept of independent assurance and role separation (operations/management, oversight, independent assurance).

https://www.theiia.org/globalassets/documents/resources/the-iias-three-lines-model-an-update-of-the-three-lines-of-defense-july-2020/three-lines-model-updated-english.pdfACFE — Report to the Nations 2024 (Occupational Fraud) (PDF copy). Supports benchmarks commonly cited from the 2024 report, including ~5% revenue loss estimate, $145,000 median loss, and 12-month median duration.

https://www.ivey.uwo.ca/media/kjljj5cy/2024-report-to-the-nations.pdf

(Alternate copy) https://www.anchin.com/wp-content/uploads/2024/08/2024-ACFE-Occupational-Fraud-Report.pdf