Disclaimer: This article is general information only and is not legal, investment, or tax advice. International tax results depend on your residency status, ownership structure, treaty position, and the type of foreign asset or income involved.

At a Glance

What changed: Canadian residents are generally taxed on worldwide income, and overseas investing can trigger both income reporting and separate foreign-asset reporting obligations.

Who is affected: Individuals, corporations, and business owners in Canada with foreign accounts, offshore securities, overseas real estate, or other specified foreign property.

What to watch most closely: Residency status, the T1135 cost threshold, foreign tax credit eligibility, exchange-rate conversion, and late-filing penalties.

If you are a Canadian tax resident, you are generally taxed on your worldwide income, including many types of overseas investment income. If the total cost amount of your specified foreign property is more than $100,000 at any time during the year, you may also have to file Form T1135. Foreign taxes paid may qualify for a foreign tax credit, but only if the income is properly reported on your Canadian return and converted to Canadian dollars using an acceptable exchange rate. The most common costly mistakes are assuming tax paid overseas ends the Canadian reporting obligation, missing the T1135 threshold, using the wrong exchange-rate approach, and claiming a foreign tax credit without the right records.

Why Overseas Investment Tax Planning Matters

Overseas investing often looks simple at the start. You buy foreign shares through a brokerage platform, hold a bank account in another country, or collect rent from a property outside Canada. The complexity usually appears later, when filing season arrives and the CRA expects reporting that many investors did not realize applied.

That is where small mistakes become expensive. Someone may have paid foreign withholding tax and assume the income does not need to be reported again in Canada. Another taxpayer may look only at year-end balances and miss the fact that their specified foreign property exceeded the reporting threshold earlier in the year. A business owner may focus on return on investment but overlook T1135, foreign tax credit forms, exchange-rate conversion, or extended reassessment exposure. CRA guidance is clear that late or missing foreign reporting can carry significant penalties, as explained in CRA’s pages on foreign reporting penalties and the Foreign Income Verification Statement.

This is why tax planning matters here. The issue is not only how much foreign income you earned. It is whether you reported it correctly, converted it correctly, and filed every required information form on time.

Step One: Confirm Canadian Tax Residency First

Before looking at foreign income or T1135, confirm whether you are a resident of Canada for tax purposes. CRA says your Canadian income tax obligations depend on residency status, and residence is determined by the full facts of your situation, including residential ties and treaty tie-breaker rules where relevant, as outlined in CRA’s folio on Determining an Individual’s Residence Status.

That matters because the worldwide-income rule starts with residency. If you are a Canadian tax resident, the default position is that your foreign income belongs in your Canadian tax picture. If you recently moved to Canada, left Canada, or have ties in more than one country, the residency analysis comes first. Getting that step wrong can distort everything that follows.

Do Canadian Residents Have to Report Overseas Investment Income?

Yes. CRA’s foreign tax credit folio states that residents of Canada are generally taxed on their worldwide income, as explained in Income Tax Folio S5-F2-C1, Foreign Tax Credit. That means foreign interest, foreign dividends, foreign rental income, and taxable capital gains from overseas assets may still need to be reported in Canada even if tax was already paid abroad.

This is the rule many taxpayers miss first. Paying foreign tax does not usually cancel the Canadian reporting obligation. It only means that, after reporting the income in Canada, you may need to review whether a foreign tax credit, treaty exemption, or other form of relief is available. CRA’s line 40500 guidance confirms that foreign tax credits are calculated after the foreign income is reported on the Canadian return.

For Ontario residents, the practical effect is that both federal and provincial calculations may be affected. CRA says individuals may need Form T2209 for the federal foreign tax credit and Form 428 for the provincial or territorial credit calculation.

What Counts as Overseas Investment Income?

Overseas investment income can include:

- interest from a foreign bank account

- dividends from non-Canadian shares

- income from foreign brokerage or fund holdings

- rental income from real estate outside Canada

- gains on the sale of foreign investments

- in some cases, holdings in foreign corporations, trusts, or entities that can trigger added reporting beyond the standard return

The exact tax treatment depends on the asset type and how the income arises, but the compliance principle is consistent: report the income, convert it to Canadian dollars, support it with records, and check whether a separate information form is required. CRA’s foreign reporting pages make clear that foreign reporting is broader than one form and can apply to individuals, corporations, trusts, and partnerships.

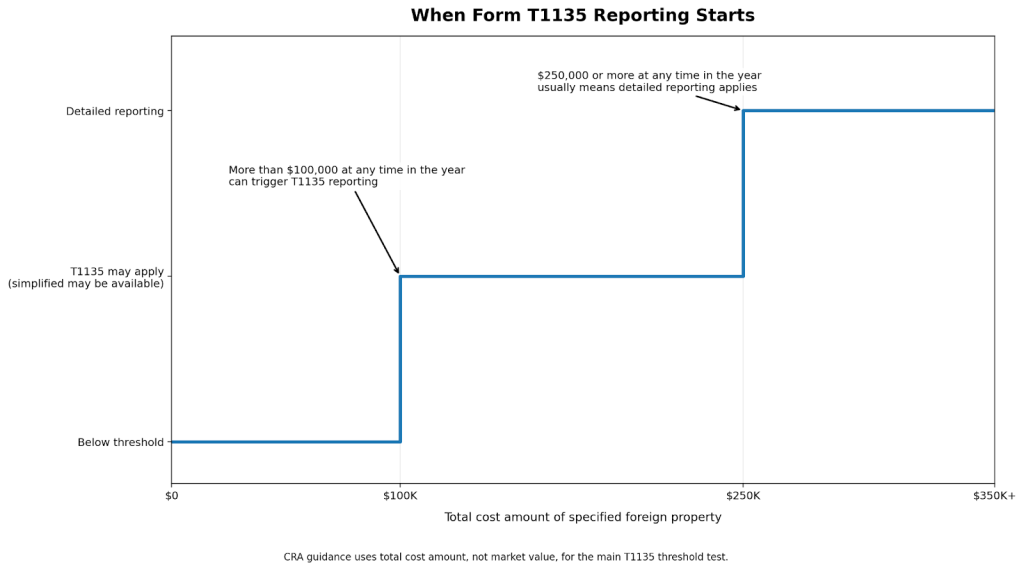

When Do You Have to File Form T1135?

You may have to file Form T1135, Foreign Income Verification Statement, if the total cost amount of your specified foreign property is more than $100,000 at any time during the year. This is a reporting form, not a tax-calculation form, and it applies separately from reporting the income itself.

This is one of the most important triggers for overseas investors in Canada.

Two points matter here:

First, the threshold is based on total cost amount, not market value. So investors who check only fair market value or only one account can easily get the test wrong. CRA’s T1135 Q&A specifically addresses the cost amount threshold.

Second, the threshold applies if you crossed it at any time in the year. You can fall below $100,000 by year-end and still have a filing obligation if you were over the threshold earlier. CRA says exactly that in its T1135 reporting guidance.

CRA also uses a two-tier reporting approach. If your specified foreign property was more than $100,000 but remained under $250,000 throughout the year, simplified reporting may apply. If the total cost reached $250,000 or more at any time, detailed reporting is generally required.

What Is the Biggest Reporting Mistake Overseas Investors Make?

The biggest mistake is confusing “no extra tax owing” with “no reporting required.”

A taxpayer may owe little or no additional Canadian tax after foreign tax credits. That does not mean the reporting rules disappear. The CRA issue is often not whether you ultimately owe more tax. It is whether you reported the foreign income and filed the required forms properly and on time.

The most common traps are:

- assuming foreign tax withheld means nothing needs to be reported in Canada

- missing the T1135 threshold because smaller holdings add up

- using market value instead of cost amount for the threshold test

- failing to keep statements that support cost, income, and tax paid

- using inconsistent exchange rates

- ignoring added corporate or trust reporting

- assuming reassessment exposure ends on the normal timeline

CRA notes that the reassessment period can be extended in certain foreign-reporting situations, including cases involving late T1135 filing and unreported income from specified foreign property, as discussed in the CRA pages on the Foreign Income Verification Statement and penalties.

Can You Claim a Foreign Tax Credit in Canada?

Often, yes. CRA says you may be able to claim a federal foreign tax credit for foreign income or profits tax paid on income earned outside Canada and reported on your Canadian return, as explained on CRA’s line 40500 – Federal foreign tax credit page.

This is where proper tax planning prevents both overpayment and underreporting.

For individuals, CRA says to complete Form T2209 and enter the result on line 40500 of the return. CRA also says you may need Form 428 for the provincial or territorial foreign tax credit calculation.

For corporations, CRA has separate guidance on provincial and territorial foreign tax credits, including reference to Schedule 21 and related corporate schedules. That matters for Ontario corporations that hold investments abroad. See CRA’s page on provincial and territorial foreign tax credits for corporations.

The key rule is simple: the foreign tax credit may help reduce double taxation, but it does not replace the need to report the foreign income first. If the income is missing from the Canadian return, the credit position is weaker from the start.

How Do Exchange Rates Affect Foreign Income Reporting?

Foreign income and foreign taxes generally must be converted to Canadian dollars for Canadian reporting. CRA says a rate acceptable to the CRA is generally one quoted by the Bank of Canada. For some recurring amounts, CRA accepts the average annual rate; for amounts arising on specific dates, the rate in effect on the day the amount arises is generally used. See CRA’s guidance on exchange rates and the folio on income tax reporting currency.

This matters more than many investors expect.

If you receive U.S. dividends, sell overseas shares, or pay tax in a foreign currency, you cannot simply leave those figures in the original currency on your Canadian return. Exchange-rate handling affects:

- the amount of income reported

- the amount of foreign tax credit claimed

- the consistency between your return and supporting records

Sloppy conversion can create a mismatch between your tax return, T1135, and your brokerage or bank records. That does not automatically mean the tax result is wrong, but it can make the file harder to defend.

Do the Same Rules Apply to Individuals, Corporations, and Business Owners?

The core principles are similar: report foreign income, review foreign reporting forms, and test whether a foreign tax credit applies. The structure matters because the forms, schedules, and administrative burden differ.

For individuals, the common pattern is:

- worldwide income reporting on the personal return

- possible T1135 filing

- T2209 and provincial credit calculations where foreign tax was paid

For corporations, the same overseas investment can create a more complex filing picture:

- foreign income still matters

- T1135 may still apply

- corporate foreign tax credit schedules may apply instead of the personal forms

- bookkeeping and year-end files need tighter coordination

CRA’s foreign reporting pages explicitly cover individuals, corporations, trusts, and partnerships. CRA’s corporate foreign tax credit guidance confirms that corporations have their own provincial and territorial credit rules and schedules.

That is why overseas investing and small-business tax planning often overlap. A corporation may improve administrative separation in some cases, but it can also increase compliance complexity.

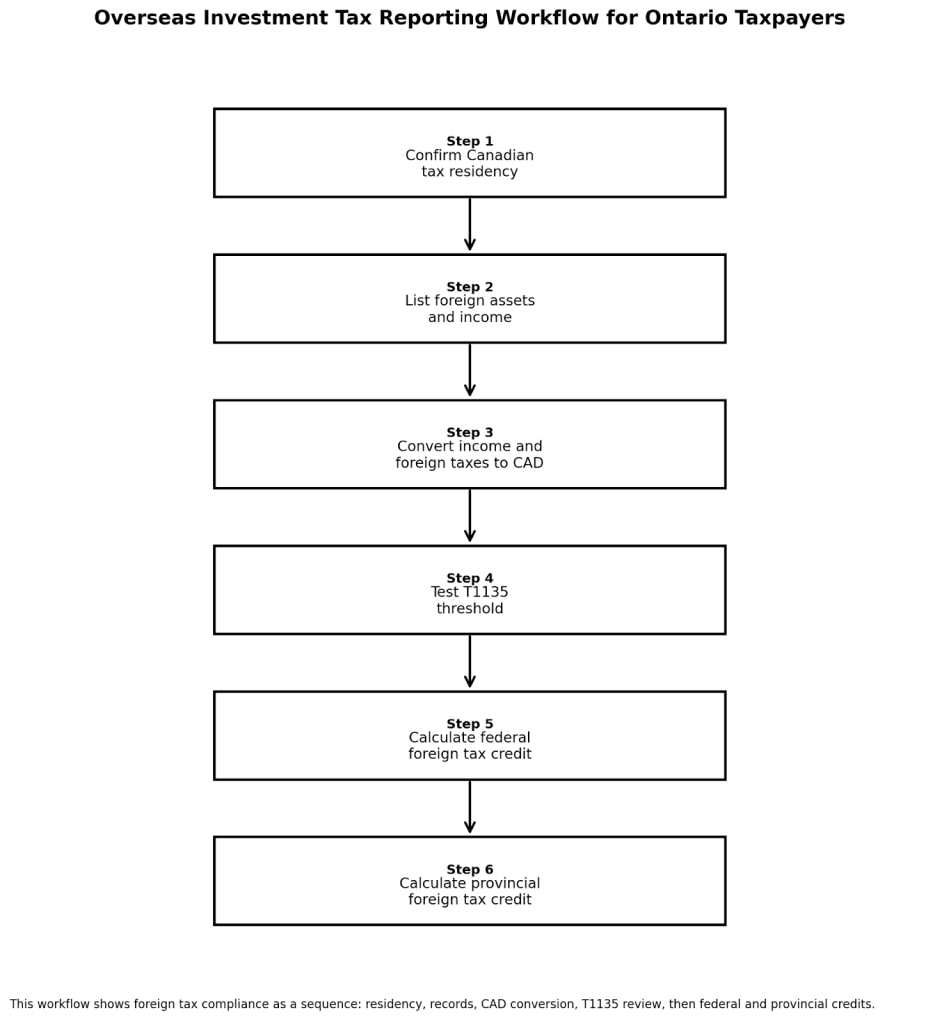

A Practical Tax-Planning Roadmap for Overseas Investors

The safest approach is to identify foreign holdings early, track cost and income during the year, and review reporting before filing season.

Use this roadmap:

- Confirm your Canadian tax residency.

- List every foreign account, security, property, and entity interest.

- Track the cost amount of specified foreign property through the year.

- Record all foreign income earned and foreign tax withheld.

- Convert income and taxes to Canadian dollars using an acceptable rate.

- Check whether Form T1135 is required.

- Review whether a foreign tax credit is available federally and provincially.

- If you are a business owner, confirm whether the investment is held personally or through a corporation.

- Keep statements, slips, transaction history, and exchange-rate support together.

- Review prior years if you suspect something was missed.

This is where good tax planning earns its value. In this area, prevention is usually cheaper than repair.

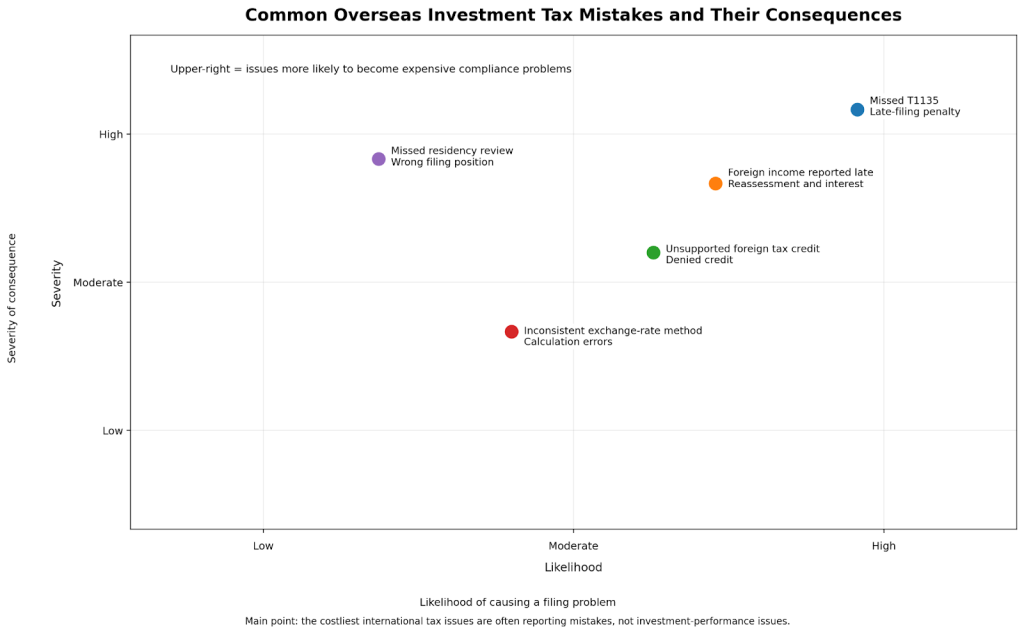

Common Mistakes Overseas Investors Need to Avoid

Most expensive mistakes here are compliance mistakes, not investment mistakes.

Missing Form T1135 is one of the biggest. CRA says significant penalties can apply for failure to file by the deadline or for false statements and omissions. The standard late-filing penalty is generally $25 per day, minimum $100, maximum $2,500, and more severe penalties may apply in more serious cases or after long delays, as described in CRA’s penalties and table of penalties.

Other common mistakes include:

- using the wrong threshold test

- claiming a foreign tax credit without reporting the income

- ignoring the provincial foreign tax credit calculation

- keeping weak records for cost, tax paid, and exchange rates

- forgetting that residency changes can alter the whole analysis

- assuming reassessment exposure ends quickly when foreign reporting is involved

FAQ

Do I have to report foreign investment income in Canada if tax was already withheld abroad?

Usually yes. If you are a Canadian tax resident, foreign investment income generally still has to be reported on your Canadian return. Foreign tax paid may support a credit, but it does not usually eliminate the Canadian reporting obligation, as explained in CRA’s foreign tax credit folio.

When is Form T1135 required?

Form T1135 may be required when the total cost amount of your specified foreign property is more than $100,000 at any time in the year. It is separate from the income tax return itself. See CRA’s T1135 reporting guidance.

Is the T1135 threshold based on market value?

No. The threshold test is based on total cost amount, not fair market value. CRA explains this in its T1135 questions and answers.

Can Ontario taxpayers claim both federal and provincial foreign tax relief?

Often yes. CRA says individuals may need Form T2209 for the federal credit and Form 428 for the provincial or territorial calculation. See CRA’s line 40500 guidance.

What happens if I miss Form T1135?

CRA says significant penalties may apply, and foreign-reporting issues can also increase reassessment risk. See the CRA pages on the Foreign Income Verification Statement,penalties, and questions and answers about penalties.

Do I need to use Bank of Canada exchange rates?

CRA says an exchange rate acceptable to the CRA is generally one quoted by the Bank of Canada, and the approach used should be consistent where relevant. See CRA’s exchange-rate guidance.

Does this matter for small business owners with overseas investments?

Yes. The foreign income, reporting forms, and foreign tax credit rules can still apply whether the investment is held personally or in a corporation, and corporations may have different schedules and more coordination requirements. See CRA’s page on provincial and territorial foreign tax credits for corporations.

Final Takeaway

The biggest tax planning mistake overseas investors make is assuming foreign investing is only an investment issue. In Canada, it is also a reporting issue.

The safest sequence is simple: start with residency, then apply the worldwide-income rule, then test for T1135 and other foreign reporting, then review foreign tax credits and exchange-rate treatment. That order reduces both overpayment risk and penalty risk.

If you have foreign accounts, offshore securities, overseas real estate, or investments held through a corporation, review the filing before the deadline rather than after CRA raises questions.

If you want help organizing your foreign income reporting or reviewing missed filings, speak with a Clearwealth accounting professional before you submit your return.

If you want, I can also insert the chart images directly into this copy-paste version the same way I did for your Florida blog.

Sources and References

- Canada Revenue Agency, Form T1135

https://www.canada.ca/en/revenue-agency/services/forms-publications/forms/t1135.html - Canada Revenue Agency, Form T1135 reporting for 2015 and later tax years

https://www.canada.ca/en/revenue-agency/services/tax/international-non-residents/information-been-moved/foreign-reporting/form-t1135-reporting-2015-later-tax-years.html - Canada Revenue Agency, Questions and answers about Form T1135

https://www.canada.ca/en/revenue-agency/services/tax/international-non-residents/information-been-moved/foreign-reporting/questions-answers-about-form-t1135.html - Canada Revenue Agency, Foreign Income Verification Statement

https://www.canada.ca/en/revenue-agency/services/tax/international-non-residents/information-been-moved/foreign-reporting/foreign-income-verification-statement.html - Canada Revenue Agency, International and non-resident taxes

https://www.canada.ca/en/revenue-agency/services/tax/international-non-residents-tax.html - Canada Revenue Agency, Line 40500 – Federal foreign tax credit

https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/about-your-tax-return/tax-return/completing-a-tax-return/deductions-credits-expenses/line-40500-federal-foreign-tax-credit.html - Canada Revenue Agency, Form T2209

https://www.canada.ca/en/revenue-agency/services/forms-publications/forms/t2209.html - Canada Revenue Agency, Form T2036

https://www.canada.ca/en/revenue-agency/services/forms-publications/forms/t2036.html - Canada Revenue Agency, Provincial and territorial foreign tax credits for corporations

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/corporations/provincial-territorial-corporation-tax/provincial-territorial-foreign-tax-credits.html - Canada Revenue Agency, Income Tax Folio S5-F2-C1, Foreign Tax Credit

https://www.canada.ca/en/revenue-agency/services/tax/technical-information/income-tax/income-tax-folios-index/series-5-international-residency/folio-2-foreign-tax-credits-deductions/income-tax-folio-s5-f2-c1-foreign-tax-credit.html - Canada Revenue Agency, Income Tax Folio S5-F1-C1, Determining an Individual’s Residence Status

https://www.canada.ca/en/revenue-agency/services/tax/technical-information/income-tax/income-tax-folios-index/series-5-international-residency/folio-1-residency/income-tax-folio-s5-f1-c1-determining-individual-s-residence-status.html - Canada Revenue Agency, Income Tax Reporting Currency

https://www.canada.ca/en/revenue-agency/services/tax/technical-information/income-tax/income-tax-folios-index/series-5-international-residency/series-5-international-residency-folio-4-foreign-currency/income-tax-folio-s5-f4-c1-income-tax-reporting-currency.html - Canada Revenue Agency, Functional currency

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/corporations/functional-currency.html - Canada Revenue Agency, Penalties

https://www.canada.ca/en/revenue-agency/services/tax/international-non-residents/information-been-moved/foreign-reporting/penalties.html - Canada Revenue Agency, Table of penalties

https://www.canada.ca/en/revenue-agency/services/tax/international-non-residents/information-been-moved/foreign-reporting/table-penalties.html - Canada Revenue Agency, Questions and answers about penalties

https://www.canada.ca/en/revenue-agency/services/tax/international-non-residents/information-been-moved/foreign-reporting/questions-answers-about-penalties.html