Last Updated: March 2026

Disclaimer: This article is general information, not legal, tax, or accounting advice. The right structure depends on your income, risk, province, industry, and how you plan to pay yourself.

Should I stay self-employed or incorporate my business in Canada in 2026?

There is no single best choice for everyone. Staying self-employed is usually simpler and cheaper to run, while incorporation often makes more sense when profits are consistently left in the business, legal liability needs are higher, or long-term growth planning matters. In Canada, a sole proprietor reports business income on a personal tax return, while a corporation files its own T2 return and is treated as a separate legal entity. CRA says sole proprietors report business income on their T1, while resident corporations generally must file a T2 every tax year, even if there is no tax payable.

For many Ontario owners, the real decision comes down to three things: tax deferral potential, administrative burden, and risk exposure. That is why the better question is not “Which structure is best?” but “Which structure fits the stage, profit level, and risk profile of my business right now?”

Why this decision matters in 2026

Choosing the wrong structure can create avoidable stress. You might miss filing deadlines, register the wrong CRA accounts, pay for bookkeeping you do not need yet, or stay personally exposed to business debt when your risk level has changed. On the other side, incorporating too early can add T2 filings, corporate recordkeeping, payroll setup, and accounting costs before the tax benefits are meaningful. CRA’s current guidance confirms that corporations generally must file every year, and that businesses may also need separate program accounts for GST/HST, payroll, and corporation income tax.

For Ontario business owners in 2026, this is not just a tax decision. It also affects GST/HST registration, payroll setup, how you pay yourself, whether you need a Business Number, and how much compliance work you will carry every year. CRA notes that incorporated businesses need a BN, while unincorporated businesses usually only need one when they register for CRA program accounts such as GST/HST or payroll.

Quick Start: Pick Your Path

Use this checklist to find the section that fits you:

- You are freelancing, consulting, or selling services under your own name: start with the self-employed sections.

- You are earning more than you need personally and want to leave cash in the business: read the incorporation tax section.

- You plan to hire staff or pay yourself a salary: read the payroll section.

- You are worried about contracts, lawsuits, or business debt: read the liability section.

- You are near or above $30,000 in taxable sales: read the GST/HST section.

- You want the lowest admin burden: compare filing and compliance first.

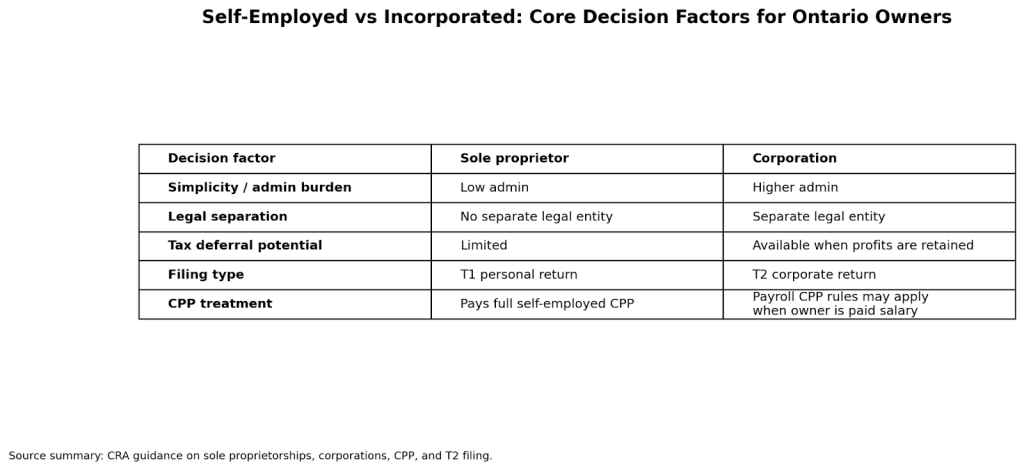

What is the difference between self-employed and incorporated?

A self-employed person usually operates as a sole proprietor. In that structure, the business is not separate from the owner for legal and tax purposes. CRA’s sole proprietorship guidance says a sole proprietor pays taxes by reporting business income or loss on a T1 income tax and benefit return.

An incorporated business is different. A corporation is a separate legal entity. It can earn income, file its own return, own assets, and continue after ownership changes. CRA says resident corporations generally must file a T2 each tax year, even if inactive or if no tax is payable.

That means the practical choice is this: do you want simplicity and lower ongoing admin, or do you need legal separation, better retained-earnings flexibility, and a structure that supports growth, partners, or more formal planning?

When staying self-employed usually makes more sense

Staying self-employed often makes sense when your business is still small, your profits are inconsistent, most profits need to be withdrawn for living costs, your legal risk is relatively low, and you want the simplest filing setup. It is usually the lower-cost option for startups, solo consultants, and service businesses that are still testing demand. CRA’s business setup guidance also notes that the structure you choose has a significant effect on how you report income.

Self-employment may be the better fit when:

- you are testing a new business idea

- your annual profit is still modest or unstable

- you expect to use most of the profit personally

- you want fewer filing obligations

- you are not ready for corporate bookkeeping, payroll, and year-end work

A sole proprietorship is straightforward. You track income and expenses, report net business income on your personal return, and pay tax personally. But “simpler” does not mean “no compliance.” You still need proper records, may need GST/HST registration, and may owe CPP on self-employment income. CRA says self-employed workers pay both the employer and employee portions of CPP when they file their T1 return.

That CPP point is one of the most overlooked differences. Employees usually split CPP with an employer. A self-employed owner generally pays the full contribution through the personal return. That does not automatically make self-employment worse, but it is a real cash-flow factor when comparing structures.

When incorporation usually makes more sense

Incorporation often becomes more attractive when you are earning more than you need personally, can leave some after-tax profit in the business, want a structure that separates the company from you personally, or expect the business to grow beyond a one-person operation. It also becomes more practical when contracts, lenders, or future partners prefer dealing with a corporation. CRA’s setup guidance identifies corporation as a distinct business structure, and Ontario’s online services confirm that incorporating and maintaining a corporation is handled through the Ontario Business Registry and related provincial filings.

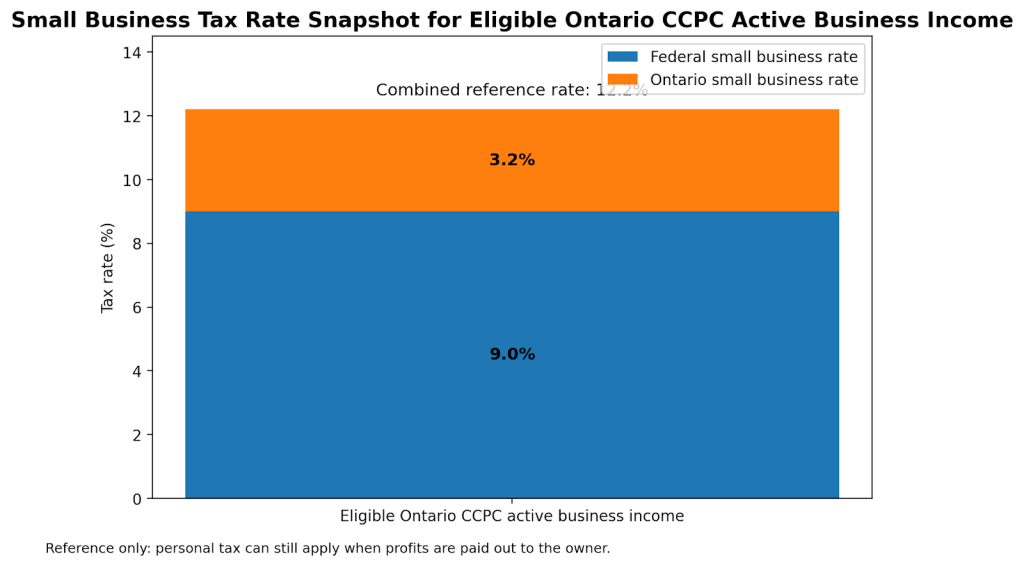

The tax argument for incorporation is real, but it needs to be framed correctly. Federally, the small business deduction reduces the net corporate tax rate on qualifying active business income to 9%. Ontario says its small business deduction reduces the Ontario corporate income tax rate on the first $500,000 of active business income of eligible CCPCs to 3.2%. Combined, that is about 12.2% on qualifying income allocated to Ontario before personal tax is considered when profits are later paid out.

That is why incorporation is often more useful as a tax deferral strategy than as a guaranteed tax savings strategy. If you can leave part of the earnings in the corporation for working capital, debt reduction, hiring, or expansion, the lower initial corporate rate may help. If you need to withdraw nearly all profits every year for personal living costs, the practical benefit may shrink once personal tax and extra admin costs are added.

Incorporation can also make more sense when:

- contracts require a corporation

- risk exposure is rising

- you want a clearer ownership structure

- you may add shareholders later

- you want the business to continue beyond the owner

Which is better for taxes in Canada?

For taxes, self-employed is usually simpler, but incorporation may create a deferral opportunity if profits can stay in the company. The better choice depends on how much profit you retain, how you plan to pay yourself, and how much complexity you are willing to carry.

Here is the plain-English version:

Self-employed: business profit is taxed directly on your personal return.

Corporation: the company pays tax first, and you pay personal tax later when money is withdrawn by salary, bonus, or dividend.

That does not mean corporations always produce less total tax. It means the timing can be better in the right circumstances. Owners get into trouble when they hear a headline like “incorporate and save tax” without checking whether they will actually leave money in the company.

If you withdraw everything every year, add corporate accounting fees, and create payroll or dividend-reporting obligations, the benefit may be much smaller than expected. A corporation can still be the right structure, but the reason may be risk management or long-term planning rather than pure tax savings.

What about liability and legal protection?

A corporation is a separate legal entity, which can provide a layer of separation between the business and the owner. A sole proprietorship does not have that separation, so the owner is generally exposed personally to business obligations.

That said, incorporation is not a complete shield. Personal guarantees, poor contracts, regulatory issues, and director responsibilities can still create personal exposure. So the smarter way to think about this is not “incorporation eliminates risk,” but “incorporation can improve legal separation when the business has grown beyond a low-risk solo operation.”

This matters most for businesses with:

- employees

- significant contracts

- leased premises

- borrowed money

- customer injury or property-damage risk

- higher professional or operational exposure

Many Ontario businesses incorporate because the risk profile changed, not because the tax profile changed first.

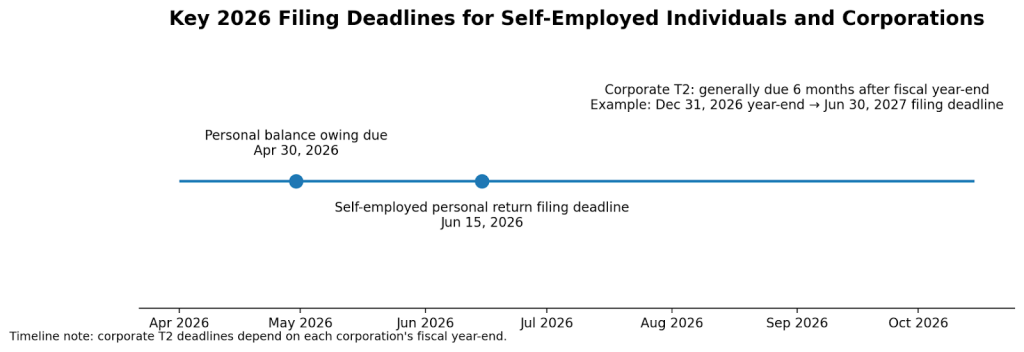

How do filing deadlines and compliance differ?

This is one of the biggest practical differences.

For self-employed owners, CRA says the filing due date for 2025 returns is generally June 15, 2026 if you or your spouse or common-law partner is self-employed. But if you have a balance owing, it is still generally due April 30, 2026. That mismatch causes confusion every year. Filing can wait until June, but paying usually cannot.

For corporations, CRA says the T2 must generally be filed within six months of the end of each tax year. CRA also states that resident corporations generally must file every tax year even if there is no tax payable, and for tax years starting after 2023, most corporations must file electronically or risk a $1,000 non-compliance penalty.

So the compliance picture looks like this:

| Topic | Self-Employed | Incorporated |

| Main tax return | T1 personal return | T2 corporate return |

| Filing deadline | Generally June 15 if self-employed | Generally 6 months after year-end |

| Payment deadline | Generally April 30 if balance owing | Depends on corporate rules and year-end |

| Recordkeeping burden | Lower | Higher |

| Separate legal entity | No | Yes |

| Annual compliance | Simpler | More involved |

The biggest mistake here is assuming incorporation is just “one extra form.” It is usually a full shift in how the business is tracked, reported, and maintained.

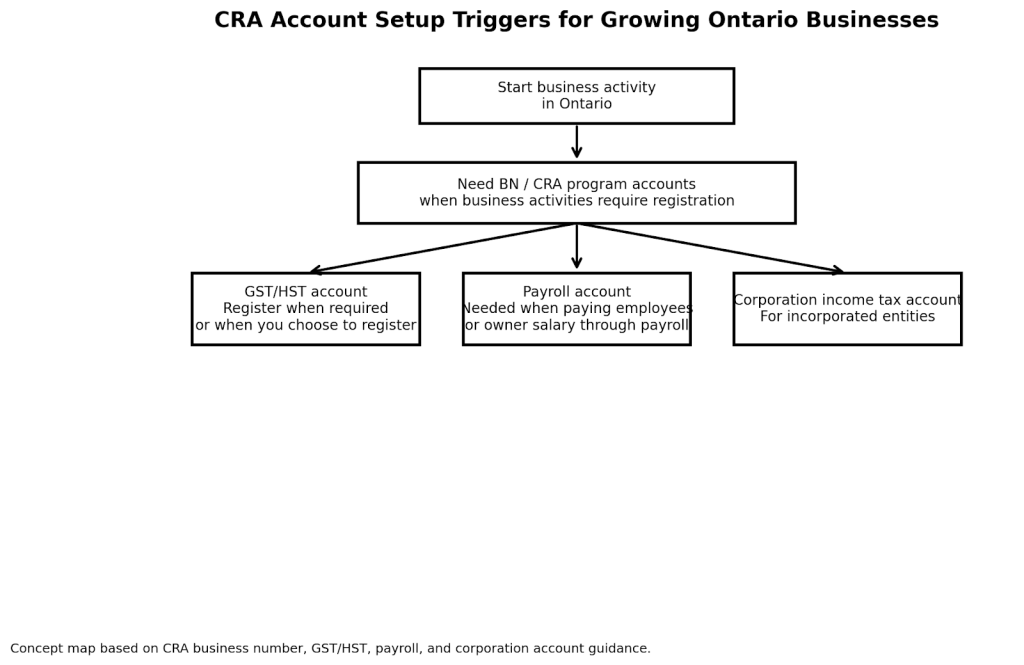

What happens with GST/HST, payroll, and CRA accounts?

Both sole proprietors and corporations may need a Business Number and CRA program accounts depending on what they do. CRA says businesses may need program accounts such as:

- RT for GST/HST

- RP for payroll

- RC for corporation income tax

If your business is unincorporated, you generally only need a BN when you register for program accounts. If you incorporate, CRA says you need a BN.

For GST/HST, the small-supplier rules are a major trigger. CRA says you must register if you are not a small supplier and you make taxable sales, leases, or other supplies in Canada. The small-supplier threshold is generally tied to $30,000.

For payroll, the difference becomes practical when a corporation starts paying the owner a salary or hires employees. CRA’s Payroll Deductions Online Calculator and payroll deduction guidance exist because once payroll applies, withholding and remittance become ongoing obligations, not optional year-end adjustments.

Sole proprietor vs corporation in Ontario

| Feature | Sole Proprietor | Corporation |

| Legal status | Not separate from owner | Separate legal entity |

| Tax filing | Personal T1 with business schedules | Separate T2 return |

| Startup cost | Usually lower | Usually higher |

| Admin burden | Lower | Higher |

| Liability separation | Limited | Better, but not absolute |

| Keeping profits in business | Limited planning flexibility | Often better for deferral and reinvestment |

| CRA account setup | May be simpler | Often more program accounts and filings |

| Best fit | Early-stage, simple operations | Growth, retained earnings, risk management |

Ontario’s current business services and registry guidance support the practical reality that incorporation usually brings more formal registration and maintenance obligations.

A simple roadmap for choosing the right structure

The best way to choose is to review profits, cash needs, risk, admin tolerance, and future plans together.

Start here:

- Estimate annual net profit.

- Decide how much you need to withdraw personally.

- Review your legal and operational risk exposure.

- Check whether you expect staff, partners, or investors.

- Compare the cost of bookkeeping, payroll, tax filings, and corporate maintenance.

- Confirm whether GST/HST or payroll registration is required.

- Revisit the structure as the business grows.

This decision should be reviewed, not romanticized. Many Ontario businesses sensibly start as self-employed operations and incorporate later when profits, risk, or staffing needs justify the change. Ontario’s own registration guidance makes clear that business owners can register and incorporate through the provincial system as the business evolves.

Common mistakes business owners make

Most structure mistakes happen because owners decide based on a single headline, usually “save tax,” without checking deadlines, CPP, payroll, legal risk, and cash-flow reality.

Common mistakes include:

- incorporating before profits support the extra admin

- staying self-employed after risk and contracts have grown

- missing the April 30 payment deadline while relying on the June 15 filing deadline

- forgetting that self-employed CPP works differently

- ignoring GST/HST registration triggers

- paying from a corporation without proper payroll or dividend reporting

- mixing personal and business records

These mistakes are expensive because they usually create both tax friction and bookkeeping cleanup later. CRA’s current rules on payment dates, GST/HST registration, CPP contributions, and corporate filing make those consequences very practical.

FAQ

Should I incorporate if I make more than $100,000?

Not automatically. Income level matters, but the bigger question is how much profit you can leave in the company after paying yourself. If most of the money is withdrawn personally, incorporation may offer less practical benefit than many online claims suggest.

Is self-employed the same as sole proprietor in Canada?

Often, yes in everyday use. A self-employed person commonly operates as a sole proprietor, though self-employment can also exist in a partnership. CRA’s self-employed guidance is aimed at sole proprietorships, partnerships, and similar business-income situations.

Do self-employed people pay more CPP?

Generally yes, in the sense that self-employed individuals pay both the employer and employee portions of CPP. CRA states this directly.

Do corporations have to file even if they made no money?

Usually yes. CRA says resident corporations generally must file a T2 every tax year, even if there is no tax payable.

When is the self-employed tax deadline in Canada for 2026?

For 2025 personal returns filed in 2026, CRA says self-employed individuals generally have until June 15, 2026 to file, but any balance owing is generally due April 30, 2026.

When is a corporate tax return due?

CRA says a corporation generally must file its T2 within six months of the end of its tax year.

Do I need to register for HST right away?

Not always. Registration depends on the small-supplier rules and the nature of your activities. But once you are no longer a small supplier and make taxable supplies, registration may become mandatory.

Can I switch from self-employed to incorporated later?

Yes. Many Ontario businesses start as sole proprietorships and incorporate later as profits, risk, or staffing needs grow. The transition should be planned carefully so registrations, banking, contracts, and CRA accounts are updated properly.

Final takeaway

For many Ontario business owners, self-employed is better when simplicity, lower cost, and direct access to profits matter most. Incorporated is often better when you are keeping profits in the business, managing more legal or contractual risk, or building something that needs a stronger long-term structure.

The key compliance reminder is simple: do not choose based on tax headlines alone. Check filing deadlines, CPP, GST/HST, payroll, legal risk, and the cost of ongoing accounting work before you decide. Rules vary by facts, industry, and how money moves through the business.

If you want, I can now turn this into a clean 2,200-word publication draft with internal link placeholders and chart callouts preserved exactly for your site CMS.

Sources and References

- Canada Revenue Agency – Small businesses and self-employed income

https://www.canada.ca/en/revenue-agency/services/tax/businesses/small-businesses-self-employed-income.html - Canada Revenue Agency – Sole proprietorships and partnerships

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/sole-proprietorships-partnerships.html - Canada Revenue Agency – Sole proprietorship

https://www.canada.ca/en/revenue-agency/services/tax/businesses/small-businesses-self-employed-income/setting-your-business/sole-proprietorship.html - Canada Revenue Agency – Corporation

https://www.canada.ca/en/revenue-agency/services/tax/businesses/small-businesses-self-employed-income/setting-your-business/corporation.html - Canada Revenue Agency – Business income tax reporting

https://www.canada.ca/en/revenue-agency/services/tax/businesses/small-businesses-self-employed-income/business-income-tax-reporting.html - Canada Revenue Agency – Due dates and payment dates for individuals

https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/important-dates-individuals.html - Canada Revenue Agency – Corporation income tax return

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/corporations/corporation-income-tax-return.html - Canada Revenue Agency – When to file your corporation income tax return

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/corporations/corporation-income-tax-return/when-file-your-corporation-income-tax-return.html - Canada Revenue Agency – Corporation tax rates

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/corporations/corporation-tax-rates.html - Canada Revenue Agency – Contributions to the Canada Pension Plan

https://www.canada.ca/en/services/benefits/publicpensions/cpp/contributions.html - Canada Revenue Agency – CPP contribution rates, maximums and exemptions

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/payroll/payroll-deductions-contributions/canada-pension-plan-cpp/cpp-contribution-rates-maximums-exemptions.html - Canada Revenue Agency – Responsibilities, benefits and entitlements for employees and self-employed workers

https://www.canada.ca/en/revenue-agency/services/tax/canada-pension-plan-cpp-employment-insurance-ei-rulings/cpp-ei-explained/employees-self-employed-workers-responsibilities-benefits-entitlements.html - Canada Revenue Agency – Register for a GST/HST account

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/gst-hst-businesses/gst-hst-account/register-account.html - Canada Revenue Agency – General Information for GST/HST Registrants

https://www.canada.ca/en/revenue-agency/services/forms-publications/publications/rc4022/general-information-gst-hst-registrants.html - Canada Revenue Agency – Small suppliers

https://www.canada.ca/en/revenue-agency/services/forms-publications/publications/2-2/small-suppliers.html - Canada Revenue Agency – Business number and CRA program accounts

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/business-registration/business-number-program-account.html - Canada Revenue Agency – Register as a resident with a Canadian business

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/business-registration/business-number-program-account/how-register/resident.html - Canada Revenue Agency – Payroll

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/payroll.html - Canada Revenue Agency – Payroll Deductions Online Calculator

https://www.canada.ca/en/revenue-agency/services/e-services/digital-services-businesses/payroll-deductions-online-calculator.html - Ontario – Corporate Income Tax

https://www.ontario.ca/document/corporations-tax/corporate-income-tax - Ontario – Register your business online

https://www.ontario.ca/page/business/start/register-your-business-online - Ontario – Incorporate an Ontario Business Corporation

https://www.ontario.ca/business/permits-licences/incorporate-an-ontario-business-corporation/ - Ontario – Ontario Business Registry

https://www.ontario.ca/page/ontario-business-registry