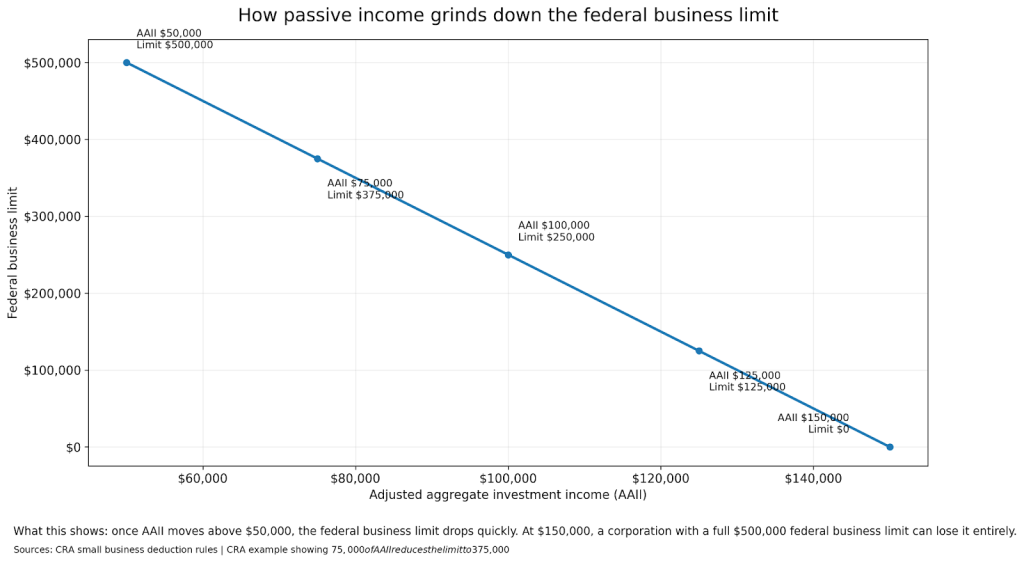

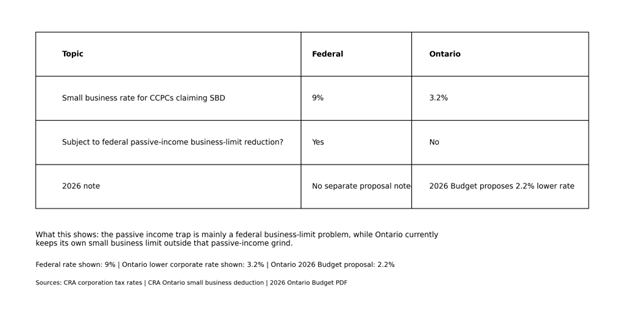

For many Ontario corporations, Passive Income is not just a side tax issue. It can reduce access to the lower federal small business rate on active business income. Under CRA’s small business deduction rules, the federal business limit starts grinding down when adjusted aggregate investment income, or AAII, goes above $50,000 in the prior calendar year. If AAII reaches $150,000 and the corporation otherwise has the full $500,000 business limit, the federal limit can be reduced to nil. Ontario adds an important twist: CRA says the Ontario small business deduction is not subject to the federal passive-income business-limit reduction.

Quick Answer

If your corporation earns enough passive investment income, it can lose part or all of its federal small business deduction in the following year. The federal business limit is reduced by $5 for every $1 of AAII above $50,000, based on the formula CRA gives in its passive investment income and SBD guidance. For a corporation that otherwise has the full $500,000 business limit, that means the grind is complete at $150,000 of AAII. The trap is easy to miss because the tax cost is indirect: the passive income itself is one issue, but the larger hit often shows up later when more of your active business income is taxed at the higher general federal corporate rate instead of the lower small business rate.

Why this catches Ontario SMEs off guard

Many owner-managers do the sensible thing: they leave extra cash inside the corporation. That money may be held for tax instalments, expansion, debt repayment, a downturn reserve, or long-term investing. The problem is that ordinary investment income inside a corporation can quietly build into a federal tax problem even when the business itself is not doing anything aggressive.

This catches Ontario businesses off guard for two reasons. First, passive income often comes from ordinary things like interest, GICs, marketable securities, rental income, or taxable capital gains. Second, the result is split between federal and Ontario tax treatment. CRA says the federal small business deduction can grind down, but the Ontario small business limit is not reduced by the federal passive-income rule. That means an Ontario corporation can lose some or all of the federal benefit while still keeping the Ontario one, which makes the tax result more confusing than many owners expect.

What is the passive income trap?

The passive income trap is the rule that cuts a CCPC’s federal business limit when adjusted aggregate investment income becomes too high. CRA’s small business deduction rules page explains that a CCPC’s business limit is generally $500,000, subject to the normal associated-corporation and taxable-capital rules, and that it is further reduced on a straight-line basis if the total AAII of the corporation and associated corporations is between $50,000 and $150,000. CRA gives the formula as BL / $500,000 × 5 × (AAII − $50,000).

For a company that otherwise has the full $500,000 business limit, the math is straightforward:

- $50,000 or less of AAII: no passive-income grind

- $75,000 of AAII: federal business limit reduced to $375,000

- $100,000 of AAII: federal business limit reduced to $250,000

- $150,000 or more of AAII: federal business limit reduced to $0

CRA’s own example shows that $75,000 of AAII reduces a $500,000 business limit by $125,000. That example is useful because it shows how quickly the grind starts to matter even before passive income becomes very large.

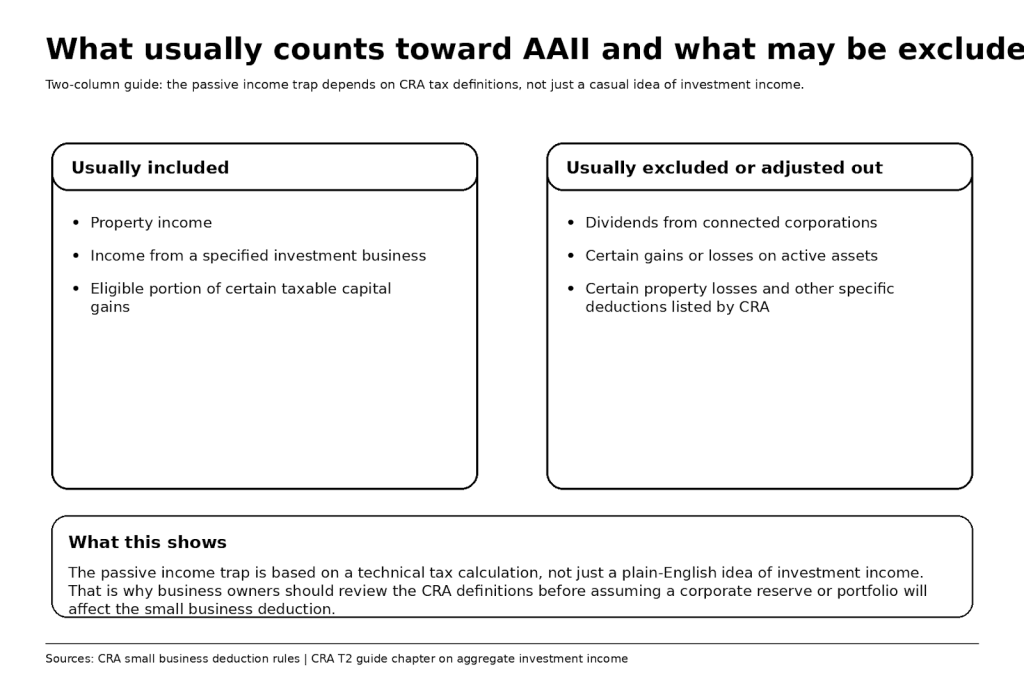

What counts as passive income for this rule?

The answer is broader than “just interest.”

CRA’s T2 Schedule 7 and the related T2 guide discussion of aggregate investment income show that the starting point is aggregate investment income, which generally includes total income from property, income from a specified investment business, and the eligible portion of certain taxable capital gains, reduced by certain property losses. CRA’s passive-income rules then define AAII by adding items such as property income and certain taxable capital gains, while excluding some items such as dividends from connected corporations and gains or losses from the disposition of property that is an active asset of the corporation at the time of disposition.

In plain English, the main trouble spots are usually:

- interest income

- portfolio dividends that do not fall within an exclusion

- many forms of rental or royalty income

- taxable capital gains that are not carved out as gains on active business assets

That is why the passive income trap can affect ordinary corporations with normal reserve accounts or investment portfolios. A GIC ladder, a brokerage account, a growing pool of retained earnings invested in securities, or appreciated non-active assets can all push AAII higher. The key point is that AAII is a tax calculation, not a bookkeeping label. If you want the real answer, it has to come from tax workpapers and Schedule 7, not a rough estimate from the general ledger.

Why associated corporations can make the problem worse

This is where many SMEs get surprised.

CRA’s small business deduction rules say the business limit must be allocated among corporations that are associated, and the passive-income reduction uses the total AAII of the corporation and any corporations with which it is associated for the relevant prior period. In other words, you do not always get to look at one company in isolation.

That matters most when an owner has an operating company plus a holding company, or multiple associated corporations in the same group. CRA’s second example shows this clearly: one corporation had $75,000 of AAII and an associated corporation had $55,000. Together, the combined AAII of $130,000 reduced the available business limit to only $100,000 when the full business limit had been allocated to one corporation. That is a dramatic result, and it explains why a holdco can materially worsen the tax picture even if the operating company itself is not earning large investment income directly.

CRA also describes an anti-avoidance rule on that same page for cases where a corporation lends or transfers property to a related corporation and one reason for doing so is to reduce AAII and the future passive-income business-limit reduction. So moving assets around a corporate group is not a clean shortcut by itself.

How Ontario changes the analysis

Ontario businesses need to split the federal and provincial stories.

CRA’s Ontario small business deduction page says the deduction reduces Ontario basic income tax and results in a lower Ontario rate of 3.2%. Most importantly for this topic, CRA explicitly says the Ontario small business limit is not subject to the federal passive income business limit reduction. That means eligible Ontario corporations can still receive the Ontario small business deduction regardless of the amount of passive income they earned, subject to Ontario’s own taxable-capital rules.

So the passive income trap is real, but it does not hit both layers of tax in the same way. A corporation can lose some or all of the federal small business deduction while still keeping the Ontario one. That softens the blow, but it does not eliminate it. You still need to know what the federal grind is doing to your active business income.

There is also a current Ontario planning wrinkle. The 2026 Ontario Budget says the government is proposing to cut the small business corporate income tax rate from 3.2% to 2.2% effective July 1, 2026. As of the current CRA Ontario page, the enacted lower Ontario rate remains 3.2%, so owners should treat the 2.2% rate as a proposal until it is actually enacted.

Federal versus Ontario treatment for Ontario CCPCs

What an SME should do before passive income becomes expensive

The best response is not panic. It is measurement.

Start by confirming that the rule applies to you. This issue mainly affects corporations that are CCPCs. A sole proprietor does not use the corporate small business deduction in the same way.

Then review the prior-year corporate return, especially Schedule 7. CRA uses Part 2 of Schedule 7 to calculate adjusted aggregate investment income and Part 1 to calculate aggregate investment income. If you are trying to understand whether the trap is approaching, Schedule 7 is where the real answer starts.

Next, identify the actual drivers of AAII. Separate interest, rent, royalties, portfolio income, and taxable capital gains from excluded items such as dividends from connected corporations and gains on active assets. Then check the entire group, not just one corporation. If there is a holdco or other associated company, the federal business limit analysis is rarely complete until the associated-company picture is included.

Finally, model the next-year federal business limit before making year-end decisions. Sometimes the answer is that paying the extra tax is acceptable because the corporation genuinely needs liquidity or long-term reserves. Sometimes the answer is that compensation, dividend, or investment structure should be revisited. But that decision should be based on numbers, not rules of thumb.

Common mistakes business owners make

The first mistake is assuming passive income means only interest. CRA’s rules are broader than that.

The second is ignoring associated corporations. The federal business-limit reduction looks at group AAII, not just one legal entity.

The third is focusing only on the tax paid on the investment income itself. CRA’s rules make clear that the bigger issue is often the next-year loss of access to the lower federal small business rate on active business income.

The fourth mistake is assuming Ontario follows the federal grind exactly. CRA says it does not. The Ontario small business limit is not subject to the federal passive-income business-limit reduction.

The fifth is thinking that a transfer to a related corporation automatically fixes the issue. CRA explicitly describes an anti-avoidance rule aimed at that kind of planning.

A sixth mistake is ignoring the refund mechanics on investment income. CRA’s T2 guide explains that CCPCs generate NERDTOH on the refundable portion of Part I tax they pay on investment income, and that all or part of ERDTOH and NERDTOH may later be refunded when the corporation pays taxable dividends. That can help with integration, but it does not restore the lost federal business limit.

FAQ

What counts as passive income in a corporation in Canada?

Generally, property income and certain taxable capital gains are the main components, with some exclusions such as dividends from connected corporations and gains on active business assets. The technical calculation flows through Schedule 7 and CRA’s related guidance.

How does passive income affect the small business deduction?

Once AAII exceeds $50,000, the federal business limit starts shrinking. If AAII reaches $150,000 and the corporation otherwise has the full $500,000 business limit, the federal limit can be fully eliminated.

Does rental income count toward the passive income grind?

Often yes, because CRA’s aggregate investment income rules include income from property and income from a specified investment business, though the exact treatment still depends on the facts.

Does Ontario follow the same passive income grind as the federal government?

No. CRA says the Ontario small business limit is not subject to the federal passive-income business-limit reduction.

Can a holding company make the problem worse?

Yes. If the corporations are associated, their AAII is combined for the passive-income business-limit reduction.

Final Takeaway

The Passive Income trap is easy to underestimate because the damage often shows up one year later, when the federal small business deduction has already started to shrink. For Ontario SMEs, the issue is even easier to misread because the federal deduction may grind down while the Ontario small business deduction still survives. The right response is not guesswork. It is a proper review of Schedule 7, the prior-year AAII calculation, and the associated-corporation picture before making compensation, dividend, or investment decisions.

If you want clarity on whether your corporation is drifting into the passive income trap, speak with a Clearwealth accounting professional. A short review can usually show whether the issue is small, growing, or already affecting your federal small business deduction.

Sources and References

- CRA small business deduction rules

https://www.canada.ca/en/revenue-agency/programs/about-canada-revenue-agency-cra/federal-government-budgets/budget-2018-equality-growth-strong-middle-class/passive-investment-income/small-business-deduction-rules.html - CRA Schedule 7

https://www.canada.ca/en/revenue-agency/services/forms-publications/forms/t2sch7.html - CRA T2 Corporation Income Tax Guide – Chapter 6

https://www.canada.ca/en/revenue-agency/services/forms-publications/publications/t4012/t2-corporation-income-tax-guide-chapter-6-pages-6-7-t2-return.html - CRA Ontario small business deduction

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/corporations/provincial-territorial-corporation-tax/ontario-provincial-corporation-tax/ontario-small-business-deduction.html - CRA corporation tax rates

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/corporations/corporation-tax-rates.html - 2026 Ontario Budget PDF https://budget.ontario.ca/2026/pdf/2026-ontario-budget-en.pdf