Budget changes do not always look like tax hikes. Sometimes they show up as higher occupancy costs, new point of sale charges, or new compliance steps that get missed until an audit, a vendor dispute, or an unhappy customer. Alberta Budget 2026 is a good example. Alberta largely holds the line on income tax rates, but adds targeted levies and increases certain property tax rates.

For small and mid sized businesses, that usually creates three practical questions.

- Will our costs rise?

- Do we need to change pricing or invoices?

- What do we need to document so we are compliant if CRA or Alberta asks?

Alberta Budget 2026 keeps personal and corporate income tax rates unchanged, including the small business rate, but introduces targeted measures that can raise operating costs for some SMEs. Key changes include a tourism levy increase to 6% on short term accommodation starting April 1, 2026, and a new 6% passenger vehicle rental tax expected to start January 1, 2027. Education property tax rates also rise for 2026 to 2027, which may flow through to commercial rents and occupancy costs. For Ontario based businesses with Alberta operations, the biggest action items are confirming where you have a permanent establishment, aligning payroll province of employment, and updating invoicing and contracts for new indirect taxes.

If you operate in multiple provinces, especially if you are an Ontario business selling in or expanding into Alberta, there is also a quiet risk. Allocating income correctly between provinces, setting payroll up properly, and charging the right GST or HST based on place of supply rules.

Quick Start: Pick Your Path

Use this checklist to jump to what applies to you.

- I own or lease business space in Alberta

Go to: How education property tax changes can raise occupancy costs - I run a hotel or short term accommodation business

Go to: How the tourism levy increase affects pricing and remittances - I rent passenger vehicles (fleet, car rental, replacements, customer rentals)

Go to: What the new vehicle rental tax means for SMEs - I am an Ontario business selling or hiring in Alberta

Go to: Operating in Alberta from Ontario: filings, payroll, and GST or HST - I want a simple action plan

Go to: Step by step roadmap for SMEs

Alberta Budget 2026 highlights SMEs should care about

Alberta Budget 2026 keeps corporate and personal income tax rates steady, but introduces targeted measures that can affect SME costs. The most practical changes for many businesses are the higher tourism levy, a new vehicle rental tax (expected 2027), and higher education property tax rates that can raise occupancy costs.

Key SME relevant items include:

- No change to Alberta corporate income tax rates, including the small business rate.

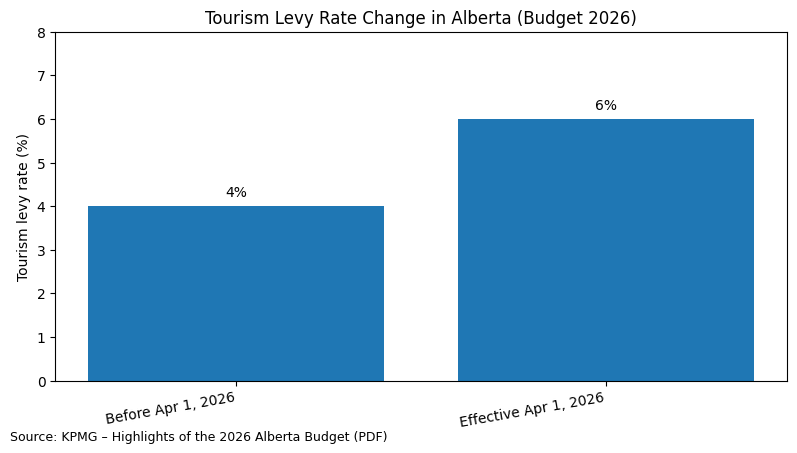

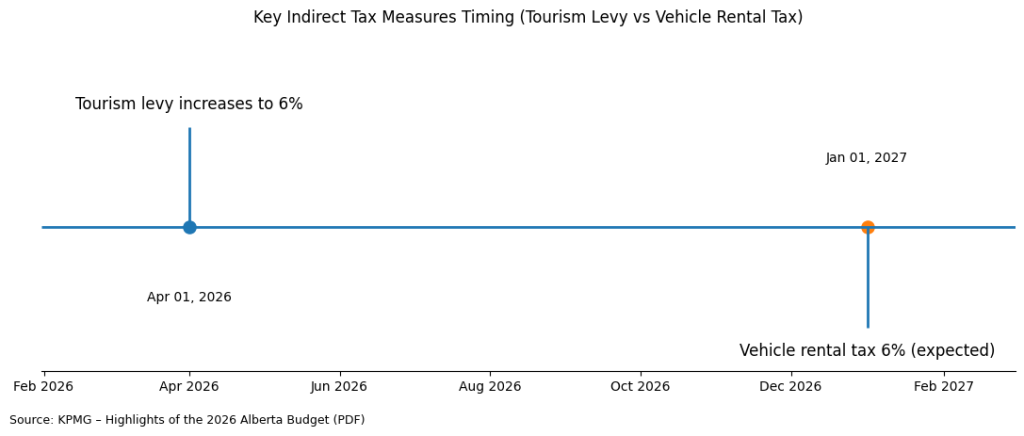

- Tourism levy increases to 6% from 4% effective April 1, 2026 (short term accommodation).

- Vehicle rental tax: a new 6% tax on passenger vehicle rentals, expected January 1, 2027 (details expected with legislation later in 2026).

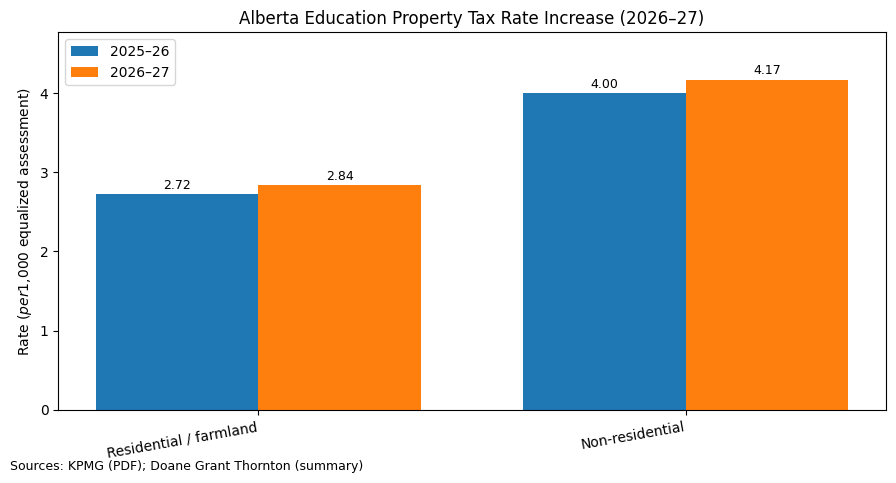

- Education property tax rates increase for 2026 to 2027 (residential and farmland, and non residential).

Are there Alberta small business tax changes in 2026

Budget 2026 does not announce increases to Alberta corporate income tax rates, including the small business rate. The meaningful cost changes for many SMEs are indirect: a higher tourism levy on accommodation, a new vehicle rental tax (expected 2027), and higher education property tax rates that can raise occupancy costs.

What to do with this as an SME

- If you are a CCPC, confirm you are properly tracking the small business limit and eligibility, especially if you have associated corporations.

- If you are a sole proprietor, corporate rate stability may not be relevant, but indirect taxes and occupancy costs can still hit margins.

How the tourism levy increase affects pricing and remittances

Effective April 1, 2026, Alberta’s tourism levy on short term accommodation increases from 4% to 6%. If you sell accommodation, you will likely need to update booking systems, invoices, and tax disclosure. If you buy accommodation for business travel, expect higher travel costs and ensure receipts separate GST and the levy.

Practical SME implications

Accommodation providers

- Update POS and booking software.

- Update invoice templates and customer facing disclosures.

- Train staff on what the levy applies to.

Businesses that travel

- Update travel budgets and expense policies.

- Confirm expense coding so the levy is booked consistently.

What the new vehicle rental tax means for SMEs

Alberta Budget 2026 introduces a proposed 6% tax on passenger vehicle rentals in Alberta, expected to take effect January 1, 2027. It is described as applying to the rental price excluding GST and excluding itemized charges like insurance and fuel. If you rent vehicles for operations or customers, plan for pricing and contract updates.

How this shows up in real life

Car rental businesses

- System changes may be needed (tax engine, invoice lines, remittance workflow).

- Update customer terms and disclosures.

SMEs renting vehicles for crews or sales

- This becomes a predictable line item cost.

- It may affect job costing if you pass travel costs to customers.

How education property tax changes can raise occupancy costs

Budget 2026 increases Alberta education property tax rates for 2026 to 2027 to $2.84 per $1,000 of equalized assessment for residential and farmland properties and $4.17 per $1,000 for non residential properties. Even if you do not own property, leases often pass property tax through to tenants, so your rent or CAM charges may rise.

What to check in your lease (owners and tenants)

- Does your lease treat education property tax as a recoverable operating cost?

- Are you billed via additional rent or CAM?

- Are there caps, exclusions, or reconciliation requirements?

If you own commercial property used by your business, separate your bookkeeping so you can see what changed.

- municipal property tax

- education property tax component

- special levies or adjustments

Operating in Alberta from Ontario: filings, payroll, and GST or HST

If your Ontario business has a permanent establishment in Alberta, you generally must allocate taxable income across provinces and may have Alberta specific corporate tax administration. Employers also need correct province of employment setup for payroll reporting, and invoices must follow GST or HST place of supply rules.

Permanent establishment and allocating income between provinces

If you have permanent establishments in more than one province, CRA requires allocating taxable income using Schedule 5. This applies to corporations with permanent establishments in Alberta.

SME takeaway: If you opened an Alberta office, hired Alberta staff, or regularly perform contracts there, do not guess. Document your facts and get your allocation approach correct early.

Payroll: province of employment

Employers must report the employee’s province of employment on the T4 slip. If you have employees working remotely or across provinces, payroll setup needs extra care so source deductions and reporting align with CRA’s administrative approach and your actual work arrangements.

GST or HST place of supply and invoicing

Alberta is not an HST province, but the rate you charge depends on place of supply rules for what you sell (goods, services, leases), not where you are incorporated. Review your invoicing logic if you sell into both Alberta and Ontario.

SME economic outlook and budgeting implications

Alberta’s fiscal plan includes continued deficits alongside capital spending. For SMEs, this can mean mixed signals: potential demand from public sector and infrastructure activity, but cost pressure from labour constraints and targeted levies. Build budgets with scenario ranges, not one forecast.

How to use this in planning:

- If you sell into construction or infrastructure supply chains, refresh your pipeline and bid calendar.

- If you are cost sensitive (retail, hospitality, services), stress test cash flow for higher occupancy and travel related costs.

Step by step roadmap for SMEs

Start by identifying which measures touch your business (accommodation, vehicle rentals, property occupancy, multi province operations). Then update pricing, invoicing, payroll, and contracts. Finally, document decisions and keep evidence so you are ready for questions from customers, lenders, CRA, or Alberta administrators.

A practical checklist

- Map where you operate and where you have people, offices, and contracts (permanent establishment risk).

- Update systems:

- booking and POS for tourism levy

- rental invoicing and contracts for vehicle rental tax (when effective)

- lease cost tracking for education property tax pass through

- Review contracts for tax change clauses (who bears new levies and when you can re-price).

- Confirm payroll province of employment setup and T4 reporting.

- Validate GST or HST charging using place of supply rules for your specific supplies.

- Document decisions in a simple Budget 2026 impacts memo for your files.

Common mistakes to avoid

The biggest errors are operational: charging the wrong tax, failing to update invoices, assuming your lease will not pass through property tax increases, and ignoring multi province allocation and payroll rules. These mistakes can trigger reassessments, customer disputes, and messy year end cleanup.

Watch for these:

- Forgetting to update accommodation systems for the 6% tourism levy effective April 1, 2026.

- Treating the vehicle rental tax as GST included when it is described as calculated on rental price excluding GST.

- Not reading lease clauses, then getting surprised by higher additional rent or CAM from education property tax changes.

- Assuming Ontario incorporation means Ontario tax only (ignoring permanent establishment and allocation).

- Payroll set up with the wrong province of employment (T4 mismatches).

- Charging HST on Alberta supplies or GST where HST applies without checking place of supply rules.

- Weak documentation for allocations, tax calculations, or pass through amounts.

Comparison table: Which Budget 2026 measures hit which SMEs

| Measure | Who is most affected | What changes | When it starts | So what for SMEs |

| Tourism levy | Hotels, short term accommodation, business travel users | Levy rate rises 4% to 6% | April 1, 2026 | Update pricing and invoices, higher travel costs, clean receipt support |

| Vehicle rental tax | Car rental companies, SMEs renting passenger vehicles | New 6% tax on passenger vehicle rentals (excluding GST) | Expected Jan 1, 2027 | Update contracts and invoicing, adjust budgets and job costing |

| Education property tax | Commercial property owners and many tenants | Rates rise (non residential to $4.17 per $1,000) | 2026 to 2027 | Lease pass through risk, higher occupancy costs |

FAQs

What are the Alberta Budget 2026 highlights for small business owners

The core SME highlights are no change on income tax rates, plus targeted cost drivers: tourism levy increases to 6% on short term accommodation (April 1, 2026), a 6% passenger vehicle rental tax expected in 2027, and higher education property tax rates for 2026 to 2027.

Are Alberta corporate tax rates changing in 2026

Budget 2026 does not announce changes to Alberta corporate income tax rates, including the small business rate.

When does the tourism levy increase take effect, and what does it apply to

The tourism levy rate increases from 4% to 6% effective April 1, 2026. The levy applies to the price of short term accommodation in Alberta.

What is the vehicle rental tax and when does it start

Budget 2026 introduces a 6% tax on passenger vehicle rentals in Alberta, expected to come into effect January 1, 2027, with details expected when legislation is introduced later in 2026.

How can education property tax increases affect my business if I do not own property

Many commercial leases pass property taxes to tenants through additional rent or operating cost recoveries. With education property tax rates rising for 2026 to 2027, tenants may see higher occupancy costs at reconciliation time. Review your lease clauses and request clear breakdowns in landlord statements.

I am an Ontario corporation with Alberta contracts. Do I need to allocate income between provinces

If you have a permanent establishment in more than one province, CRA requires allocating taxable income using Schedule 5. Document your facts and keep support for your allocation method.

How do I determine the province of employment for payroll reporting

Employers must report the employee’s province of employment on the T4 slip. If employees work in more than one province or territory, document the arrangement and ensure payroll setup and reporting align with CRA guidance.

Will Alberta Budget 2026 change my GST or HST rate on invoices

The budget items discussed are provincial measures, not GST or HST changes. But if you sell across provinces, you must charge GST or HST based on place of supply rules for your specific supplies.

Closing: The main compliance takeaway

Alberta Budget 2026 is less about headline income tax rate changes and more about targeted levies and pass through costs that can quietly erode margins and create compliance risk if systems are not updated.

Before year end, make sure you can answer: which measures affect us, what changed in our invoices and contracts, and what evidence would we show if questioned. Keep documentation, avoid assumptions, and update bookkeeping categories so the impact is visible in reporting.

If you want help mapping the impact on your specific situation, especially if you are an Ontario business operating in Alberta, speak with a qualified accounting professional.

Sources and references (for publication)

Government of Alberta — Budget 2026 portal and Fiscal Plan documents (Open Alberta)

Alberta Budget 2026 taxpayers summary page (albertabudget.ca)

CRA — Permanent establishment guidance and Schedule 5 allocation instructions

- Permanent establishment (CRA): https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/corporations/provincial-territorial-corporation-tax/permanent-establishment.html

- Schedule 5 allocation instructions (CRA): https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/corporations/provincial-territorial-corporation-tax/you-have-complete-schedule-5.html

- Optional deeper technical reference (CRA folio): https://www.canada.ca/en/revenue-agency/services/tax/technical-information/income-tax/income-tax-folios-index/series-4-businesses/folio-3-general-principles-business-income-calculation/income-tax-folio-s4-f3-c2-provincial-income-allocation.html