Running a business as a sole proprietor in Ontario means you’re responsible for everything from invoicing and bookkeeping to taxes. Every dollar you spend to operate your business could reduce your tax bill, but only if you know which expenses are legitimate deductions and how to report them correctly to the Canada Revenue Agency (CRA). Additionally, unlike employees, you’re responsible for the full Canada Pension Plan (CPP) contribution — both the employee and employer portions — which can significantly impact your yearly tax bill. Missed deductions can cost you money, and errors can trigger CRA review or interest charges. This guide walks you through the most important deductions, how to calculate them, how CPP works for sole proprietors, and how to stay compliant throughout the tax year.

As a sole proprietor in Canada, you figure out tax deductions by tracking business-related expenses and reporting them on Form T2125 attached to your T1 income tax return. Eligible deductions include operating costs, home office expenses, vehicle costs, and more. The Canada Pension Plan (CPP) must be calculated on net business income, with you paying both the employee and employer portions. Staying organized and keeping receipts is key to CRA compliance.

Disclaimer: This article is for educational purposes only. Consult your accountant for personalized tax planning.

Quick Start: Pick Your Path

- New sole proprietor: Just started and need to learn what you can deduct.

- Growing business: Looking to maximize deductions and plan CPP payments.

- Side business founder: Combining employment income with sole proprietorship.

- Hybrid income earner: Juggling multiple income streams and CPP questions.

Each path has different reporting requirements and may affect when you pay taxes or how much CPP you owe.

What Is a Tax Deduction for Sole Proprietors?

Direct Answer: A tax deduction for a sole proprietor is any business expense that the CRA recognizes as necessary to earn income. These expenses are subtracted from your gross business revenue to determine your net income, reducing the amount you pay tax on.

Sole proprietors report business income as part of their personal tax return (T1 General) using Form T2125 (Statement of Business or Professional Activities). The CRA allows you to claim legitimate business expenses that are incurred to earn income. These expenses reduce your taxable income and, in turn, your federal and provincial tax liabilities.

If you earn $80,000 from freelancing and have $20,000 in deductible business expenses, your net income for tax purposes becomes $60,000. Your income tax will be calculated on $60,000, not $80,000.

What Business Expenses Are Deductible?

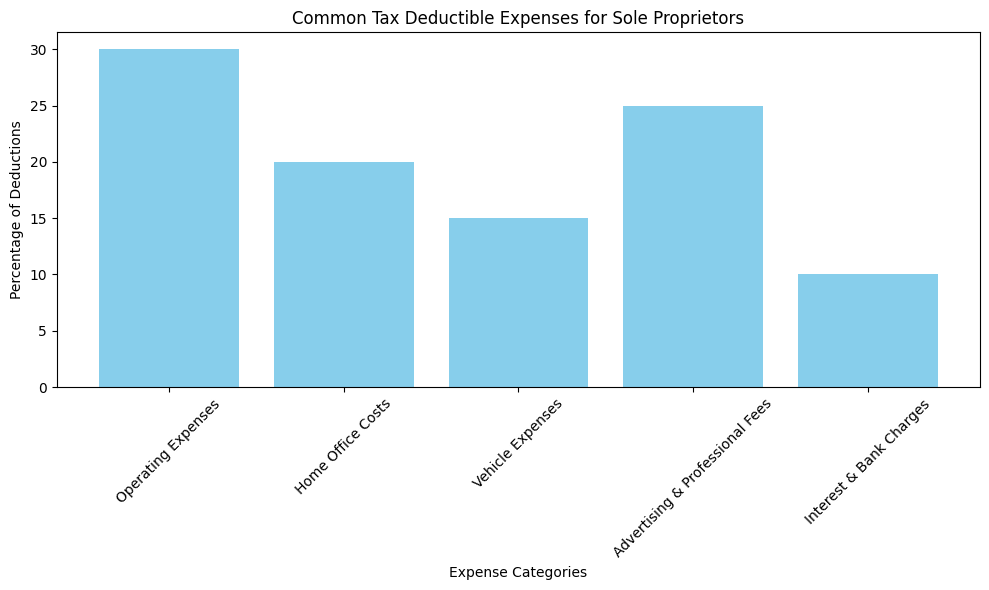

Sole proprietors can deduct a wide range of business expenses including operating costs, home office costs, vehicle expenses, advertising, professional fees, and certain interest charges as long as they are reasonable and directly related to earning business income.

Common deductible categories include:

- Operating and office expenses: Office supplies, software subscriptions, utilities.

- Home office expenses: A proportion of utilities, rent/mortgage interest, property taxes, and insurance if you work from home.

- Vehicle expenses: Fuel, maintenance, and insurance proportionate to business use.

- Advertising and marketing: Business promotions, website costs.

- Meals and entertainment: 50% deductible when directly related to business.

- Interest and bank charges: On business loans or accounts.

- Professional fees: Accountant, legal fees directly tied to the business.

Each expense must be reasonable and supported by documentation. Capital assets (like equipment) are typically deducted over time using Capital Cost Allowance (CCA).

How to Complete Form T2125

Form T2125 is the CRA form used by sole proprietors to report business income and expenses. You list your gross revenues, eligible expenses, and calculate your net business income to include in your T1 tax return.

Form T2125 summarizes your business’s financials:

- Business identification: Name, industry code.

- Income: Total revenue earned from clients.

- Expenses: Categories for deductible costs (see above).

- Net income/loss calculation: Subtract expenses from income.

This net amount transfers to your T1 General (Line 13500).

Tip: Use bookkeeping software or a simple spreadsheet to capture receipts and totals year-round. This will make filing your T2125 much easier.

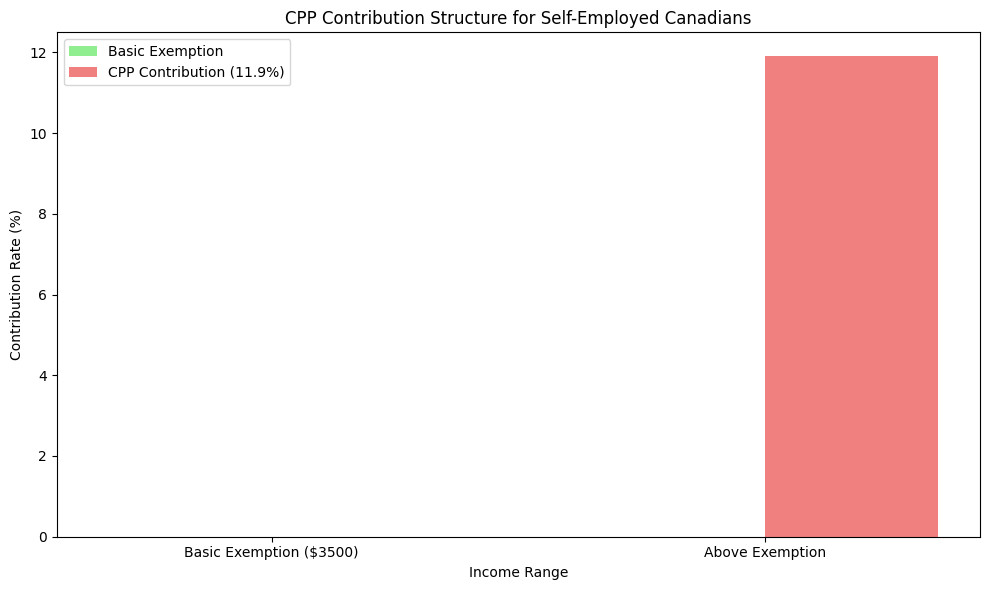

How CPP Works for Self‑Employed Sole Proprietors

Sole proprietors must pay into the Canada Pension Plan (CPP) on net business income above the basic exemption amount ($3,500). You’re responsible for paying both the employee and employer portions of CPP, which effectively doubles the rate compared to employees.

Regular employees only pay half of the CPP contribution, with the employer covering the other half. As a self-employed sole proprietor, you pay both portions. The rate and thresholds are defined annually by the CRA and reported on Schedule 8 of your T1 return.

- You pay CPP contributions only on net business income (after deductions).

- The first $3,500 of net income is exempt each year.

- Above the exemption, you pay a combined rate (e.g., ~11.9% base rate for 2025).

- There’s a second tier (CPP2) for higher income ranges.

Tax Impact:

- Half of your CPP contribution is deductible as a business expense, reducing taxable income.

- The other half generates a non-refundable tax credit.

Filing Deadlines and Payments

Sole proprietors must file their T1 return by June 15 of the following year, but any taxes owed must be paid by April 30 to avoid interest charges. If you owe more than a certain threshold, quarterly instalments may be required.

- Tax filing deadline: June 15 (with a spouse, if applicable).

- Tax payment deadline: April 30 (for any balance owing).

- Installments: If taxes owing consistently exceed CRA’s threshold, CRA may request quarterly payments.

Missing deadlines can result in interest and penalties, so it’s important to calculate provisional taxes throughout the year.

Common Mistakes Sole Proprietors Make

Mistakes include failing to track receipts, misclassifying personal expenses as business deductions, underreporting income, and not accounting for CPP correctly.

- Poor documentation: No receipts or organized records.

- Blending personal and business costs: Claiming personal expenses as business-related.

- Failing to claim eligible deductions: Not claiming every deduction you’re entitled to.

- Incorrect CPP reporting: Misunderstanding the dual-share requirement.

- Missing deadlines: Leading to penalties or interest.

Good bookkeeping and early preparation help avoid these issues.

FAQ

What counts as self‑employment income?

Gross income from your business before expenses — all revenue earned in the tax year must be reported.

Can I claim home office expenses?

Yes, if part of your home is used regularly and exclusively for business, you can claim a proportion of eligible household costs.

Do I have to register for GST/HST?

If your revenue exceeds the small supplier threshold (~$30,000), you generally must register and remit GST/HST.

How long should I keep receipts?

CRA recommends keeping records for six years in case of review.

Can I deduct vehicle costs?

Yes — only the business-use portion of fuel, insurance, and maintenance, supported by a mileage log.

Is help from an accountant worth it?

Yes — complex deductions and CPP calculations often benefit from a professional review to minimize errors.

Closing

Understanding tax deductions and CPP obligations as a sole proprietor requires careful tracking, documentation, and filing. If done correctly, you can maximize deductions and minimize errors. If you’re unsure, consider seeking help from a Clearwealth accounting professional for tailored guidance.

Reminder: Always retain receipts and supporting documentation in case CRA requests them.

Sources and References

• How to file taxes as a sole proprietor in Canada — WaveApps

https://www.waveapps.com/blog/sole-proprietor-tax-filing-canada

• Are you self‑employed? Understand tax obligations — Canada.ca

https://www.canada.ca/en/revenue-agency/news/newsroom/tax-tips/tax-tips-2024/are-you-self-employed-understand-tax-obligations.html

• Common self‑employed tax deductions — QuickBooks Canada

https://quickbooks.intuit.com/ca/resources/taxes/common-self-employed-tax-deductions/

• Guide to completing CRA T4002 — Xero Canada

https://www.xero.com/ca/guides/t4002-guide-small-businesses/

• Understanding CPP contributions for self‑employed Canadians — BBS Accounting

https://bbsaccounting.ca/understanding-cpp-contributions-for-self-employed-canadians/