A business can look healthy from the outside and still be a bad purchase.

Revenue may depend on one customer. Inventory may be slow-moving. Payroll remittances may be behind. GST/HST may have been handled incorrectly. Employment obligations may be larger than expected. The numbers may look acceptable at a glance, but the underlying risk may not.

That is why due diligence matters. It is not paperwork for its own sake. It is the process that helps you decide:

- Whether to buy

- How much to pay

- Whether to buy assets or shares

- What protections to demand before closing

Done properly, due diligence is not just about confirming value. It is about finding what could make the deal more expensive after you own it.

What Is Due Diligence When Buying a Business?

Due diligence is the buyer’s structured review of a target’s finances, operations, legal risks, tax position, and future prospects before signing or closing.

BDC describes due diligence as a review of the target’s business prospects, finances, and legal issues. That framing matters because buyers are not just asking whether the business made money last year. They are asking whether those earnings are real, repeatable, compliant, and likely to continue after the sale. (bdc.ca)

A good review looks at more than the seller’s summary package. It tests what the business really earns, what it owes, and what risks may transfer with it.

Why Deal Structure Changes the Risk So Much

The structure matters because an asset purchase and a share purchase do not create the same tax, GST/HST, administrative, or liability outcomes.

CRA states that in a share purchase, the corporation remains the same legal entity, a change in the ownership of the shares does not change the tax values of the corporation’s assets, and the purchase of shares is generally not subject to GST/HST. (canada.ca)

An asset purchase is different. The buyer may purchase selected equipment, inventory, customer relationships, and goodwill instead of the company’s shares. CRA also explains that a qualifying sale of a business or part of a business may allow the parties to make a joint election under subsection 167(1) so GST/HST does not apply to covered supplies under the agreement, but only if the conditions are met. (canada.ca)

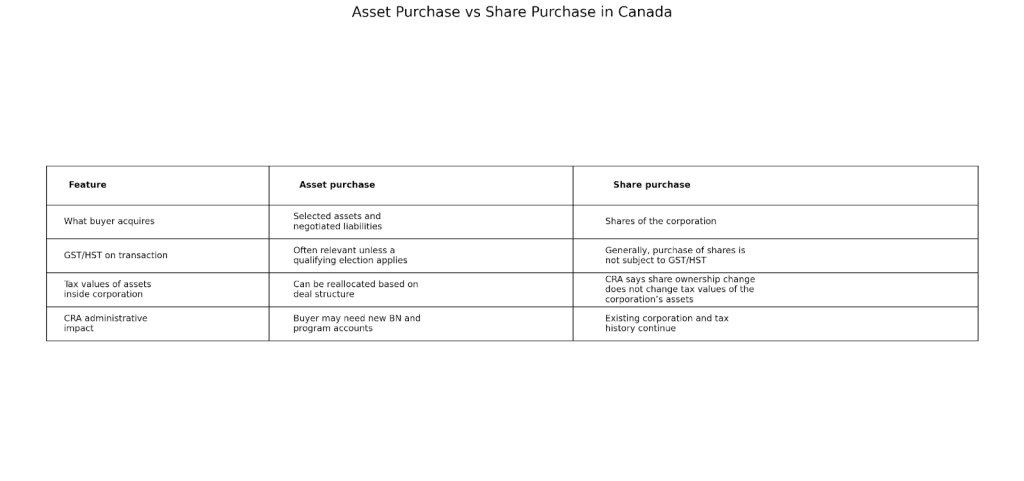

Asset Purchase vs Share Purchase

| Feature | Asset Purchase | Share Purchase |

| What the buyer acquires | Selected assets and possibly some assumed liabilities | Shares of the corporation |

| GST/HST treatment | Often relevant unless a qualifying election applies | Generally not subject to GST/HST on the share purchase |

| Tax values inside the corporation | Buyer may negotiate allocations by asset class | Change in share ownership does not change tax values of corporate assets |

| Hidden liability risk | Often narrower if liabilities are carefully excluded | Often broader because the corporation continues |

| Administrative follow-up | May require a new BN and new program accounts | Existing corporation and tax history continue |

Practical takeaway: “Asset versus share” is not just legal drafting. It affects tax treatment, registration steps, valuation, and post-closing risk.

What Tax, GST/HST, and Payroll Issues Buyers Should Check

A profitable-looking business can still become a bad purchase if filings, remittances, or records are weak.

CRA says a buyer may need a new business number and should review the GST/HST and payroll implications of the business being purchased. CRA also says records must support tax obligations and entitlements, and businesses generally must keep records for six years from the end of the last tax year they relate to. (canada.ca)

Key tax and compliance checks

- Confirm whether income tax filings are current

- Review GST/HST registrations, returns, elections, and balances

- Verify payroll remittances, T4 filings, and source deduction records

- Check whether CRA correspondence or unresolved reviews exist

- Assess whether record quality is strong enough to support reported results

Payroll deserves extra attention. CRA’s payroll guidance covers deduction, remittance, filing, corrections, penalties, and compliance obligations. Directors should also not assume payroll exposure disappears into the background. CRA states that while directors may delegate tasks, they remain responsible for ensuring payroll deductions and GST/HST are remitted. (canada.ca)

Bottom line: Good due diligence is not just a valuation exercise. It is also a compliance review.

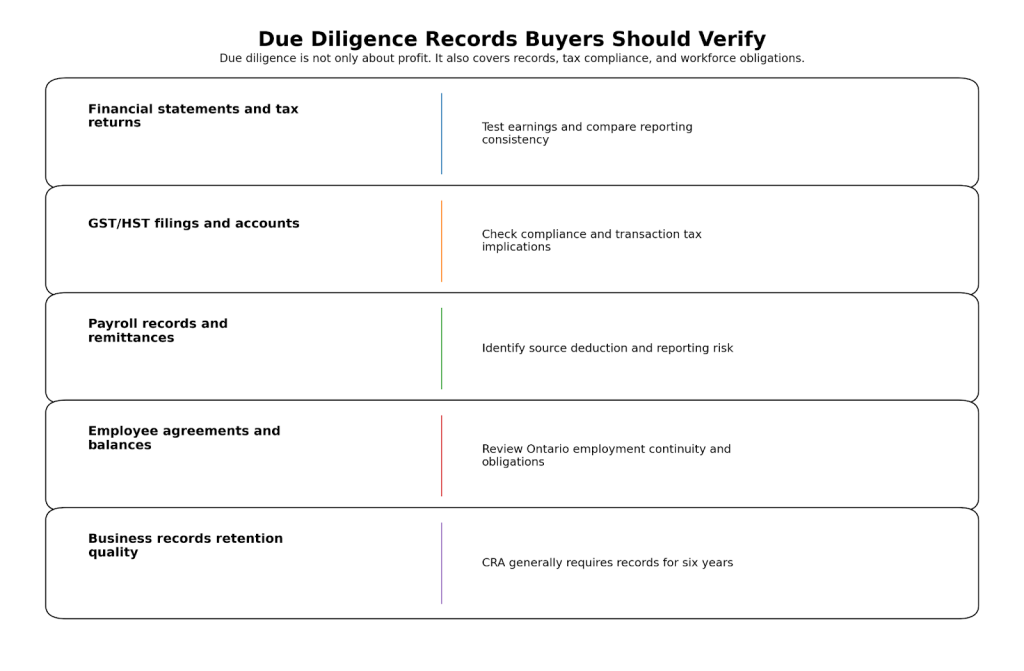

Which Financial Records Matter Most Before You Agree on Price?

The most useful records are the ones that show whether earnings are durable, not just whether revenue exists.

BDC advises buyers to examine the target’s finances, prospects, and legal issues, and warns that buyers can unknowingly become responsible for liabilities such as tax reassessments, lawsuits, and warranty claims that were not obvious at first review. (bdc.ca)

Records and metrics that matter most

- Historical financial statements

- Corporate and sales tax filings

- Customer concentration reports

- Gross margin trends

- Payroll records and employee costs

- Inventory aging and valuation support

- Debt schedules and contingent liabilities

- Working capital needs after closing

For a smaller business, practical questions often matter more than elegant models:

- Is revenue concentrated in one or two customers?

- Are gross margins stable?

- Is inventory current and saleable?

- Are owner expenses mixed into the books?

- Will the buyer need more cash after closing than the seller implies?

These issues affect both valuation and financing risk.

What Ontario Employment Risks Do Buyers Miss?

Ontario buyers often focus on tax and payroll, but miss the employment issues that continue after closing.

Ontario’s Employment Standards Act guidance explains that where there is a sale of a business and an employee of the seller is hired by the purchaser, the employee’s prior service may count as if it had been employment with the new employer for ESA rights based on length of employment. That can affect rights tied to vacation, protected leaves, termination notice, and severance-related calculations under the ESA framework. (ontario.ca)

Employment items to review early

- Employment agreements

- Vacation balances

- Benefit obligations

- Ongoing terminations or disputes

- Independent contractor classifications

- Whether employees are expected to continue after closing

This is one reason payroll due diligence is not enough by itself. Buyers should assess employment continuity and service-related obligations before finalizing price and structure.

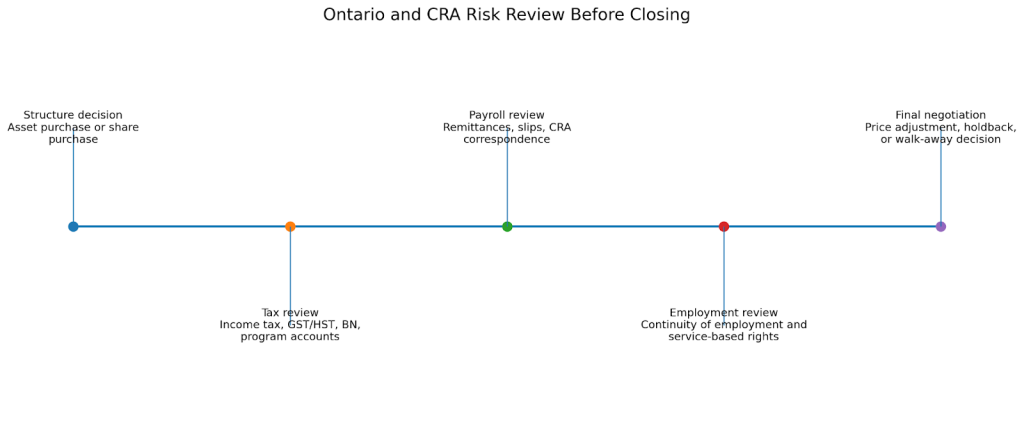

How To Run a Better Due Diligence Process

A strong process starts before the letter of intent becomes binding on the wrong terms.

Step 1: Clarify the deal structure

Decide whether you are exploring an asset purchase, a share purchase, or both.

Step 2: Request a due diligence package

Ask for financial statements, tax returns, GST/HST filings, payroll records, leases, contracts, customer concentration data, and employee information.

Step 3: Verify CRA accounts and filings

Check whether the business number, GST/HST, payroll, and related program accounts are active, current, and properly handled.

Step 4: Review record quality

Weak or incomplete records are a warning sign. If the seller cannot support the numbers, the risk usually belongs in the price or the deal protections.

Step 5: Test the earnings

Reconcile tax filings, internal statements, payroll costs, and working capital needs with the seller’s price expectations.

Step 6: Review employment exposure in Ontario

Do not assume employee obligations reset cleanly at closing.

Step 7: Address GST/HST on the transaction itself

If it is an asset deal, confirm whether a subsection 167(1) election may apply and whether the legal conditions are actually met.

Step 8: Negotiate protections

If diligence findings change the risk, they should also change the price, holdbacks, representations and warranties, indemnities, or the decision to walk away.

Common Mistakes Buyers Make

- Treating seller financials as enough

- Ignoring deal structure until late

- Skipping payroll and CRA account review

- Overlooking Ontario employee continuity rules

- Not testing customer concentration

- Assuming GST/HST on the deal is automatic or irrelevant

- Moving too fast before the records support the price

The pattern is simple: buyers often focus on the visible business and miss the administrative and compliance risks that remain after closing.

FAQ

What is due diligence when buying a business in Canada?

It is the process of verifying the target’s finances, tax filings, records, legal risks, contracts, and operating reality before you buy. The purpose is to confirm value and uncover liabilities before they become your problem. (bdc.ca)

Is an asset purchase safer than a share purchase?

Often it can reduce some inherited-liability risk, but it creates different tax and administrative consequences. CRA says share purchases generally are not subject to GST/HST, while qualifying asset sales may require separate GST/HST analysis or a valid election. (canada.ca)

Do I need to review CRA accounts before closing?

Yes. CRA says buyers may need a new business number and should review payroll and GST/HST implications. Program accounts and filing history are an important part of due diligence. (canada.ca)

How long should the target’s records be available?

CRA says records generally must be kept for six years from the end of the last tax year to which they relate. Weak or incomplete records are a major warning sign in a business purchase. (canada.ca)

What Ontario employment issue should buyers watch closely?

Continuity of employment. Ontario says that when a business is sold and the purchaser hires the seller’s employees, prior service can count for certain ESA rights based on length of employment. (ontario.ca)

Can GST/HST apply when buying business assets?

Yes. CRA explains that a qualifying sale of a business or part of a business may use the subsection 167(1) joint election so that GST/HST does not apply to covered supplies, but the rules are conditional and not automatic. (canada.ca)

Why does valuation depend on due diligence?

Because price should reflect verified earnings, working capital, assets, customer risk, liabilities, and future prospects. BDC notes that buyers can otherwise inherit problems that were not obvious in the first review. (bdc.ca)

Final Takeaway

A business purchase is not just a negotiation over price. It is a review of tax filings, payroll, records, GST/HST, employees, contracts, and structure.

Buyers who skip that work may not just overpay. They may inherit problems that were visible before closing, but only to anyone who checked.

Good due diligence does not guarantee a perfect deal. But it usually gives you a clearer price, a better structure, and a stronger chance to walk away from the wrong business before it becomes expensive.

Speak With an Advisor

If you are reviewing a potential acquisition in Ontario, a Clearwealth advisor can help you assess:

- Bookkeeping quality and earnings support

- Tax filing and GST/HST risk

- Payroll setup and remittance history

- Employment exposure

- Transaction implications before you commit

Request a tailored assessment before signing a deal that may cost more than it appears.

Disclaimer

This article is general information only, not legal, tax, accounting, or transaction advice. The right structure and tax treatment depend on your facts, the purchase agreement, the target’s records, and professional advice.

Sources & References

- https://www.bdc.ca/en/articles-tools/start-buy-business/buy-business/buying-business-conducting-due-diligence

- https://www.bdc.ca/en/articles-tools/start-buy-business/buy-business/due-diligence-valuation

- https://www.bdc.ca/en/articles-tools/entrepreneur-toolkit/templates-business-guides/due-diligence-when-buying-business-checklist

- https://www.bdc.ca/en/articles-tools/entrepreneur-toolkit/guides/buying-business-canada

- https://www.bdc.ca/en/about/mediaroom/news-releases/historic-300-billion-wave-of-business-acquisitions-set-to-reshape-canada-economy

- https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/business-registration/maintain-business/buying-business.html

- https://www.canada.ca/en/revenue-agency/services/tax/businesses/small-businesses-self-employed-income/setting-your-business/bringing-assets-into-a-business/buying-existing-business.html

- https://www.canada.ca/en/revenue-agency/services/forms-publications/publications/14-4/sale-a-business-part-a-business.html

- https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/keeping-records/where-keep-your-records-long-request-permission-destroy-them-early.html

- https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/keeping-records/gst-hst-payroll-records.html

- https://www.canada.ca/en/revenue-agency/services/forms-publications/publications/t4001.html

- https://www.canada.ca/en/revenue-agency/services/forms-publications/publications/ic89-2/director-s-liability.html

- https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/business-registration/business-number-program-account.html

- https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/gst-hst-businesses.html

- https://www.ontario.ca/laws/statute/00e41

- https://www.ontario.ca/document/employment-standard-act-policy-and-interpretation-manual/part-iv-continuity-employment

- https://www.ontario.ca/document/your-guide-employment-standards-act-0