Running a Canadian corporation often means balancing two priorities: minimizing tax legally and keeping enough cash inside the business to operate and grow. For many owner managed structures, dividends between related companies (for example, Opco paying Holdco) are part of routine planning and cash management.

Budget 2025 proposals change the timing risk. In certain group structures, a corporation that pays a taxable dividend to an affiliated corporation may not receive its dividend refund right away. If you have multiple corporations, especially with different year ends, this can create a real cash flow gap around tax payment dates.

Disclaimer: This article is general information, not legal, tax, or financial advice. Rules can change and outcomes depend on your facts. Speak with a qualified professional before acting.

Pick your path

Use this quick guide to jump to the sections that match your setup.

- One corporation, dividends paid directly to you

Focus on: Who is most exposed, Common mistakes, Roadmap - Opco and Holdco

Focus on: How the suspension works, Year end planning - Corporate group with an investment corporation (Investco)

Focus on: RDTOH basics, Passive investment income planning - Multiple corporations with different year ends

Focus on: Who is most exposed, Balance due day timing - Intercorporate dividends used for regular cash management

Focus on: What unlocks the refund, Roadmap

What are dividend refunds and RDTOH in plain English

A dividend refund is the mechanism that allows certain private or subject corporations to recover some refundable taxes after paying taxable dividends.

RDTOH (Refundable Dividend Tax on Hand) is the tracking account used to measure those refundable taxes over time.

In practical terms:

- A corporation may pay higher tax on certain types of investment income.

- Part of that tax is intended to be refundable once the corporation pays taxable dividends.

- That refundable amount sits in RDTOH until the corporation pays the right kind of taxable dividends and claims the refund.

This is why RDTOH matters in corporate tax planning. The total tax rate matters, but timing matters too. If a refund shows up later than expected, the business may need a different plan for funding taxes, payroll, or investment.

What are the proposed dividend suspension rules

Budget 2025 proposals include rules that can suspend (delay) a dividend refund in certain affiliated corporate group situations.

At a high level, the proposals target timing mismatches where:

- a payer corporation pays a taxable dividend to an affiliated recipient corporation, and

- the recipient’s balance due day for the year it receives the dividend ends after the payer’s balance due day.

The policy intent is to limit tax deferral opportunities in tiered structures that can accelerate a dividend refund in one corporation while related tax in another corporation becomes payable later.

Key point: The refund is not necessarily eliminated. In many cases, it is delayed until conditions are met.

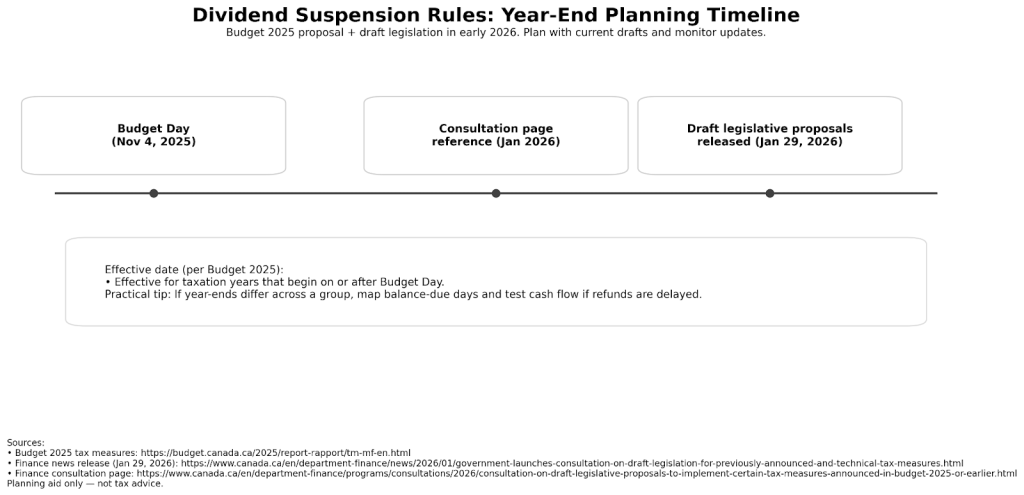

When do these rules apply

Budget 2025 indicates the measure applies for taxation years that begin on or after Budget Day (November 4, 2025).

In early 2026, the Department of Finance released draft legislative proposals for consultation that include a measure commonly described as tax deferral through tiered corporate structures.

Practical notes:

- If your year end is not December 31, your effective date depends on when your taxation year begins.

- Draft rules can evolve before enactment, so treat aggressive planning as higher risk until final legislation is in place.

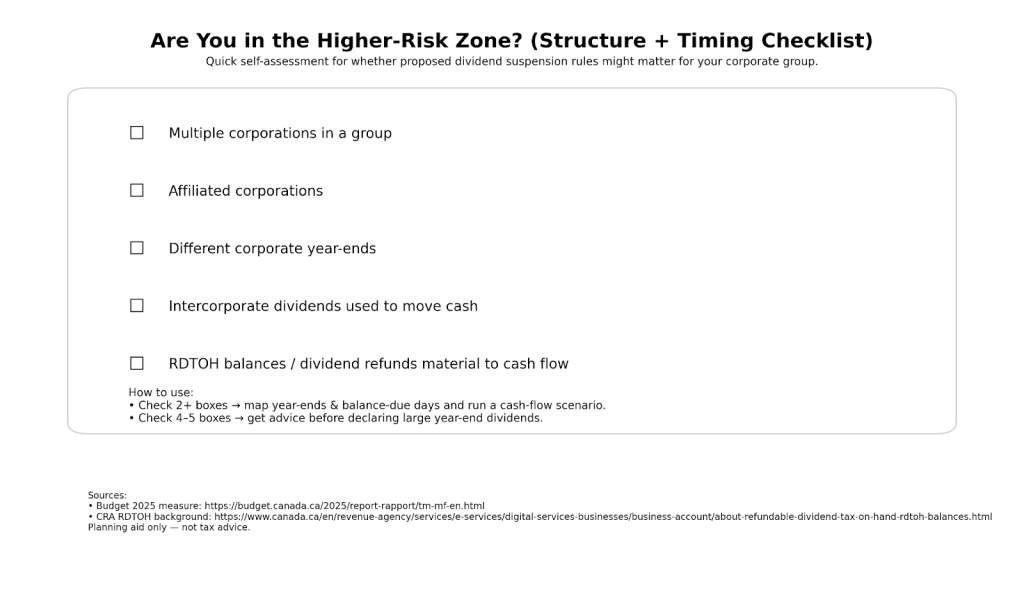

Who is most exposed

These proposals are most likely to matter if your group has one or more of the following:

1) Tiered corporate structures with related companies

Examples:

- Holdco owns Investco, Investco owns Opco

- multiple holding entities layered for historical reasons

2) Staggered year ends inside the group

This is the most common hidden risk. When year ends do not line up, balance due days can fall in different months and create the timing mismatch the proposals target.

3) Significant refundable balances

A delayed refund is more painful when the group has meaningful refundable tax amounts due to:

- passive investment income

- intercorporate dividends that trigger Part IV tax

- a combination of both

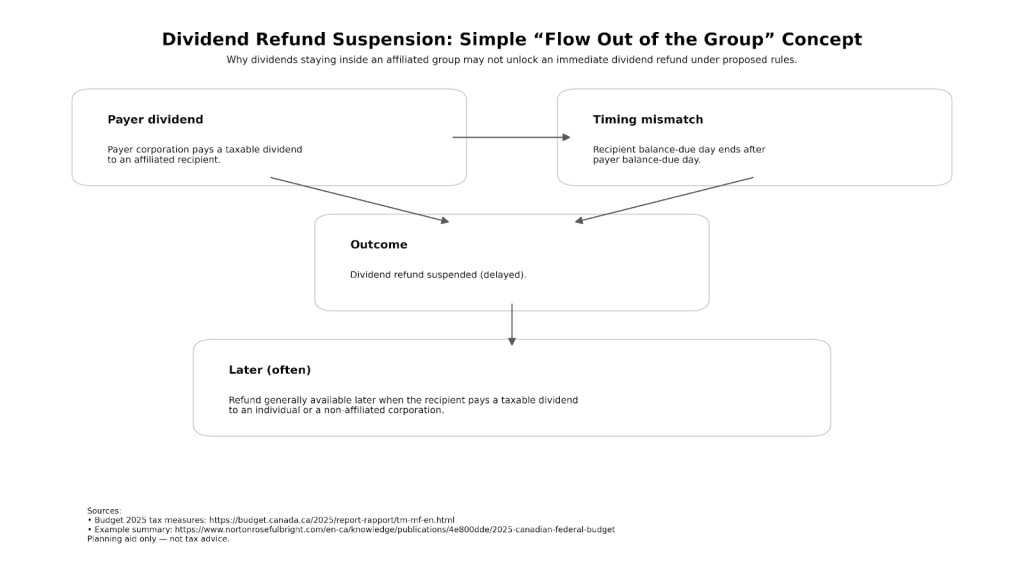

How the suspended dividend refund works, conceptually

The proposals focus on this trigger:

- a taxable dividend is paid by a payer corporation to an affiliated recipient corporation, and

- the recipient’s balance due day for the year the dividend is received ends after the payer’s balance due day.

When that happens, the payer’s dividend refund that would otherwise be available may be suspended.

What typically unlocks the suspended refund

Professional commentary on the proposals generally describes that the suspended refund becomes claimable later, commonly when dividends move out of the affiliated group, such as:

- the recipient pays a taxable dividend to an individual shareholder, or

- the recipient pays a taxable dividend to a non affiliated corporation.

Plain English translation:

- Dividends that remain inside the corporate group may not be enough to trigger an immediate refund.

- The refund becomes more closely connected to dividends ultimately flowing outside the affiliated chain.

Visual: Timing risk checklist

Use this table to spot whether you should take a closer look.

| Your situation | Likely attention level | Why it matters |

| One corporation paying dividends to an individual | Low to moderate | Less exposure to group timing mismatches |

| Opco paying Holdco with aligned year ends | Moderate | Still a group dividend, but timing may be simpler |

| Multiple corporations with different year ends | High | Balance due day sequencing is a core trigger |

| Large RDTOH balances from investment income | High | A delayed refund has a bigger cash impact |

| Dividends used to fund payroll or tax payments | High | Timing surprises can cause liquidity strain |

Why this changes corporate planning in 2026

If your planning assumes a dividend refund arrives soon after a dividend is paid, a suspension can create:

- cash flow surprises near tax payments

- more pressure on Q1 liquidity planning

- owner remuneration timing decisions (salary versus dividends)

- more complicated coordination across the group (who pays what, when)

It can also shift planning priorities, including whether:

- aligning year ends is worth revisiting

- dividend flows should be simplified

- you need a more formal cash management policy across the group

Common mistakes to avoid

- Assuming the dividend refund is automatic and immediate

Dividend refunds are already technical, and the proposed suspension adds another timing layer. - Not mapping balance due days across the group

The trigger relies on balance due day timing, not only on the dividend payment date. - Weak documentation for intercorporate dividends

Board resolutions, dividend declarations, and consistent bookkeeping matter, especially under review. - Overlooking affiliation tests

Affiliation is a specific concept under the Income Tax Act. Confirm it rather than assuming. - Treating draft rules as final

Draft legislation can change before enactment. Plan conservatively and revisit as updates are released.

Step by step roadmap to prepare

Use this workflow as a practical year end planning sequence for corporate groups.

1) Build your corporate map

- list every corporation in the group

- note ownership percentages

- confirm which corporations are affiliated

- note each year end

2) Pull refundable account balances

- current RDTOH balances (and any internal tracking)

- past dividend refund amounts

- investment income activity and Part IV exposures (if applicable)

3) Create a dividend flow calendar

- map balance due days across the group

- map planned dividends (who pays whom, and when)

- flag dividends that remain inside the group versus dividends paid to individuals

4) Stress test cash flow

- model what happens if the expected dividend refund is delayed

- confirm you can still cover taxes, payroll, and operating expenses

5) Consider simplifying (where appropriate)

Depending on your facts, this could include:

- aligning year ends where feasible

- simplifying tiered structures

- rethinking when dividends are paid out of the group

6) Document the file

- board minutes and dividend resolutions

- supporting calculations

- consistent bookkeeping entries

FAQ

Are these rules in force, or still proposed

They were proposed in Budget 2025, and draft legislative proposals were released for consultation in January 2026. Final rules may change before enactment.

What is RDTOH in simple terms

It is an account that tracks certain refundable taxes a private or subject corporation may recover, generally tied to taxes on investment income and Part IV tax, net of dividend refunds already received.

Do these rules apply to every corporation that pays dividends

Not necessarily. The proposals focus on taxable dividends paid to affiliated corporations where balance due day timing creates a deferral concern.

What triggers a suspended dividend refund

In general terms, a suspension may occur when a taxable dividend is paid to an affiliated recipient corporation and the recipient’s balance due day for the year the dividend is received ends after the payer’s balance due day.

How do you unlock a suspended dividend refund

Professional commentary generally describes that the payer may be able to claim the refund later when the recipient pays a taxable dividend to a non affiliated corporation or an individual shareholder.

What should I do before my next year end

Build a calendar of year ends, balance due days, and planned dividends across the group. Then run a cash flow scenario where the dividend refund is delayed.

Wrap up

Dividend planning inside a corporate group can be completely normal. What is changing is the timing risk. Under Budget 2025 proposals, some groups may face delays in recovering refundable taxes through the dividend refund system, especially where corporate year ends are staggered.

If you want help assessing exposure, modeling the cash flow impact, and building a cleaner dividend and year end plan, speak with a qualified accounting professional.