Can You Get a Business Loan With Bad Credit?

Bad credit is often treated as a dead end—but in practice, it is only one part of a lender’s decision.

Canadian lenders typically assess overall business viability, not just a score. That includes cash flow stability, financial statements, debt levels, and the purpose of the loan. If these areas are strong, approval may still be possible—even when credit history is less than ideal.

This matters because many business owners apply too early, relying on speed instead of preparation. In most cases, clean records and a clear repayment plan improve approval odds more than rushing an application.

What “Bad Credit” Means in Business Lending

Bad credit signals higher repayment risk. It may reflect missed payments, high credit utilization, collections activity, or limited credit history.

For business loans, this can affect:

- Loan size and approval likelihood

- Interest rates and fees

- Collateral requirements

- Repayment terms

However, lenders rarely rely on credit score alone. They also evaluate:

- Business performance and revenue trends

- Financial position and leverage

- Owner’s net worth and involvement

- Purpose and structure of the loan

Key takeaway: A weak credit profile narrows options—but it does not automatically disqualify a business.

What Lenders Evaluate Beyond Credit Score

1. Cash Flow and Repayment Capacity

Lenders focus heavily on whether your business can support loan payments.

- Stable or growing revenue increases confidence

- Predictable cash flow reduces perceived risk

- Clear repayment plans strengthen approval

2. Debt Position and Financial Structure

Two core indicators often reviewed:

- Debt service coverage: Ability to cover loan payments from income

- Debt-to-equity: How leveraged the business already is

A business with strong revenue but excessive debt may still be declined.

3. Purpose of the Loan

Specific, well-defined uses are easier to approve than vague requests.

Examples of stronger cases:

- Equipment purchases

- Expansion with defined ROI

- Working capital tied to receivables or inventory

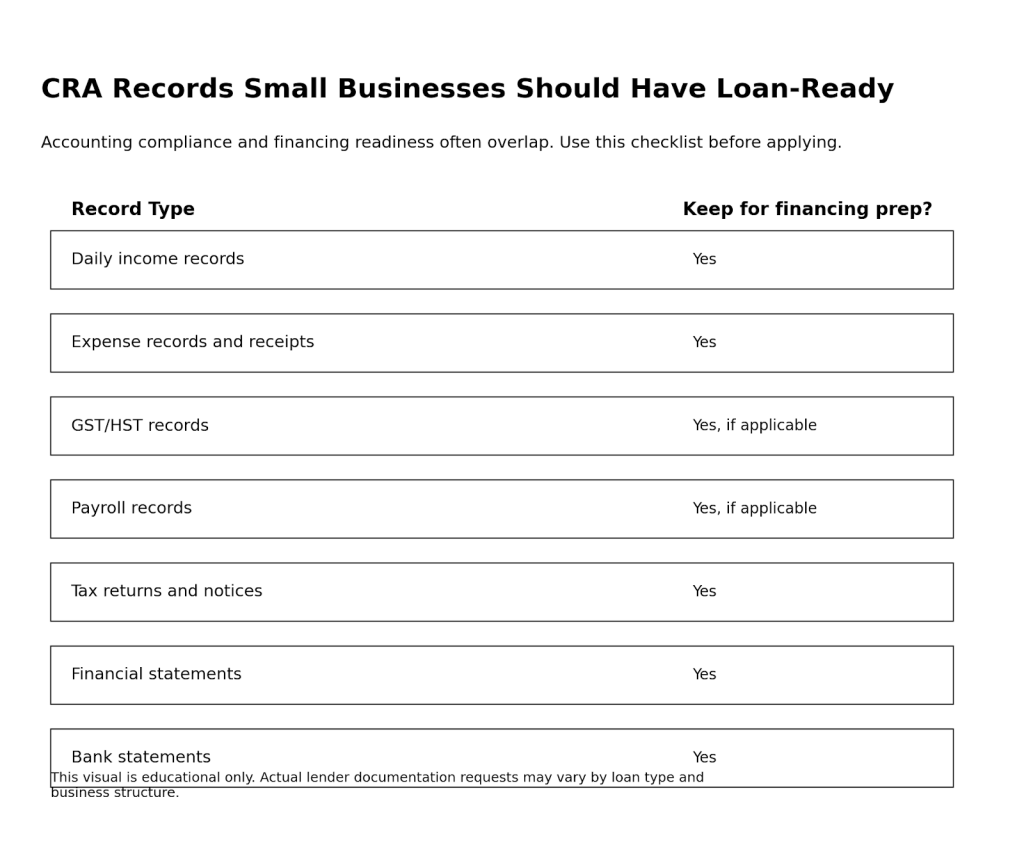

Required Financial and Tax Records

Strong documentation is often the deciding factor in borderline applications.

Businesses in Canada are expected to maintain complete financial records, including income, expenses, and supporting documents. Missing or inconsistent records can reduce lender confidence—even if the business is profitable.

Typical documents include:

- Recent financial statements

- Business bank statements

- Filed tax returns

- GST/HST filings (if applicable)

- Payroll summaries (if applicable)

- Accounts receivable and payable aging

- Business registration and ownership documents

- Clear explanation of how funds will be used

Insight: In many cases, improving bookkeeping has a greater impact on approval than improving credit score in the short term.

Financing Options for Bad Credit Borrowers

Business owners in Canada typically consider four main paths:

| Financing Option | Strength | Challenge | Best Fit |

| Traditional bank loan | Lower cost, stable terms | Stricter requirements | Established businesses with strong records |

| Government-backed programs | Risk-sharing improves access | Must meet program rules | Startups and small businesses |

| BDC-related financing | Designed for growth | Requires proof of viability | Businesses with clear expansion plans |

| Alternative lenders | Faster, more flexible | Higher cost | Urgent or non-traditional cases |

Decision insight: Speed, cost, and approval probability rarely align—choosing the right trade-off is critical.

Startups and Sole Proprietors: What Matters Most

Businesses with limited history must establish credibility quickly.

Focus areas:

- Filed and up-to-date tax returns

- Clean, organized bookkeeping

- Realistic financial projections

- Clear separation of personal and business finances

For sole proprietors, personal credit carries more weight, making accuracy and transparency even more important.

Step-by-Step: How to Improve Approval Odds

A stronger application starts before you contact a lender.

- Review your credit profile to identify errors or risks

- Update bookkeeping and reconcile accounts

- Prepare financial statements and cash flow forecasts

- Define a clear use of funds tied to business outcomes

- Match the lender to your situation (bank, program, or alternative)

- Compare total cost—not just speed of funding

Common Mistakes That Reduce Approval Chances

Even strong businesses get declined for preventable reasons:

- Applying with incomplete or outdated records

- Ignoring tax filing or compliance gaps

- Requesting funding without a defined purpose

- Prioritizing speed over affordability

- Failing to review credit reports beforehand

- Mixing personal and business finances

Pattern: Most rejections are driven by clarity and documentation—not just credit score.

FAQs

Can I get a business loan in Canada with bad credit?

Yes—if your business demonstrates strong cash flow, organized records, and a credible repayment plan. Approval depends on the lender and loan structure.

Do lenders prioritize credit score or cash flow?

Both matter, but cash flow and repayment capacity often carry greater weight in business lending decisions.

What documents should I prepare?

Financial statements, tax returns, bank statements, invoices, and any records that clearly show income, expenses, and obligations.

Are government-backed programs available to sole proprietors?

Yes, provided eligibility criteria are met.

How long should business records be kept?

Typically, records should be retained for six years after the relevant tax year.

Are alternative lenders easier to access?

They may be more accessible, especially for urgent needs, but often come with higher costs or stricter repayment terms.

Final Takeaway

A business loan with bad credit is not out of reach—but approval depends on whether your business can demonstrate reliability beyond the credit file.

In practice, lenders are asking one question: Can this business realistically repay the loan?

The strongest applications answer that clearly—with clean records, stable cash flow, and a defined purpose for the funds.

Speak With an Advisor

If you want to improve your approval odds, start with your financial foundation.

A Clearwealth accounting professional can help you:

- Prepare loan-ready financial statements

- Identify gaps in bookkeeping and tax records

- Structure a financing request that aligns with lender expectations

Request a tailored assessment to position your business for financing success.

Disclaimer

This article is for general educational purposes only and does not constitute legal, tax, or lending advice. Eligibility, rates, and approval criteria vary by lender and borrower profile.

Sources and References

Canada Small Business Financing Program

https://ised-isde.canada.ca/site/canada-small-business-financing-program/en

Canada Small Business Financing Program Guidelines

https://ised-isde.canada.ca/site/canada-small-business-financing-program/en/find-loan-your-small-business/canada-small-business-financing-program-guidelines

Frequently asked questions—For small businesses

https://ised-isde.canada.ca/site/canada-small-business-financing-program/en/frequently-asked-questions-small-businesses

Helping small businesses get loans

https://ised-isde.canada.ca/site/canada-small-business-financing-program/en/find-loan-your-small-business/helping-small-businesses-get-loans

BDC: How to get a business loan despite having a bad credit history

https://www.bdc.ca/en/articles-tools/money-finance/get-financing/find-financing-poor-credit

BDC: How a bank looks at your business

https://www.bdc.ca/en/articles-tools/money-finance/get-financing/how-a-bank-looks-at-your-business

BDC: What is the debt service coverage ratio (DSCR)?

https://www.bdc.ca/en/articles-tools/entrepreneur-toolkit/templates-business-guides/glossary/debt-service-coverage-ratio

BDC Financing

https://www.bdc.ca/en/financing

CRA: Business records

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/sole-proprietorships-partnerships/business-records.html

CRA: Keeping records

https://www.canada.ca/en/revenue-agency/services/forms-publications/publications/rc188/keeping-records.html

CRA: GST/HST and payroll records

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/keeping-records/gst-hst-payroll-records.html

Ontario: Get funding or more help

https://www.ontario.ca/page/business/start/get-funding-or-more-help

Innovation Canada Business Benefits Finder

https://innovation.canada.ca/innovation/s/list-liste?language=en_CA

RBC Business Loan Accelerator Program

https://www.rbcroyalbank.com/business/loans/business-accelerator-loan-program.html

TD Business Accelerator Loan Program

https://www.td.com/ca/en/business-banking/small-business/credit/business-accelerator-loan-program

CIBC Alternative Financing

https://www.cibc.com/en/business/advice-centre/starting-your-business/alternate-sources-of-financing.html