Many businesses do not fail because of one bad decision. They struggle because they keep defending an old decision after the facts have changed.

A software build runs over budget. A second location underperforms. A service line keeps producing weak margins. The owner tells themselves the business just needs more time. Meanwhile, payroll tightens, GST/HST falls behind, and year-end work becomes harder to manage.

That is where the sunk cost fallacy becomes expensive. It is not just a mindset issue. It can turn into a bookkeeping, tax, payroll, and cash flow problem because CRA deadlines do not pause while the business waits for a turnaround.

What Is the Sunk Cost Fallacy?

The sunk cost fallacy is the tendency to continue with a project or strategy because money, time, or effort has already been spent, even when the better decision going forward may be to stop.

A sunk cost is a past cost that cannot be recovered. Good business decisions should be based on:

- Future costs

- Future returns

- Future risk

- Future cash flow

They should not be based mainly on money already lost.

In practical terms, this shows up when owners say:

- “We already spent too much to shut it down.”

- “We need to keep going or the earlier investment was wasted.”

- “Let’s give it one more quarter,” despite weak numbers and rising obligations.

Key takeaway: Past spending may matter for your records and financial statements, but it does not automatically justify new spending.

Why This Gets Expensive for Canadian Businesses

In Canada, sunk-cost thinking becomes expensive because compliance obligations keep moving even when management decisions stall.

If a weak project keeps consuming cash, that money may no longer be available for:

- Payroll remittances

- GST/HST payments

- Supplier obligations

- Corporate tax balances

- Routine bookkeeping and year-end work

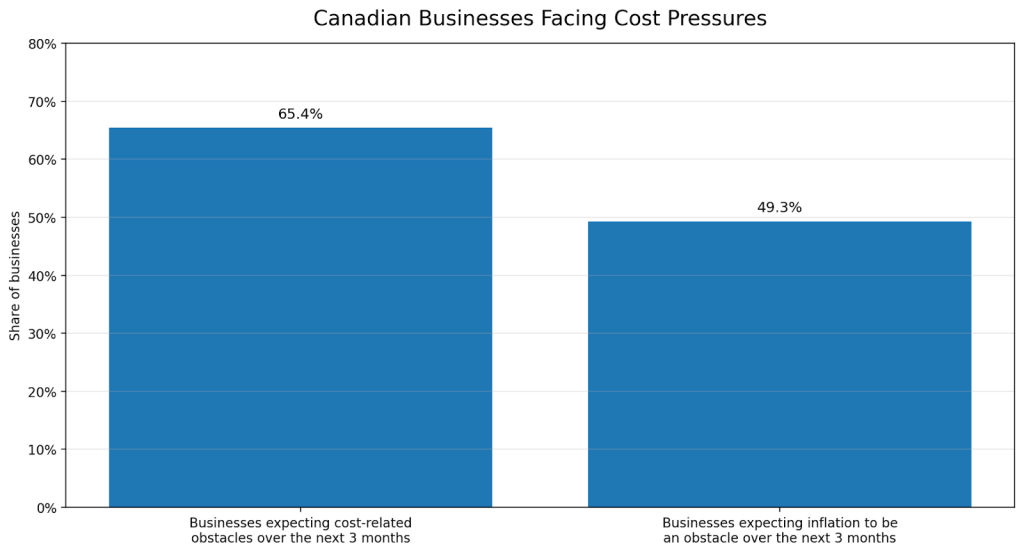

This risk grows in a high-cost, uncertain environment. Statistics Canada reported that 65.4% of businesses expected cost-related obstacles in the second quarter of 2025, and the Bank of Canada reported that uncertainty continued to weigh on business sentiment, investment, and hiring plans in 2025.

That context matters. When owners are already under pressure, they are more likely to keep funding weak decisions to avoid admitting that the original plan is no longer working.

Where the Sunk Cost Fallacy Shows Up in Real Business Operations

Bookkeeping and Recordkeeping

Weak bookkeeping makes emotional decisions easier.

If the books are late, you may not know whether a product line, client segment, or location is truly profitable. Instead of reviewing evidence, owners rely on instinct, optimism, or memory.

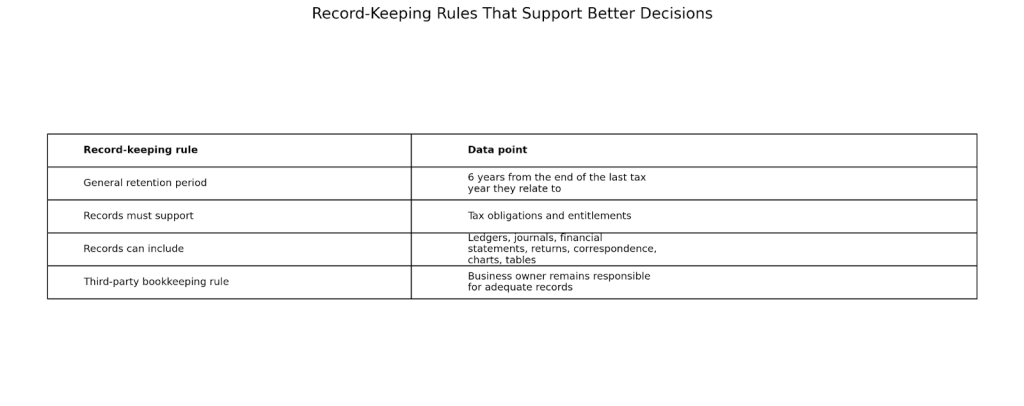

For CRA purposes, records must be detailed enough to support tax obligations and entitlements, and businesses generally need to keep them for six years. That means poor records do not just weaken decisions—they also weaken your tax position.

GST/HST

GST/HST problems often start when a struggling business delays hard choices.

A business may continue a weak initiative, cross the registration threshold, and then fall behind on filings or remittances. Once registered, obligations continue even if the business is under pressure.

CRA also expects documentary support for GST/HST claims. If invoice quality is weak, valid input tax credit claims can become harder to defend later.

Payroll

Payroll is where delayed decisions become painful fastest.

When cash gets tight, some owners start treating payroll deductions as temporary working capital. That is dangerous. CRA payroll remittance penalties escalate quickly, and the agency can also assess interest. Some accelerated remitters can also face penalties for using the wrong payment method on the due date.

Corporate Tax

A weak project can also spill into year-end and tax filing discipline.

If an owner delays cleanup, restructuring, or closing decisions, year-end work may be postponed as well. For corporations, late filing can trigger a penalty based on unpaid tax due on the filing deadline, plus an additional monthly charge while the return remains late.

Bottom line: Compliance deadlines do not wait for management confidence to return.

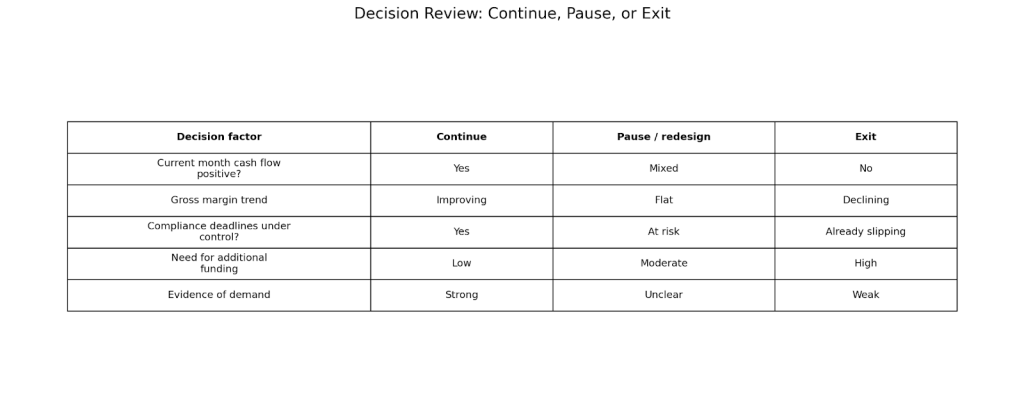

How to Tell the Difference Between Patience and Sunk-Cost Thinking

Patience is evidence-based. Sunk-cost thinking is emotion-based.

A business may be right to stay the course if it can show:

- Improving margins

- Stable or rising demand

- Manageable working capital pressure

- A realistic timeline to performance

- Capacity to meet all tax and payroll obligations while continuing

Warning signs of sunk-cost thinking include:

- The main argument is “we already spent too much to stop”

- Forecasts depend more on hope than current numbers

- Bookkeeping is behind

- Payroll or GST/HST pressure is increasing

- Nobody has documented a downside scenario or exit plan

Ask four questions before spending more:

- What additional cash must be spent from today onward?

- What measurable return is realistically expected from today onward?

- What compliance risk grows if we continue?

- What happens if we stop, sell, outsource, or pause now?

If those answers are vague, you may be dealing with bias rather than disciplined patience.

A Better Decision Framework for Small Businesses

A better process separates past spending from future choices.

| Decision Lens | Sunk-Cost Thinking | Better Accounting-Based Thinking |

| Main question | How do we justify what we already spent? | What choice gives the best result from today forward? |

| Evidence used | Hope, pride, fear of waste | Current margins, cash flow, tax deadlines, payroll pressure |

| Treatment of past spending | Used as a reason to continue | Treated as unrecoverable and separate |

| Record quality | Delayed or unclear | Up-to-date bookkeeping and support |

| Compliance impact | Easy to ignore until penalties appear | Built into the decision before more cash is committed |

| Best for | Ego protection | Business survival and cleaner financial management |

This is not a legal test. It is a practical management discipline that helps owners make better forward-looking decisions.

A Practical Roadmap for Ontario and Canadian Small Businesses

The best way to reduce sunk-cost mistakes is to create a recurring review process.

Step 1: Close the books regularly

Monthly is better than waiting for tax season. Current numbers improve decision quality.

Step 2: Separate sunk costs from future costs

Do not use unrecoverable spending as the reason to keep going.

Step 3: Review cash flow before profit claims

A project can look acceptable on paper and still create a cash crunch.

Step 4: List all compliance deadlines

Track the filing and payment dates that apply to your business, including payroll, GST/HST, T1, T2, instalments, and information slips.

Step 5: Set a stop-loss rule

Example: if margin, utilization, or sales remain below target for two review periods, the business must pause, redesign, or exit.

Step 6: Document the decision

Write down assumptions, expected return, risks, and the next review date.

Step 7: Get outside challenge

A bookkeeper, accountant, or tax advisor is usually more objective than the owner who approved the original investment.

This kind of framework is especially useful for Ontario owner-managers who make fast decisions in lean organizations.

Common Mistakes Canadian Businesses Make

- Treating past spending as a reason for future spending

- Waiting too long to update bookkeeping

- Using GST/HST or payroll cash to cover operating stress

- Confusing filing deadlines with payment deadlines

- Ignoring electronic filing or remittance rules

- Keeping subscriptions, software, locations, or roles that no longer support the core business

- Delaying outside advice because “it might still turn around”

FAQs

What is the sunk cost fallacy in business?

It is the habit of continuing with a project or expense because of what has already been spent, instead of judging whether future spending still makes sense.

Is the sunk cost fallacy a tax rule?

No. It is a decision-making bias, not a CRA rule. But it can lead to tax and compliance problems when owners delay filings, remittances, or bookkeeping cleanup.

How does this affect a sole proprietor in Canada?

Sole proprietors often feel the impact through cash flow, GST/HST registration, and personal tax balances. Filing and payment dates can also differ, which adds pressure when decisions are delayed.

How does this affect a corporation?

A corporation may keep funding an unprofitable activity too long, then fall behind on year-end accounting, GST/HST, or payroll. Late T2 filing can trigger penalties when taxes remain unpaid.

Can better bookkeeping really reduce sunk-cost mistakes?

Yes. Up-to-date books improve visibility on margins, working capital, tax obligations, and cash flow.

What is one practical way to reduce this bias?

Use a written review rule before spending more money. Compare future cost, future return, and compliance risk. If the only strong reason to continue is what you already spent, stop and reassess.

Does this matter in Ontario specifically?

Yes. Ontario businesses still face CRA filing, remittance, and recordkeeping rules, so poor decisions can still spill into federal tax and payroll consequences.

Final Takeaway

A bad past investment does not become a good future decision just because it was expensive.

For Canadian businesses, the sunk cost fallacy becomes especially costly when it spills into late bookkeeping, payroll pressure, GST/HST problems, or missed filing deadlines. The strongest response is not emotional. It is operational: better records, better review habits, and earlier outside challenge.

Speak With an Advisor

If you want an objective second look at your numbers, a Clearwealth advisor can help you review:

- Bookkeeping quality

- Payroll setup and remittances

- GST/HST support and filings

- Cash flow pressure points

- The decision framework behind a struggling product, client segment, or expansion plan

Request a tailored assessment before a manageable loss becomes a broader compliance problem.

Disclaimer

This article is general information only, not legal, tax, audit, or accounting advice. Tax treatment and business decisions depend on your facts, entity type, records, contracts, and timing.

Sources & References

- https://www.canada.ca/en/revenue-agency/news/newsroom/tax-tips/tax-tips-2025/self-employed-get-ready-tax-season-helpful-tips.html

- https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/payroll/remitting-source-deductions/how-when-remit-make-payment.html

- https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/corporations/corporation-payments/avoiding-penalties.html

- https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/gst-hst-businesses/file-gst-hst-return/reporting-requirements-deadlines/gst-hst-filing-penalties.html

- https://www.canada.ca/en/revenue-agency/services/forms-publications/publications/rc188/keeping-records.html

- https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/gst-hst-businesses.html

- https://www150.statcan.gc.ca/n1/daily-quotidien/250527/dq250527a-eng.html

- https://www.bankofcanada.ca/2025/04/business-outlook-survey-first-quarter-of-2025

- https://www.bdc.ca/en/articles-tools/entrepreneur-toolkit/templates-business-guides/financial-management

- https://docs.iza.org/dp14257.pdfbhj