For many Ontario small business owners, 2026 isn’t about one big program. It’s about understanding how several tax shifts stack together—and making sure your bookkeeping keeps up.

If you run a small business in Ontario, 2026 may feel like a year where every dollar has a job.

Payroll costs remain steady. Demand can shift quickly. And when governments announce “relief,” it’s not always clear whether it applies to you, how much it’s worth, or what steps you need to take.

The opportunity? Some businesses may keep more after-tax cash.

The risk? Missing eligibility details, timing rules, or filing steps while you’re busy running operations.

This guide breaks down the 2026 small business tax shifts in plain English—what’s changing, what to track, and how to plan without overwhelm.

Quick Start: Pick Your Path

If You’re Incorporated in Ontario (CCPC)

☐ Review Ontario’s Small Business Deduction changes starting in 2026

☐ Check whether your active business income is near the small business limit

☐ If your fiscal year spans Jan 1, 2026, plan for prorated calculations

☐ Keep clean payroll and headcount records if eligible for automatic credits

If You’re a Sole Proprietor or Partnership

☐ Track income and expenses monthly (avoid year-end catch-up)

☐ Separate personal and business spending

☐ Set aside funds for tax installments if required

☐ Maintain a digital “tax folder” for receipts and documents

If You Run Payroll

☐ Confirm CRA remittance schedules

☐ Ensure CRA account access is secure and up to date

☐ Keep employee counts and payroll summaries organized

☐ Prioritize compliance—penalties can erase tax relief

If You’re Investing in Equipment or Expanding

☐ Maintain a capital expenditure (capex) list

☐ Track “available for use” dates carefully

☐ Confirm whether accelerated write-offs apply

☐ Keep invoices, contracts, and in-service documentation

What’s Shifting in 2026 (In Plain English)

When people search “2026 tax relief Canada,” they expect one major announcement.

In reality, 2026 is a stack of targeted changes:

- Ontario is modifying Small Business Deduction mechanics (rate and income limit).

- Federal measures continue through refundable credits and investment-focused incentives.

- Personal tax adjustments may affect owner-managers who pay themselves wages.

Instead of asking “What’s the one new program?”, ask:

Which of these changes touches my business structure and my personal income?

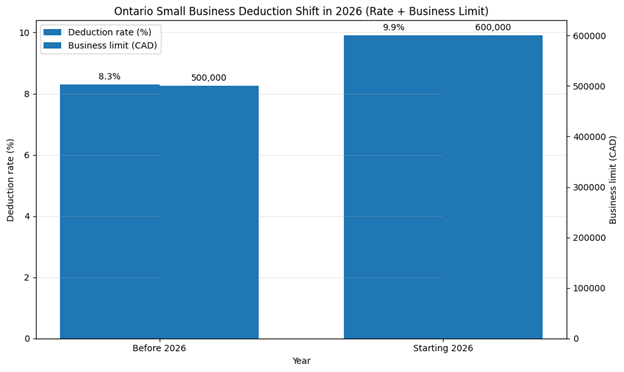

Ontario’s 2026 Change for Incorporated Small Businesses

For many incorporated small businesses, this is the headline update.

Ontario introduced legislation to:

- Increase the Small Business Deduction rate from 8.3% to 9.9%

- Increase the business limit from $500,000 to $600,000 of income eligible for the SBD

What This Means Practically

| If Your Active Business Income Is… | What It Could Mean |

| Well below the limit | Modest benefit, but positive at the margin |

| Near the limit | Potentially meaningful impact as more income qualifies |

| Above the limit | Planning matters—blended rates can surprise owners |

If your corporate year-end is not December 31 (which is common), and your taxation year crosses January 1, 2026, you may need to prorate certain calculations. This is one of the most common areas where businesses experience unexpected results.

Federal Measures Affecting Small Business

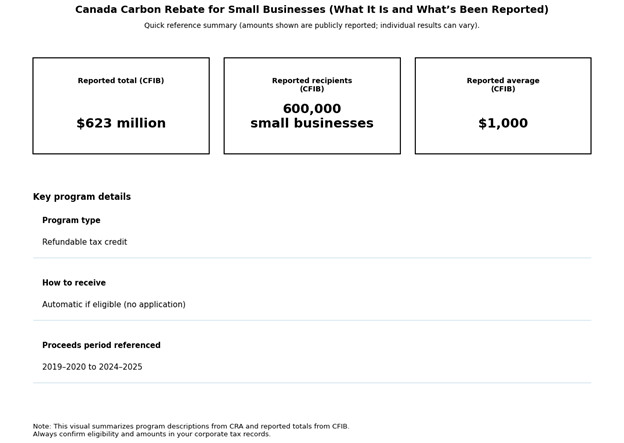

Canada Carbon Rebate for Small Businesses (Refundable Credit)

This refundable credit returns a portion of federal fuel charge proceeds directly to eligible Canadian-controlled private corporations (CCPCs).

Key points:

- It is described as automatic if eligible (no separate application required).

- “Refundable” generally means it can result in a payment even if tax payable is low.

- You should still reconcile the amount with your corporate filings and maintain supporting documentation.

Automatic does not mean ignore it.

Accelerated Write-Offs (CCA Measures)

For many small businesses, tax relief shows up through deductions rather than direct payments.

Capital Cost Allowance (CCA) allows businesses to deduct equipment and certain capital assets over time. Accelerated measures can increase first-year deductions for qualifying property acquired after specific dates and available for use before certain deadlines.

Why This Matters in 2026

- The “available for use” date can matter as much as the purchase date.

- A large purchase can reduce taxable income—and affect other thresholds.

- Poor documentation can invalidate or delay deductions.

If you’re expanding, upgrading equipment, or purchasing vehicles, timing and paperwork should be part of your planning.

A Personal Tax Change That May Affect Owners

Federal measures include a reduction to the first marginal personal income tax rate beginning in 2026.

Why small business owners should care:

- If you pay yourself or family members a salary, personal brackets matter.

- Some non-refundable credits are tied to that first rate.

- Compensation planning (salary vs dividends) conversations may shift.

It’s not a direct small business tax cut—but it can influence take-home pay and planning decisions.