If you’re trying to grow in 2026, you’re probably feeling pressure from at least one direction: higher operating costs, uneven customer demand, or the nagging sense that you’re working harder without building real profitability.

Most growth problems aren’t marketing problems—they’re planning problems. Not because you’re doing anything wrong, but because growth changes everything: cash flow timing, staffing needs, remittances, tax obligations, and how clean your books must be to make confident decisions.

The good news: Fiscal Year planning (Canada‑style) doesn’t have to be complicated. You don’t need a 40‑tab spreadsheet. You need:

- a clear target,

- a few smart guardrails,

- and a rhythm (monthly bookkeeping, quarterly check‑ins, and an intentional year‑end approach).

Quick start: pick your path for Fiscal Year 2026

Choose the closest match and start there.

| Your situation | Start here | Your “non‑negotiables” |

| Solo operator / new business | Confirm your Fiscal Year dates and set simple revenue + profit targets | Monthly bookkeeping + sales tax tracking; build a basic cash buffer plan |

| Hiring / adding payroll | Add a “true cost of employee” line (wages + employer costs + training time) | Payroll remittance routine; cash reserve; tighter monthly close |

| Scaling (new location, bigger contracts, more inventory) | Build a 12‑month cash forecast with scenarios | Capital timing + documentation; map CRA deadlines to avoid penalties |

| Incorporated (or considering it) | Review instalments, owner pay, and clean categories early | Align growth spend with year‑end planning; keep shareholder loan tidy |

What “Fiscal Year 2026 planning” really means

Your Fiscal Year is the 12‑month period your business uses for accounting and reporting. For corporations, CRA refers to this as the corporation’s tax year (its fiscal period).

Planning for Fiscal Year 2026 means:

- You set growth goals before money leaves the bank.

- You budget for timing—not just totals.

- You coordinate bookkeeping, payroll, GST/HST, and tax deadlines so growth doesn’t create avoidable surprises.

Start with a growth target your finances can actually support

A useful growth target has three layers.

1) Growth goal (plain English)

Examples:

- “Add 10 recurring clients.”

- “Open a second service route.”

2) Financial targets (simple numbers)

- Monthly revenue target

- Gross margin target (what’s left after direct costs)

- Net profit target (what’s left after all costs)

3) Capacity targets (what must change)

Headcount, hours, equipment, software, vehicles, inventory, subcontractors—whatever must increase to deliver the growth.

Why this matters: If you only set the growth goal, you can accidentally grow into a cash crunch. If you add the financial targets, you can plan the steps and timing.

Visual: Growth Target Ladder

| Layer | Question to answer | Output |

| Growth | What are we trying to achieve? | 1 primary goal + 2–3 supporting goals |

| Financial | What does “success” look like in numbers? | Revenue, margin, profit targets |

| Capacity | What must change to deliver it? | Hiring, tools, inventory, systems timeline |

Budgeting for Fiscal Year 2026 without making it complicated

A practical budget has two parts.

Your “keep the lights on” budget

- Rent/lease

- Insurance

- Software/subscriptions

- Utilities/phone/internet

- Base marketing

- Professional fees (bookkeeping/accounting)

Your “growth spend” budget

- Hiring and training

- Equipment and tools

- Increased inventory

- Sales and marketing campaigns

- Financing costs (interest, fees)

- One‑time setup costs (new location, renovations, onboarding systems)

Mini‑checklist: budget reality check

- If revenue arrives 30–60 days after delivery, do you have cash to cover the gap?

- If you add one employee, can you cover at least 3 months of payroll‑related outflow?

- If sales drop 15% for one quarter, do you stay current on remittances?

That’s the heart of small business growth planning: not “Can we grow?” but “Can we grow and stay stable?”

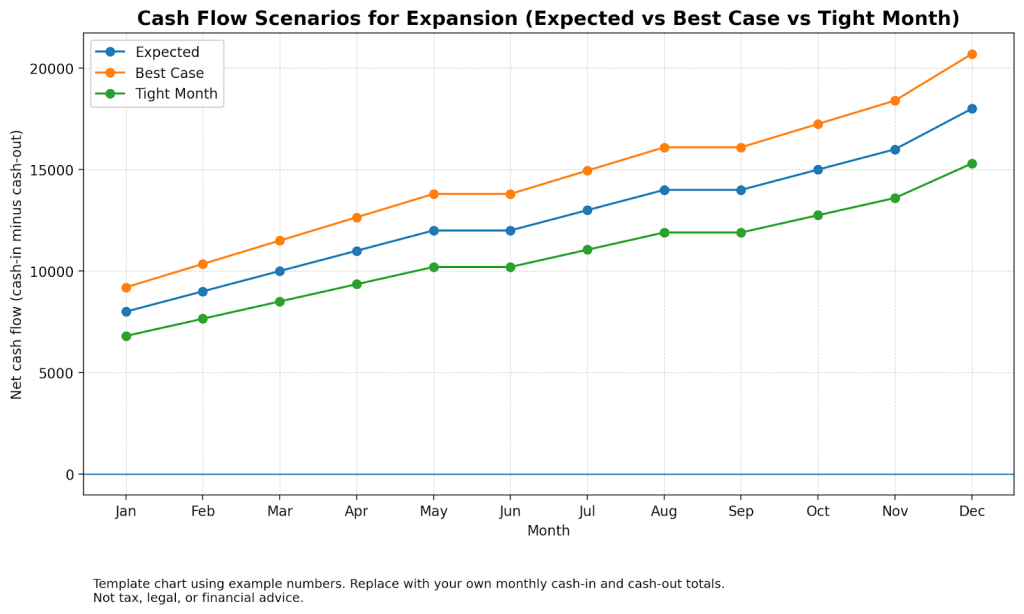

Cash flow planning for expansion: the part most businesses skip

Profit and cash are not the same. A business can show a profit on paper and still run out of money because:

- customers pay late,

- inventory ties up cash,

- loan payments don’t wait,

- remittances are due on schedule.

For growth, build a simple 12‑month cash plan with three scenarios:

| Scenario | What it’s for | What changes |

| Expected | Your most realistic plan | Normal collections + normal spend |

| Best case | Upside planning | Faster sales, earlier collections |

| Tight month | Stress‑test | Delayed payments, slower sales, higher costs |

Then add these lines (even rough estimates help):

- GST/HST remittances

- Payroll source deduction remittances (if you have employees)

- Corporate tax instalments (if applicable)

- Major one‑time purchases

Tip: Your cash plan should answer one question every month: “Do we have enough runway to keep making decisions?”

Corporate tax planning basics for Ontario businesses

If you’re incorporated and carry on business in Ontario through a permanent establishment, you’re generally dealing with both federal and Ontario corporate income tax.

In practical terms for Fiscal Year 2026, this often means:

- Your growth plan should include when profits land (and whether instalments will be required).

- Your owner pay strategy (salary vs dividends) should be reviewed alongside cash needs and compliance deadlines.

- If you have more than one corporation, association/allocation rules can matter—especially around the small business limit.

Keep it simple: You don’t need to master tax law. You do need a plan that avoids surprises.

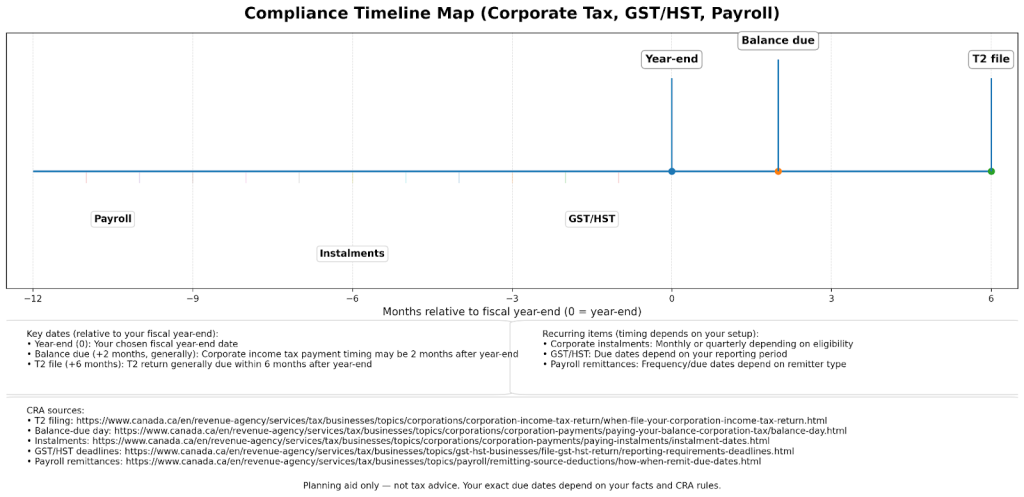

Don’t let deadlines and remittances derail momentum

Growth tends to expose weak compliance routines. Map these early and build them into your calendar.

Compliance timing map (high level)

| Item | What it impacts | What to do now |

| Corporate return (T2) filing | Late filing penalties | Confirm year‑end and assign responsibility |

| Corporate tax payment (balance due) | Interest if late—even if return is filed | Plan cash timing right after year‑end |

| Corporate instalments | Cash outflow throughout the year | Determine if monthly vs quarterly applies |

| GST/HST | Remittance schedule and penalties/interest | Confirm reporting period and due dates |

| Payroll remittances | Frequent deadlines and compliance risk | Confirm remitter type + set a routine |

Clean books = faster decisions (and fewer surprises)

If your bookkeeping is behind, growth feels like driving in fog. The fix isn’t “working harder.” It’s building a rhythm.

A realistic monthly close routine

- Reconcile bank/credit cards

- Categorize income/expenses consistently

- Review accounts receivable aging (who owes you money)

- Review GST/HST collected vs expected

- Review payroll totals and remittance schedule

- Compare actual vs budget (even at a high level)

Mini‑checklist: bookkeeping health

- Are receipts stored and linked to transactions?

- Are owner transactions clearly separated from business costs?

- Are GST/HST categories correct (and consistent)?

- Do you know your profit this month without guessing?

Capital investment planning that supports scaling

Equipment, vehicles, tools, and technology can speed up growth—but only if you:

- document the business purpose,

- track assets properly,

- and plan timing so cash flow can handle it.

Even if you’re not deciding on a major purchase today, list your “likely buys” for Fiscal Year 2026 and assign:

- estimated cost,

- target month,

- expected impact (time saved, capacity gained, quality improved),

- how you’ll pay (cash, loan, lease).

This is capital planning in plain language: spend where it increases capacity or margin.

Common mistakes that stall real growth

Here’s what shows up most often in Ontario small and mid‑sized businesses:

- Growing revenue without a cash plan (inventory, payroll, and taxes arrive before customer payments)

- Mixing business and personal spending (messy books and harder tax work)

- Waiting until year‑end to “do tax planning” (you lose options and time)

- Forgetting compliance timing (T2 filing vs tax payment vs instalments are not the same)

- Underestimating payroll admin (remittance frequency and deadlines must be respected)

- Using last year’s budget even though the business changed (growth needs a new baseline)

A step‑by‑step roadmap for Fiscal Year 2026 planning

Use this sequence. It’s simple, repeatable, and effective.

1) Set the foundation (week 1–2)

- Confirm your Fiscal Year dates and key deadlines

- Set one primary growth goal and 2–3 supporting goals

- Build a one‑page budget (baseline + growth spend)

2) Build the system (week 2–4)

- Set a monthly bookkeeping close date (same day each month)

- Create clean categories for GST/HST, payroll, owner pay, and major expenses

- Start a receipt capture routine your team will actually follow

3) Make it tax‑aware (month 2)

- Map corporate tax, GST/HST, and payroll deadlines into a calendar

- If incorporated, check whether instalments apply and plan cash timing

- Draft your year‑end approach (timing of expenses, owner pay, and major purchases)

4) Review and adjust (quarterly)

- Compare actual results to budget

- Update the cash flow forecast

- Revisit hiring timing, pricing, and capacity constraints

FAQ (Ontario + Canada)

Does “Fiscal Year” mean the same thing as calendar year?

Not always. Many businesses choose a fiscal year that isn’t January to December. For corporations, CRA treats the tax year as the corporation’s fiscal period.

When is my corporate tax return due?

Corporations generally file the T2 return within six months after the end of the tax year.

If my return is due in six months, does that mean my tax payment is due then too?

Often no. Corporate tax payments are commonly due earlier than the filing deadline.

How do corporate tax instalments work?

Instalments can be required throughout the year. Some eligible CCPCs may be able to pay quarterly instead of monthly.

How do GST/HST due dates work in Ontario?

Your due date depends on your reporting period. Your personalized return typically shows the due date.

How often do I have to remit payroll deductions?

Your remitter type sets your remitting frequency and affects due dates. It’s generally tied to your average monthly withholding amount.

What’s one simple way to avoid a growth‑related cash crunch?

Build a rolling cash forecast that includes GST/HST, payroll remittances, and (if applicable) tax instalments—then update it monthly.

Wrap‑up: Growth is easier when your numbers are on your side

Real growth isn’t just selling more—it’s building a business that can handle more. If you do the basics well in Fiscal Year 2026—budgeting, cash flow planning, clean books, and tax‑aware timing—you’ll make better decisions faster and avoid the most common growth traps.

Reminder: This is general information, not tax or financial advice. Your situation can change the right answer.

Next step (practical, low‑friction)

If you want a clean Fiscal Year 2026 plan you can actually run the business on, consider a short planning meeting with a qualified accounting professional to:

- pressure‑test your budget and cash forecast,

- map filing/payment/remittance deadlines,

- and align owner pay, growth spend, and compliance routines.