If a CRA Canada audit letter lands in your inbox, the real issue is rarely the letter itself. It is whether your books and records can prove what you filed.

For small businesses, the biggest audit risks are usually operational. Incomplete source documents, unsupported GST/HST claims, payroll errors, worker misclassification, and late remittances can turn a manageable review into an expensive dispute. For Ontario businesses, the stakes can extend beyond income tax to payroll obligations and provincial exposure tied to employer compliance.

The practical takeaway is simple: audit readiness is not a one-time project. It is a recordkeeping and reconciliation discipline. Businesses that keep clean files, separate personal and business activity, and fix errors early are usually in a stronger position if CRA asks questions.

Why This Matters to Ontario Small Businesses

A CRA audit is usually about proof, not panic. Auditors look at whether your books, invoices, payroll records, bank activity, and tax filings support the amounts you reported.

When records are incomplete, the process slows down. That often means more time spent pulling documents, more professional fees, and a higher risk that otherwise valid deductions or credits will be denied because the support is weak.

For Ontario business owners, that pressure can affect more than one return. A recordkeeping problem in one area can spill into GST/HST, payroll, shareholder transactions, or year-end corporate filings.

Quick Start: Pick Your Risk Area

Sole Proprietor or Self-Employed

Focus on business records, separating personal and business expenses, and maintaining GST/HST support.

Incorporated Business

Focus on corporate filings, shareholder transactions, payroll setup, and late-filing exposure.

Employer

Focus on payroll deductions, remittance timing, T4 accuracy, and worker classification.

GST/HST Registrant

Focus on invoices, input tax credit support, and matching returns to the underlying books.

What Does a CRA Canada Audit Actually Look For?

A CRA business audit examines whether your books and records support the amounts filed in your returns. That can include ledgers, invoices, receipts, contracts, bank statements, payroll records, and GST/HST documentation.

A business audit is not limited to suspected fraud. It is a review of whether your filings are complete, accurate, and supportable. If your records do not support your position, CRA may deny the claim or use other methods to estimate income.

Two ideas matter here:

- Books and records are the accounting data and source documents that explain your income, expenses, taxes collected, taxes claimed, payroll deductions, and other filing positions.

- Input tax credits (ITCs) allow GST/HST registrants to recover eligible tax paid or payable on business purchases used in commercial activities, but only where the supporting documents are adequate.

The Recordkeeping Mistake That Causes the Most Audit Problems

The most common CRA Canada audit mistake is weak recordkeeping.

A spreadsheet summary is not enough on its own. CRA expects the proof behind the numbers. That includes invoices, receipts, deposit records, sales records, contracts, bank statements, payroll forms, and working papers that explain how you prepared the return.

Retention also matters. Businesses generally need to keep records for at least six years from the end of the last tax year to which they relate. Destroy records too early and you may create a much larger problem than the original issue.

For Ontario businesses using cloud software, the question is not whether records are digital or paper. The question is whether they are complete, readable, retrievable, and available when requested.

How GST/HST Mistakes Increase Audit Risk

GST/HST problems often start with documentation.

A common mistake is claiming input tax credits without proper invoice support. If supplier invoices are missing required details, CRA may reduce or deny the claim during an audit.

Another recurring issue is mixing personal and business spending. Owner-managed businesses are especially exposed when one account or card is used for both. If the business-use percentage is unclear or unsupported, deductions and ITCs become vulnerable.

Late or inaccurate GST/HST filings can add cost quickly. Interest can apply to late balances, and filing failures can attract penalties depending on the facts.

GST/HST Red Flags to Review

- Missing invoice details

- Unsupported ITC claims

- Personal and business spending mixed together

- Returns that do not match accounting records

- Late or inconsistent filings

Why Payroll Errors Trigger Expensive Problems

Payroll is one of the fastest ways for routine admin issues to become real financial exposure.

Employers must deduct, remit, and report income tax, CPP contributions, and EI premiums correctly and on time. They also need records showing hours worked, amounts withheld, TD1 forms, slips issued, and returns filed.

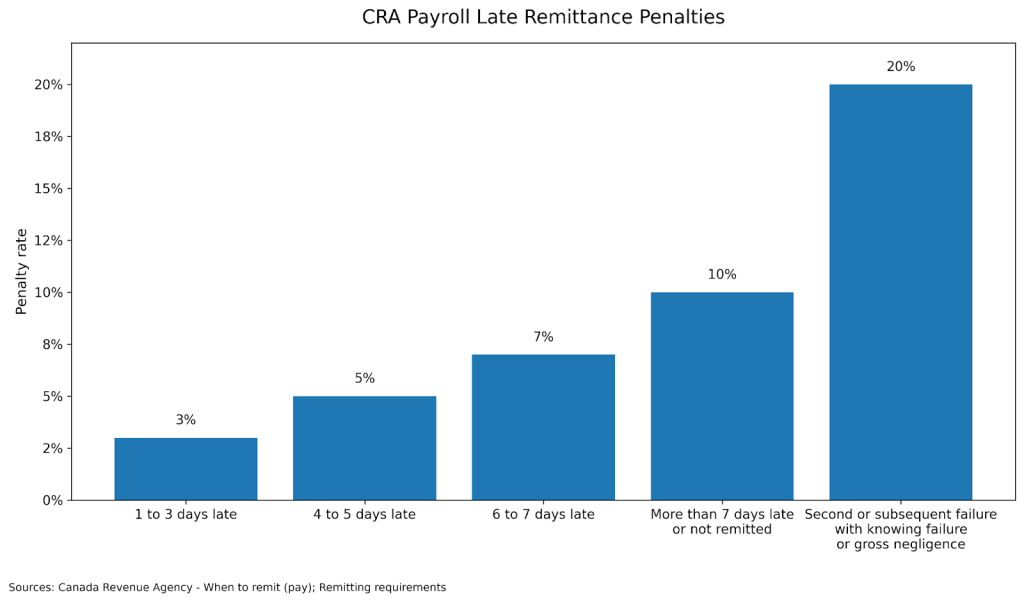

Late remittances can become expensive quickly. CRA applies graduated penalties for late payroll remittances, and repeated failures or gross negligence can increase the penalty further.

For Ontario employers, payroll compliance can also connect to provincial obligations such as Employer Health Tax. That makes reconciliation between payroll reports, remittances, T4 slips, and year-end records especially important.

Payroll Errors Small Businesses Should Catch Early

- Remitting source deductions late

- Using incorrect deduction amounts

- Incomplete employee setup documents

- T4 slips that do not match payroll totals

- Failing to reconcile year-end payroll records

What Happens When You Misclassify a Worker?

Worker misclassification is another common CRA Canada audit mistake.

Calling someone an independent contractor does not make them one. CRA looks at the real working relationship, including control, chance of profit, risk of loss, and how integrated the worker is in the business.

If CRA concludes the worker was really an employee, the business may face payroll exposure tied to CPP, EI, and income tax withholding, plus penalties and interest.

Employee vs. Contractor at a Glance

| Feature | Employee | Self-Employed Contractor |

| Control over work | Business usually directs how and when work is done | Worker usually controls how work is done |

| Chance of profit | Limited | Usually present |

| Risk of loss | Limited | Usually present |

| Payroll deductions | Employer usually withholds CPP, EI, and income tax | Worker usually handles own tax obligations |

| Audit risk if misclassified | Payroll reassessment risk | Relationship may be reclassified |

What Penalties Can Follow Audit Mistakes?

The consequences depend on the issue, but they often include denied deductions, denied ITCs, arrears interest, late-filing penalties, late-remittance penalties, and, in more serious cases, penalties for false statements or gross negligence.

For corporations, late-filing penalties can apply where tax remains unpaid by the filing deadline. For payroll, late remittance penalties can escalate based on how late the payment is. In serious cases, the financial cost of poor support goes well beyond the original tax amount.

The larger point is strategic: small documentation gaps rarely stay small once multiple filings are reviewed together. That is why businesses should treat bookkeeping, payroll, and tax reporting as connected systems rather than separate admin tasks.

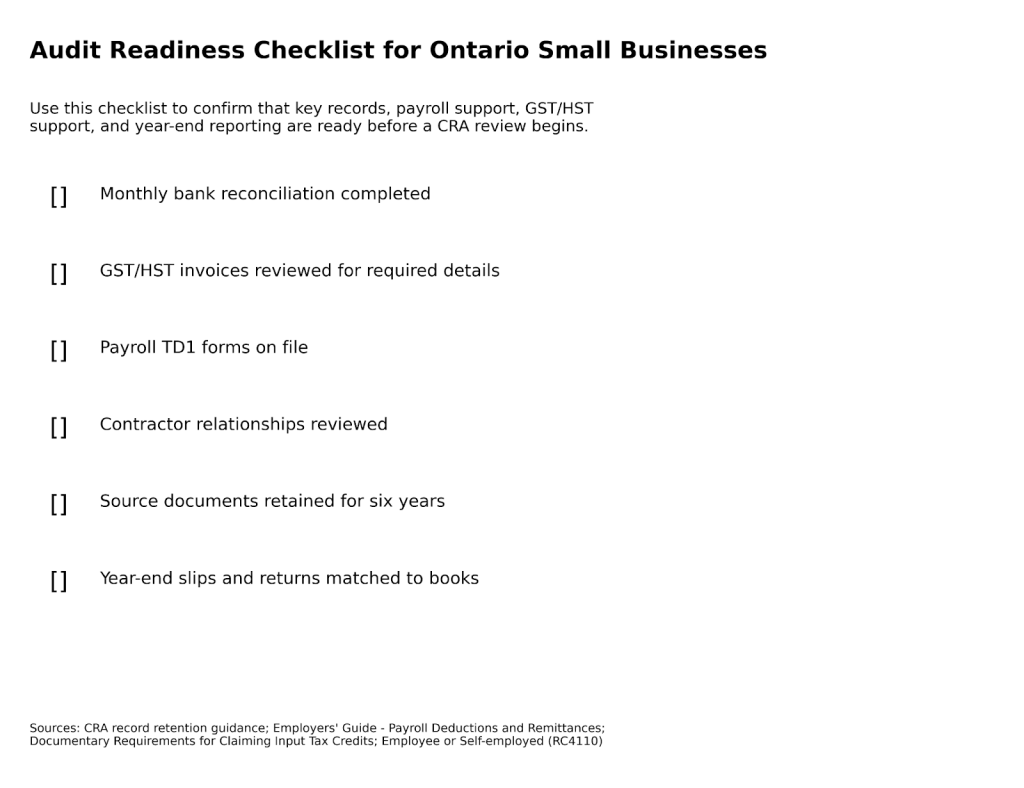

A Practical Roadmap to Prepare for a CRA Audit

The goal is straightforward: every number on a return should trace back to a source document, a ledger entry, and a reconciliation you can explain.

1. Separate Business and Personal Activity

Use dedicated bank accounts and cards wherever possible.

2. Reconcile Monthly

Match bank accounts, sales records, payroll, and tax filings before year-end.

3. Review GST/HST Support

Confirm invoices contain the information needed to support ITCs.

4. Review Payroll Setup

Check TD1 forms, deduction calculations, remittance frequency, and slip preparation.

5. Reassess Contractor Relationships

Review worker classification before CRA does.

6. Keep Records for the Required Period

Do not destroy paper or electronic records too early.

7. Fix Errors Early

If you uncover issues before CRA contacts you, professional advice may help you evaluate available correction options.

Common CRA Canada Audit Mistakes Small Businesses Need to Avoid

Most avoidable audit problems follow the same pattern: weak documents, inconsistent filings, late remittances, and positions that cannot be explained clearly when reviewed.

The most common mistakes are:

- Keeping summaries but not the underlying source documents

- Claiming GST/HST credits without proper invoice support

- Mixing personal and business spending

- Missing payroll remittance deadlines

- Misclassifying employees as contractors

- Filing late and hoping the issue will be ignored

- Waiting until CRA contact to address known errors

FAQ

How long do I need to keep business records in Canada?

Businesses generally need to keep records for six years from the end of the last tax year to which they relate. Special rules can apply.

Can CRA audit electronic records?

Yes. Electronic records still need to be complete, accessible, and able to support the amounts filed.

What records should I expect to provide during a CRA small business audit?

Depending on the scope, CRA may review ledgers, journals, invoices, receipts, contracts, payroll records, bank statements, and GST/HST support.

Can I claim a GST/HST input tax credit without a proper invoice?

That is risky. Weak or incomplete support can cause an ITC claim to be denied.

What happens if I pay payroll remittances late?

CRA can assess graduated penalties and interest, with higher exposure for repeated failures or serious non-compliance.

How does CRA decide if someone is an employee or contractor?

CRA looks at the overall relationship, including control, tools, chance of profit, risk of loss, and whether the worker is operating an independent business.

Can I fix old tax errors before CRA audits me?

Possibly. In some situations, relief may be available if the issue is addressed before CRA contact and the program requirements are met.

Does Ontario have audit exposure outside CRA?

Yes. Ontario businesses can also face reviews or audits tied to provincial taxes administered by the Ontario Ministry of Finance.

What Business Owners Should Do Next

The biggest CRA Canada audit mistake is usually not one dramatic event. It is a pattern of small gaps that builds over time: missing invoices, unreconciled books, payroll slips that do not tie out, contractor relationships that were never reviewed, and filings submitted without enough support.

The good news is that audit readiness is largely operational. Better bookkeeping, timely remittances, organized documents, and earlier correction of errors can reduce both stress and risk.

Speak with a Clearwealth accounting professional to review your recordkeeping process, strengthen your compliance controls, and prepare a practical response plan before CRA questions become expensive.

Sources and References

Canada Revenue Agency, Business audits

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/changes-your-business/business-audits.html

Canada Revenue Agency, What you should know about audits

https://www.canada.ca/en/revenue-agency/services/forms-publications/publications/rc4188/what-you-should-know-about-audits.html

Canada Revenue Agency, Keeping records

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/keeping-records.html

Canada Revenue Agency, Keeping Records (RC188)

https://www.canada.ca/en/revenue-agency/services/forms-publications/publications/rc188/keeping-records.html

Canada Revenue Agency, What are records, who has to keep them, and why it is important

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/keeping-records/what-records-who-keep-them.html

Canada Revenue Agency, Where to keep your records, for how long and how to request permission to destroy them early

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/keeping-records/where-keep-your-records-long-request-permission-destroy-them-early.html

Canada Revenue Agency, GST/HST records to keep

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/gst-hst-businesses/calculate-prepare-report/gst-hst-records-keep.html

Canada Revenue Agency, Documentary Requirements for Claiming Input Tax Credits

https://www.canada.ca/en/revenue-agency/services/forms-publications/publications/8-4/documentary-requirements-claiming-input-tax-credits.html

Canada Revenue Agency, Input tax credits

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/gst-hst-businesses/calculate-prepare-report/input-tax-credit.html

Canada Revenue Agency, Charge and collect the tax – Receipts and invoices

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/gst-hst-businesses/charge-collect-receipts-invoices.html

Canada Revenue Agency, Employers’ Guide – Payroll Deductions and Remittances

https://www.canada.ca/en/revenue-agency/services/forms-publications/publications/t4001/employers-guide-payroll-deductions-remittances.html

Canada Revenue Agency, Payroll

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/payroll.html

Canada Revenue Agency, When to remit (pay)

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/payroll/remitting-source-deductions/how-when-remit-due-dates.html

Canada Revenue Agency, Remitting requirements

https://www.canada.ca/en/revenue-agency/services/e-services/digital-services-businesses/business-account/remitting-requirements.html

Canada Revenue Agency, Employee or Self-employed (RC4110)

https://www.canada.ca/en/revenue-agency/services/forms-publications/publications/rc4110/employee-self-employed.html

Canada Revenue Agency, Employment status: Employee or self-employed

https://www.canada.ca/en/revenue-agency/services/tax/canada-pension-plan-cpp-employment-insurance-ei-rulings/employee-self-employed.html

Canada Revenue Agency, GST/HST filing penalties

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/gst-hst-businesses/file-gst-hst-return/reporting-requirements-deadlines/gst-hst-filing-penalties.html

Canada Revenue Agency, Avoiding penalties for corporations

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/corporations/corporation-payments/avoiding-penalties.html

Canada Revenue Agency, Voluntary Disclosures Program

https://www.canada.ca/en/revenue-agency/programs/about-canada-revenue-agency-cra/compliance/voluntary-disclosures-program.html

Canada Revenue Agency, IC00-1R7 Voluntary Disclosures Program

https://www.canada.ca/en/revenue-agency/services/forms-publications/publications/ic00-1/ic00-1r7-voluntary-disclosures-program.html

Ontario Ministry of Finance, What to expect during an Ontario Ministry of Finance audit

https://www.ontario.ca/document/ontarios-tax-system/what-expect-during-ontario-ministry-finance-audit

Ontario Ministry of Finance, Employer Health Tax

https://www.ontario.ca/document/employer-health-tax-eht

Disclaimer: This article is general information, not legal or tax advice. CRA audit outcomes depend on your facts, records, and filing history. It is wise to get professional advice before responding to an audit letter or correcting past filings.