Corporate life insurance can create different tax results depending on who owns the policy, who pays the premiums, who is named as beneficiary, whether the policy is term or permanent, and whether shareholders or employees receive a personal benefit. The CRA’s guidance on insurance expenses is a useful starting point, but Ontario business owners should still review the setup with an accountant, insurance advisor, and lawyer before acting.

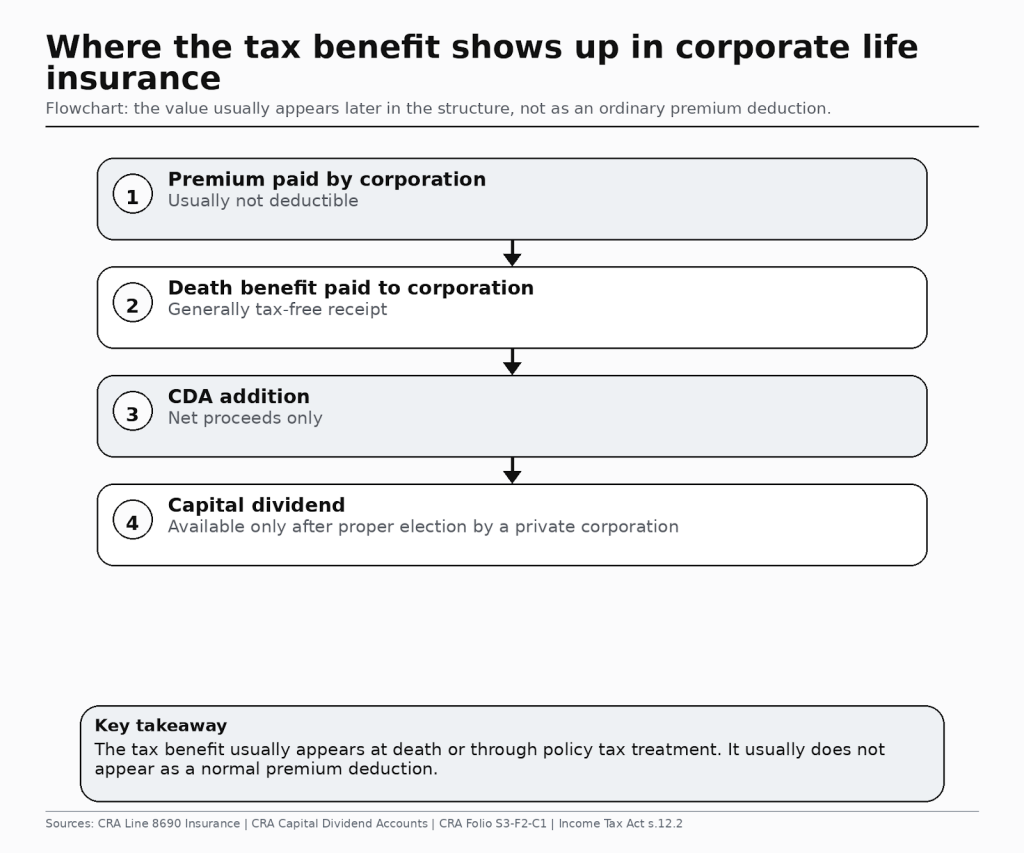

For most Ontario corporations, the tax value of corporate life insurance does not show up when premiums are paid. It usually shows up later, through tax-free proceeds to the corporation, potential additions to the corporation’s capital dividend account, and the different tax treatment of an exempt permanent policy under the Income Tax Act. The CRA is also actively warning taxpayers about aggressive insurance-based tax schemes, so the strongest planning usually comes from clean structure and documentation, not from promoter-style tax claims.

Quick Answer

In Canada, corporate life insurance premiums are usually not deductible. The CRA says this directly in its guidance on insurance expenses: in most cases, you cannot deduct life insurance premiums. The real tax benefits typically appear somewhere else. If a corporation is the beneficiary, the death benefit is generally received tax-free by the corporation. If the corporation is private, the net proceeds may increase its capital dividend account, which can support a tax-free capital dividend if the proper election is filed. And for some permanent policies, the investment buildup may be treated differently under the Income Tax Act’s accrual rules for life insurance policies. A narrow exception may allow a limited deduction when a lender requires the policy as collateral for a qualifying business or income-producing loan.

Why business owners misunderstand this area

Many owners hear “corporate life insurance” and assume it works like rent, wages, or software: pay the premium, deduct the expense, save tax now. That is usually the wrong lens.

The CRA’s rule on business insurance expenses is not especially generous for life insurance. In most cases, premiums are not deductible. That means the planning value usually comes from three other places instead: protecting the business if a shareholder or key person dies, building value inside certain permanent policies, and creating the possibility of a more tax-efficient distribution later through the capital dividend account.

That is also why this is an area where caution matters. The CRA recently warned taxpayers about aggressive tax schemes involving insurance products, especially arrangements marketed as easy tax-free access to funds. A better planning question is not “Can I write off the premium?” but “Where does the real tax benefit appear, and what rules control it?”

Where the real tax benefits actually come from

The real tax benefits of corporate life insurance usually come from the death benefit, the capital dividend account, and in some cases the different tax treatment of an exempt permanent policy. They do not usually come from deducting premiums, which is why the CRA’s insurance expense guidance is only the starting point.

The first benefit is straightforward. If the corporation is the beneficiary, the death benefit is generally received tax-free by the corporation. For a private corporation, the CRA says the net proceeds of a life insurance policy received as beneficiary are added to the capital dividend account. CRA’s more technical Capital Dividends folio explains that the amount is generally the proceeds minus the policy’s adjusted cost basis, not automatically the full face amount.

That distinction matters. The policy’s adjusted cost basis, or ACB, is a tax concept. It is not the same as cash value, fair market value, or the total premiums you remember paying. If the ACB is not what you think it is, the CDA addition may also be different from what you expected. The CRA’s capital dividend folio is the right place to verify that logic before assuming how much can come out tax-free.

The second potential tax advantage appears during life, not at death. The federal Income Tax Act section 12.2 governs accrual taxation for certain life insurance interests. In practical planning conversations, this is why exempt permanent policies are often discussed differently from non-exempt policies. That does not mean permanent insurance is automatically better, and it does not mean later access to value is automatically tax-free. It means the tax treatment can be different enough that the policy needs to be modeled carefully, especially inside a corporation.

Ontario matters too. Ontario’s corporate income tax overview confirms that corporations with a permanent establishment in Ontario are generally subject to both federal and Ontario corporate tax. As of the current Ontario page, the small business rate is 3.2% on eligible active business income, although the 2026 Ontario Budget proposes a lower 2.2% rate effective July 1, 2026, subject to legislation. That means the “pay personally or pay through the corporation” analysis is partly about insurance, but also about timing, tax rates, and cash flow.

When premiums are actually deductible

In most cases, they are not.

The CRA says in both its insurance expense line guidance and broader business expense page that life insurance premiums are generally not deductible. The main exception business owners ask about is a collateral insurance deduction.

CRA’s archived but still commonly referenced IT-309R2 bulletin on premiums used as collateral explains how narrow that exception is. The policy must be assigned to a restricted financial institution as collateral. The borrowing must be for a purpose where interest would otherwise be deductible in computing business or property income. The lender must require the policy as collateral. And even then, the deduction is limited to the lesser of the premiums paid and the net cost of pure insurance, usually prorated to the outstanding loan balance. CRA also notes that interpretation bulletins do not have the force of law, but they remain useful as CRA technical guidance.

So the practical rule is simple: a policy does not become deductible just because it relates to the business. If the lender did not require it, if the debt was not used to earn income, or if the calculation is not supportable, the deduction can fail.

Corporate ownership versus employee coverage and personal ownership

Corporate ownership can create business-continuity and CDA advantages, but it also brings technical rules around ACB, beneficiary design, elections, and possible shareholder-benefit issues. Employee coverage follows a different set of rules.

If a corporation pays premiums for employee coverage, the CRA’s page on premiums and contributions to insurance plans and the Employers’ Guide – Taxable Benefits and Allowances become important. Employer-paid premiums for certain insurance arrangements can create a taxable benefit and reporting obligation, which is a payroll issue rather than a corporate estate-planning issue.

If the policy mainly benefits a shareholder personally, the risk shifts again. CRA’s technical materials on shareholder transactions and benefits do not create a special “corporate life insurance safe zone.” If the corporation pays for something that primarily benefits the shareholder, shareholder-benefit concerns can arise. That is why ownership, beneficiary designation, and the business purpose need to line up before the policy is placed.

In practical terms:

| Arrangement | Main tax treatment | Main planning use | Main watch-out |

| Corporation owns policy on shareholder or key person | Premiums usually non-deductible; CDA may arise on net proceeds | Buy-sell funding, estate liquidity, key-person protection | CDA is based on net proceeds, not always full proceeds |

| Policy assigned as collateral | Limited deduction may apply if CRA conditions are met | Debt protection and borrowing support | Must meet lender, loan-purpose, and formula requirements |

| Employer-paid employee coverage | Can create taxable benefit and reporting obligations | Employee benefits and retention | Payroll treatment differs from owner planning |

| Personal ownership | No corporate CDA planning | Family protection outside the company | May miss business succession or continuity planning |

What a good Ontario setup usually looks like

The best setup depends on the goal. The cleanest structure usually starts by matching the business purpose to the owner, payer, and beneficiary before the policy is put in place.

Start with the purpose. Is the policy for buy-sell funding, key-person protection, debt coverage, estate liquidity, employee benefits, or long-term wealth planning? The tax answer changes with the goal, especially if you hope to rely on the collateral-insurance exception.

Next, decide who should own the policy and who should benefit from it. Corporate owner and corporate beneficiary often make sense for continuity and CDA planning. Personal ownership may fit better when the real goal is family protection outside the corporation. Mixed-purpose designs need more scrutiny because they can blur the line between business planning and personal benefit.

Then choose policy type intentionally. Term insurance is often easier to justify for temporary risks like debt or buy-sell exposure. Permanent insurance may be worth analyzing when long-term estate or balance-sheet planning matters and the policy is expected to qualify as exempt under the Income Tax Act rules. But that decision should be driven by modeling, not by the assumption that permanent automatically means better tax results.

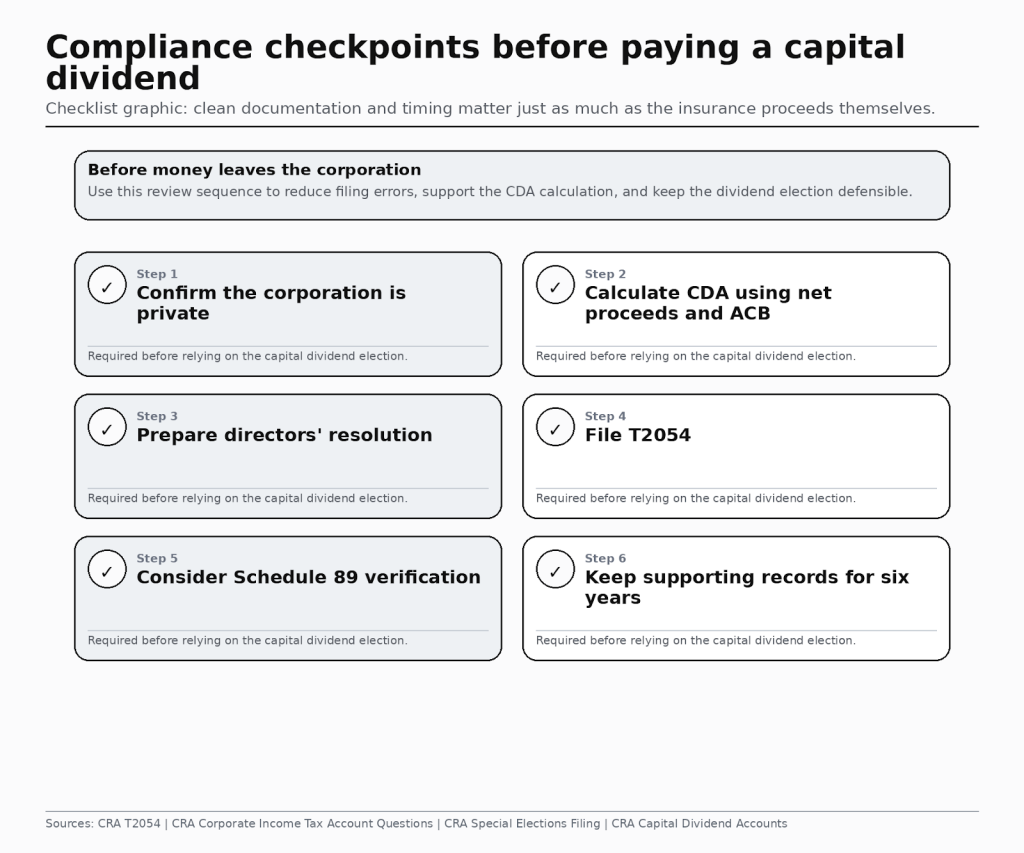

Finally, prepare the paperwork before you need it. If a private corporation plans to pay a capital dividend, the prescribed election form is T2054. CRA also says in its guidance on filing a special election or return that if you are filing T2054 through certified software, you may need to file T2 Schedule 89 first in certain situations, especially if you have not previously verified the CDA balance or disagree with CRA’s balance. CRA’s corporate income tax account Q&A reinforces that Schedule 89 is used for CDA balance verification.

Common mistakes corporations make

The most common mistake is still the simplest one: treating the premium like an ordinary deductible expense. CRA’s default position is the opposite.

The second mistake is assuming the full death benefit always creates full CDA room. CRA’s capital dividend materials make clear that ACB matters.

The third is skipping the election and verification process. If you plan to pay a capital dividend, the correct form is T2054, and in some cases Schedule 89 needs to be filed first. CRA also notes that if it accepts a late, amended, or revoked election, a penalty can apply equal to the lesser of $8,000 or $100 for each complete month from the original due date to the request date.

The fourth is ignoring payroll or shareholder-benefit issues when the policy really benefits an employee or shareholder personally. That is where technical planning can turn into reporting trouble.

And the fifth is trusting marketing claims that sound easier than the CRA’s rules. CRA’s insurance-scheme warning exists for a reason.

FAQ

Is corporate life insurance tax deductible in Canada?

Usually no. CRA says in most cases you cannot deduct life insurance premiums. The main exception is a narrow collateral-insurance deduction where the policy is required by a restricted financial institution as security for a qualifying loan.

How does the capital dividend account help?

For a private corporation, the net proceeds of a qualifying life insurance death benefit may increase the capital dividend account, which can support a tax-free capital dividend if the proper election is filed.

Does permanent insurance grow tax-free inside a corporation?

Not automatically. But exempt policies are treated differently from non-exempt policies under the Income Tax Act’s accrual rules, which is why permanent insurance is often considered in long-term corporate planning.

Are employer-paid life insurance premiums a taxable benefit?

They can be, depending on the arrangement. CRA’s payroll benefit guidance is the right place to check the treatment and reporting rules.

What forms matter before paying a capital dividend?

The core election form is T2054, and Schedule 89 may be required first in some cases to verify the CDA balance.

Final Takeaway

The real tax value of corporate life insurance in Canada is usually structural, not immediate. The benefit often appears through tax-free proceeds to the corporation, possible CDA treatment, different exempt-policy tax treatment, or a narrow collateral deduction. It is rarely a simple premium write-off. That is why the safest mindset for Ontario business owners is to assume the premium is non-deductible unless a specific CRA rule says otherwise, verify any exception carefully, and document the structure before relying on a tax result.

Sources and References

- Canada Revenue Agency, Line 8690 – Insurance https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/sole-proprietorships-partnerships/report-business-income-expenses/completing-form-t2125/line-8690-insurance.html

- Canada Revenue Agency, Capital dividend accounts

https://www.canada.ca/en/revenue-agency/services/e-services/digital-services-businesses/business-account/capital-dividend-accounts.html - Canada Revenue Agency, Income Tax Folio S3-F2-C1, Capital Dividends

https://www.canada.ca/en/revenue-agency/services/tax/technical-information/income-tax/income-tax-folios-index/series-3-property-investments-savings-plans/series-3-property-investments-savings-plan-folio-2-dividends/income-tax-folio-s3-f2-c1-capital-dividends.html - Canada Revenue Agency, Answers to common questions for Corporate income Tax accounts

https://www.canada.ca/en/revenue-agency/services/e-services/digital-services-businesses/business-account/answers-common-questions-corporate-income-tax-accounts.html - Canada Revenue Agency, T2054 Election for a Capital Dividend Under Subsection 83(2)

https://www.canada.ca/en/revenue-agency/services/forms-publications/forms/t2054.html - Canada Revenue Agency, Filing a special election or return

https://www.canada.ca/en/revenue-agency/services/e-services/digital-services-businesses/corporation-internet-filing/special-elections.html - Canada Revenue Agency, Penalty for accepting a late, amended or revoked election

https://www.canada.ca/en/revenue-agency/services/about-canada-revenue-agency-cra/complaints-disputes/late-amended-revoked-elections/penalty-accepting-a-late-amended-revoked-election.html - Canada Revenue Agency, Premiums and contributions to insurance plans

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/payroll/benefits-allowances/benefits-allowances-chart/premiums-contributions.html - Canada Revenue Agency, T4130 Employers’ Guide – Taxable Benefits and Allowances

https://www.canada.ca/en/revenue-agency/services/forms-publications/publications/t4130.html - Department of Justice, Income Tax Act, section 12.2

https://laws-lois.justice.gc.ca/eng/acts/I-3.3/section-12.2.html - Department of Justice, Income Tax Act, section 148

https://laws-lois.justice.gc.ca/eng/acts/I-3.3/section-148.html - Ontario Government, Corporate Income Tax

https://www.ontario.ca/document/corporations-tax/corporate-income-tax - Canada Revenue Agency, Warning: The CRA has identified aggressive tax schemes involving insurance products

https://www.canada.ca/en/revenue-agency/news/newsroom/tax-tips/tax-tips-2025/warning-cra-identified-aggressive-tax-schemes-involving-insurance-products.html - Canada Revenue Agency, Income Tax Folio S3-F1-C1, Shareholder Loans and Debts

https://www.canada.ca/en/revenue-agency/services/tax/technical-information/income-tax/income-tax-folios-index/series-3-property-investments-savings-plans/folio-1-shares-shareholders-security-transactions/income-tax-folio-s3-f1-c1-shareholder-loans-debts.html